The Standard and Poor’s 500 (S&P 500) is one of the most significant global stock market indices. Due to the high volatility and sensitivity of financial markets, accurately predicting their closing price remains a challenging task. Early-stage predictions of this index could significantly reduce risks associated with financial bubbles and market instability. While existing literature presents various methods for forecasting closing prices, there is a noticeable lack of comparative studies or practical implementations. To address this gap, researchers evaluated three neural network models: the Feedforward Neural Network (FFNN), Generalized Regression Neural Network (GRNN), and Radial Basis Neural Network (RBNN). The author chose to use PyCharm for developing the models due to its user-friendly interface and robust support for Python programming. The comparison focused on mathematical characteristics, prediction accuracy, and associated error metrics to determine the most effective model. Mathematically, the RBNN can be considered a hybrid of the FFNN and GRNN, as both GRNN and RBNN utilize kernel functions as activation mechanisms. For this forecasting task, the FFNN combined with the ReLU activation function produced the most accurate predictions. The analysis, conducted through three distinct evaluation methods, identified the FFNN as the most reliable model for this application. The author refrains from definitively claiming FFNN as the optimal method for predicting closing prices; however, among the neural networks considered, FFNN appears to be the most promising option. As a future implementation, the author intends to enhance the FFNN by developing a hybrid model incorporating Long Short-Term Memory (LSTM) architecture, to contribute mathematically to improve predictive accuracy and precision.

| Published in | American Journal of Applied Mathematics (Volume 13, Issue 3) |

| DOI | 10.11648/j.ajam.20251303.14 |

| Page(s) | 225-236 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

S&P 500 Index, Neural Networks, New York Financial Market, Mathematics, Kernel, Closing Price, Training Ratio, Mean Square Error

Error | Training Testing Ratios | |||||

|---|---|---|---|---|---|---|

0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

FFNN | MAE | 0.0104 | 0.0109 | 0.0082 | 0.0099 | 0.0079 |

MAPE | 0.47% | 0.49% | 0.37% | 0.44% | 0.36% | |

GRNN | MAE | 0.0007 | 0.0008 | 0.0002 | 0.0005 | 0.0006 |

MAPE | 0.94% | 0.97% | 0.55% | 0.82% | 0.83% | |

RBNN | MAE | 0.0136 | 0.0535 | 0.0312 | 0.0206 | 0.0795 |

MAPE | 2.86% | 7.06% | 5.10% | 3.66% | 9.27% | |

Training Testing Ratios | ||||||

|---|---|---|---|---|---|---|

0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

FFNN | Linear | 145.55 | 143.7 | 180.37 | 51.86 | 198.3 |

Polynomial | 137.93 | 134.96 | 179.69 | 50.40 | 196.98 | |

GRNN | Linear | 70.21 | 24.58 | 16.98 | 44.06 | 188.92 |

Polynomial | 66.83 | 23.23 | 16.52 | 43.14 | 180.98 | |

RBNN | Linear | 14.51 | 9.92 | 29.25 | 99.45 | 20.25 |

Polynomial | 14.31 | 9.58 | 28.73 | 93.43 | 20.16 | |

EFFR | Effective Federal Funds Rate |

FFNN | Feedforward Neural Network |

GRNN | Generalized Regression Neural Network |

LSTM | Long Short-term Memory |

MAE | Mean Absolute Error |

MAPE | Mean Absolute Percentage Error |

MSE | Mean Square Error |

RBF | Radial Basis Function |

RBNN | Radial Basis Neural Network |

S&P 500 | Standard & Poor’s 500 |

| [1] | Dilpriya, T. A. H., Lanel, G. H. J., Perera, M. T. M. Reviewing the efficacy of Federal Reserve Bank reserve policies through a time series analysis of the effective federal funds rate. International Journal of Research and Innovation in Social Science (IJRISS). 2023, 7(4), pp. 869-880. |

| [2] | Challet, D., Bel Hadj Ayed, A. Predicting financial markets with Google Trends and not so random keywords. Social Science Research Network (SSRN). 2013. |

| [3] | Dilpriya, T. A. H., Lanel, G. H. J., Perera, M. T. M., Vidanage, B. V. N. C. Analysing the S&P 500 index in relation to the Google Trends of stock market-related words in the United States. In Transformative applied research in computing, engineering, science and technology, 1st Ed. CRC Press: Boca Raton, Florida, USA; 2025, p. 8. |

| [4] | Mintarya, L. N., Halim, J. N. M., Angie, C., Achmad, S., Kurniawan, A. Machine learning approaches in stock market prediction: A systematic literature review. Procedia Computer Science. 2023, 216, pp. 96–102. |

| [5] | Zhang, A., Zhong, G., Dong, J., Wang, S., Wang, Y. Stock market prediction based on generative adversarial network. Procedia Computer Science. 2019, 147, pp. 400–406. |

| [6] | Hiransha, M., Gopalakrishnan, E. A., Vijay, K. M., Soman, K. P. NSE stock market prediction using deep-learning models. Procedia Computer Science. 2018, 132, pp. 1351–1362. |

| [7] | Thilakarathne, H., Lanel, J., Perera, T., Vidanage, C. Predicting S&P 500 Closing Prices Using a Feedforward Neural Network: A Machine Learning Approach, Journal of Mathematics and Statistics Studies. 2025, 6(1), pp. 18-31. |

| [8] | Selvin, S., Vinayakumar, R., Gopalakrishnan, E. A., Menon, V. K., Soman, K. P. Stock price prediction using LSTM, RNN and CNN-sliding window model. In International Conference on Advances in Computing, Communications and Informatics (ICACCI). IEEE, 2017; pp. 1643–1647. |

| [9] | Nelson, D. M. Q., Pereira, A. C. M., de Oliveira, R. A. Stock market's price movement prediction with LSTM neural networks. In International Joint Conference on Neural Networks (IJCNN). IEEE, 2017; pp. 1419–1426. |

| [10] | Vargas, M. R., De Lima, B. S. L. P., Evsukoff, A. G. Deep learning for stock market prediction from financial news articles. In IEEE International Conference on Computational Intelligence and Virtual Environments for Measurement Systems and Applications (CIVEMSA), Annecy, France, 2017; pp. 60-65. |

| [11] | Pilla, P. R., Mekonen, R. Forecasting S&P 500 Using LSTM Models. |

| [12] | Htun, H. H., Biehl, M., Petkov, N. Forecasting relative returns for S&P 500 stocks using machine learning. Financ Innov. 2024, 10, p. 118. |

| [13] | Shi, B., Tan, C., Yu, Y. Predicting the S&P 500 stock market with machine learning models. Applied and Computational Engineering. 2024, 48, pp. 255-261. |

| [14] | Rodriguez, F. S., Norouzzadeh, P., Anwar, Z. et al. A machine learning approach to predict the S&P 500 absolute percent change. Discov Artif Intell. 2024, 4(8). |

| [15] | Zhang, W. S&P 500 Index Price Prediction Based on ARIMA Model. Advances in Economics, Management and Political Sciences. 2025, 147, pp. 156–161. |

APA Style

Thilakarathne, H. D., Lanel, J., Perera, T., Vidanage, C. (2025). A Mathematical Evaluation of Diverse Neural Network Models to Predict S&P 500 Closing Prices in the New York Financial Market. American Journal of Applied Mathematics, 13(3), 225-236. https://doi.org/10.11648/j.ajam.20251303.14

ACS Style

Thilakarathne, H. D.; Lanel, J.; Perera, T.; Vidanage, C. A Mathematical Evaluation of Diverse Neural Network Models to Predict S&P 500 Closing Prices in the New York Financial Market. Am. J. Appl. Math. 2025, 13(3), 225-236. doi: 10.11648/j.ajam.20251303.14

@article{10.11648/j.ajam.20251303.14,

author = {Hirushi Dilpriya Thilakarathne and Jayantha Lanel and Thamali Perera and Chathuranga Vidanage},

title = {A Mathematical Evaluation of Diverse Neural Network Models to Predict S&P 500 Closing Prices in the New York Financial Market},

journal = {American Journal of Applied Mathematics},

volume = {13},

number = {3},

pages = {225-236},

doi = {10.11648/j.ajam.20251303.14},

url = {https://doi.org/10.11648/j.ajam.20251303.14},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ajam.20251303.14},

abstract = {The Standard and Poor’s 500 (S&P 500) is one of the most significant global stock market indices. Due to the high volatility and sensitivity of financial markets, accurately predicting their closing price remains a challenging task. Early-stage predictions of this index could significantly reduce risks associated with financial bubbles and market instability. While existing literature presents various methods for forecasting closing prices, there is a noticeable lack of comparative studies or practical implementations. To address this gap, researchers evaluated three neural network models: the Feedforward Neural Network (FFNN), Generalized Regression Neural Network (GRNN), and Radial Basis Neural Network (RBNN). The author chose to use PyCharm for developing the models due to its user-friendly interface and robust support for Python programming. The comparison focused on mathematical characteristics, prediction accuracy, and associated error metrics to determine the most effective model. Mathematically, the RBNN can be considered a hybrid of the FFNN and GRNN, as both GRNN and RBNN utilize kernel functions as activation mechanisms. For this forecasting task, the FFNN combined with the ReLU activation function produced the most accurate predictions. The analysis, conducted through three distinct evaluation methods, identified the FFNN as the most reliable model for this application. The author refrains from definitively claiming FFNN as the optimal method for predicting closing prices; however, among the neural networks considered, FFNN appears to be the most promising option. As a future implementation, the author intends to enhance the FFNN by developing a hybrid model incorporating Long Short-Term Memory (LSTM) architecture, to contribute mathematically to improve predictive accuracy and precision.},

year = {2025}

}

TY - JOUR T1 - A Mathematical Evaluation of Diverse Neural Network Models to Predict S&P 500 Closing Prices in the New York Financial Market AU - Hirushi Dilpriya Thilakarathne AU - Jayantha Lanel AU - Thamali Perera AU - Chathuranga Vidanage Y1 - 2025/06/30 PY - 2025 N1 - https://doi.org/10.11648/j.ajam.20251303.14 DO - 10.11648/j.ajam.20251303.14 T2 - American Journal of Applied Mathematics JF - American Journal of Applied Mathematics JO - American Journal of Applied Mathematics SP - 225 EP - 236 PB - Science Publishing Group SN - 2330-006X UR - https://doi.org/10.11648/j.ajam.20251303.14 AB - The Standard and Poor’s 500 (S&P 500) is one of the most significant global stock market indices. Due to the high volatility and sensitivity of financial markets, accurately predicting their closing price remains a challenging task. Early-stage predictions of this index could significantly reduce risks associated with financial bubbles and market instability. While existing literature presents various methods for forecasting closing prices, there is a noticeable lack of comparative studies or practical implementations. To address this gap, researchers evaluated three neural network models: the Feedforward Neural Network (FFNN), Generalized Regression Neural Network (GRNN), and Radial Basis Neural Network (RBNN). The author chose to use PyCharm for developing the models due to its user-friendly interface and robust support for Python programming. The comparison focused on mathematical characteristics, prediction accuracy, and associated error metrics to determine the most effective model. Mathematically, the RBNN can be considered a hybrid of the FFNN and GRNN, as both GRNN and RBNN utilize kernel functions as activation mechanisms. For this forecasting task, the FFNN combined with the ReLU activation function produced the most accurate predictions. The analysis, conducted through three distinct evaluation methods, identified the FFNN as the most reliable model for this application. The author refrains from definitively claiming FFNN as the optimal method for predicting closing prices; however, among the neural networks considered, FFNN appears to be the most promising option. As a future implementation, the author intends to enhance the FFNN by developing a hybrid model incorporating Long Short-Term Memory (LSTM) architecture, to contribute mathematically to improve predictive accuracy and precision. VL - 13 IS - 3 ER -

Department of Computer and Data Science, Faculty of Computing, NSBM Green University, Homagama, Sri Lanka

Biography: Hirushi Dilpriya Thilakarathna is a Lecturer in the Department of Computer and Data Science at NSBM Green University. She holds a Bachelor of Science (Hons.) Degree in Mathematics with First Class Honors from the University of Sri Jayewardenepura, Sri Lanka, where she graduated as the top student in her batch in 2021. In recognition of her outstanding academic performance, she was awarded the Dr. Sunethra Weerakoon Memorial Gold Medal and the Dr. Srimathi Wewala Gold Medal for excellence in Mathematics. Ms. Thilakarathna is currently pursuing her PhD in Mathematics at the University of Sri Jayewardenepura. Jayewardenepura. At NSBM Green University, she lectures in Advanced Mathematics, Probability, Statistical Inference, Descriptive Statistics, and Computational Thinking Development. She is a member of the Computer Society of Sri Lanka and remains actively engaged in academic and research pursuits in her field.

Research Fields: Actuarial Science, Financial Mathematics, Neural Networks, Mathematical Modelling, Telecommunication Networks, Graph Theory, Computational Theory

Department of Mathematics, Faculty of Applied Science, University of Sri Jayewardenepura, Nugegoda, Sri Lanka

Research Fields: Graph Theory and its Applications, Optimization, Deep Learning

Department of Mathematics, Faculty of Applied Science, University of Sri Jayewardenepura, Nugegoda, Sri Lanka

Research Fields: Financial Mathematics, Graph Theory

Department of Mathematics, Faculty of Applied Science, University of Sri Jayewardenepura, Nugegoda, Sri Lanka

Research Fields: Number Theory, Abstract Algebra.

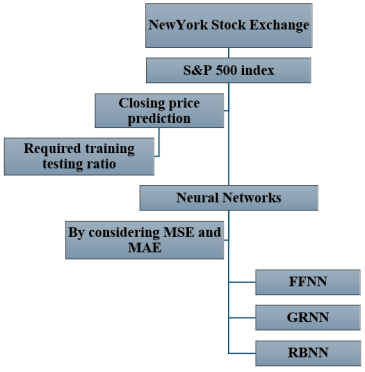

Figure 1. Research design of the S&P 500 index closing price prediction.

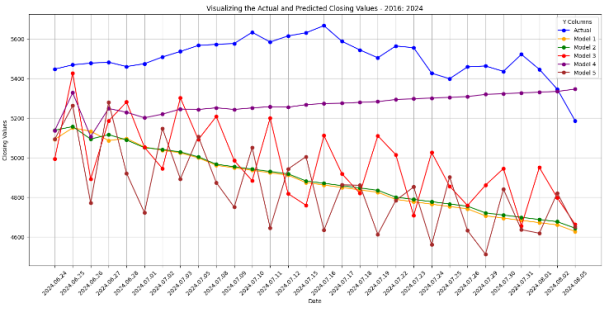

Figure 2. Actual and predicted closing prices by using FFNN.

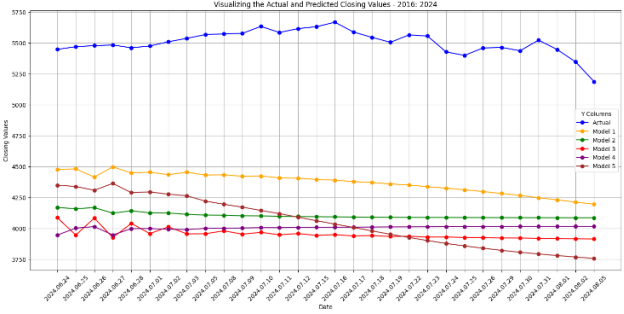

Figure 3. Actual and predicted closing prices by using GRNN.

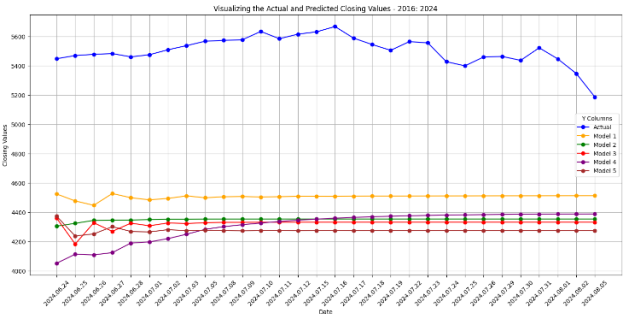

Figure 4. Actual and predicted closing prices by using RBNN.

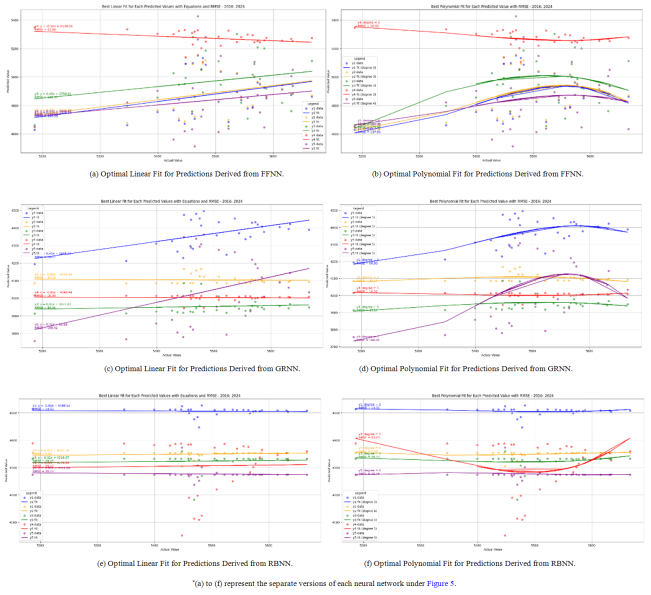

Figure 5. *Fitted Models from each Neural Network.

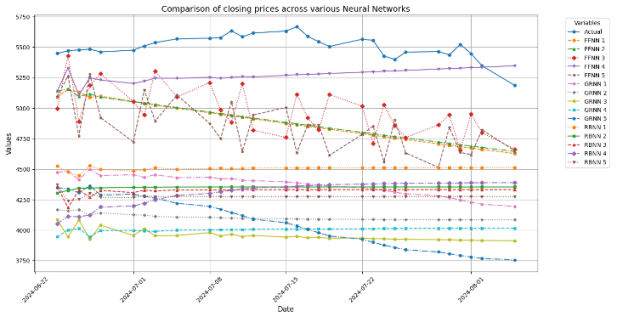

Figure 6. Comparative Analysis of Predictions across each Neural Network Architecture.

Information