2. Literature Review

The reviews literature is centered on studies on tax incentives in attracting foreign direct investments for the Agro-processing industries. The study explores the subject by reviewing both theoretical and empirical literature on previous works.

2.1. Tax

Tax is the main source of Government revenue for any country in the world of which Ghana is not an exception. Taxes are backed by law which makes it compulsory payments for which no value or service has to be rendered in return by the tax payer. It is a financial charge or levy imposed on an individual or a legal entity by the state. According to Justice Wendell Holmes

| [12] | Holmes, O. W., Jr., 1904. Compania General de Tabacos de Filipinas v. Collector of Internal Revenue, 275 U.S. 87. U.S. Supreme Court. |

[12]

a famous American judge, “a tax is a price we pay for living in a civilized society”. Taxation is based on an arbitrary system of laws passed by Parliament and interpreted by the Judiciary, giving effect to what one must assume to be the democratic will of the citizens

| [1] | Akoto, J., 2001. Principles and practice of taxation in Ghana. Accra: City Publishers. |

[1]

. Tax is defined as pecuniary burden laid upon an individual, entities or properties to support the Government. It’s not a voluntary donation, but an enforced contribution, enacted pursuant to legislative authority. Early form of taxation in Ghana was indirect tax in the then Gold Coast. It was started in the form of custom duties in 1850. This was levied on imported goods at the rate of ½% ad valorem. This tax was introduced by the British after they had taken over the Danish Forts and trading posts to meet the cost of administering the colonies.

| [25] | Samiei, H., 1999. Ghana: Tax reform and revenue productivity. IMF Working Paper. Washington, D. C.: International Monetary Fund. |

[25]

.

2.2. Tax Administration in Ghana

According to

| [10] | Government of Ghana, 1943. Income Tax Ordinance No. 27 of 1943. Accra: Government Printer. |

[10],

the institution responsible for tax administration and collection in Ghana has changed in name from Income Tax Department under the Income Tax ordinance (No. 27) of 1943, through to Central Revenue Department with the introduction of the other taxes and duties between 1961 and 1963. This re-organization continued in 1986 and by virtue of the enactment of P.N.D.C law 143 of 1986, where the name changed to Internal Revenue Service

| [13] | Internal Revenue Service, 2000. Internal Revenue Service Act, 2000. Accra: Ghana Publishing Corporation. |

[13]

to its current form Domestic Tax Revenue Division of Ghana Revenue Authority upon passing the Ghana Revenue Authority Act 2009 (Act 791). Ghana Revenue Authority thus replaces the Ghana Revenue Agencies in the Administration of Taxes and Customs Duties in the country.

| [8] | Ghana Revenue Authority (GRA), 2010. GRA News. Accra: Ghana Revenue Authority. |

[8]

. All this reorganization is to make tax administration effective and efficient in responding to improve tax collection over the years.

2.3. Taxation from Global Perspective

As several government regimes make conscious efforts to attract and direct multinational companies with capital to invest around stable and promising economies, which comes along with associated technology spillovers, fiscal incentives have become a global tool from tax holidays and import duty exemptions to investment allowances and accelerated depreciation for achieving such goals.

| [19] | Morisset, J., 2003. Tax incentives: Using tax incentives to attract foreign direct investment. Public Policy for the Private Sector Note No. 250. Washington, D. C.: World Bank. |

[19]

. This trend appears to have strengthened since the early 1990s. At a glance, the impact of tax incentives on foreign direct investment appears uncertain. Over the past few decades’ time-series econometric analysis and literature on international investors have shown that tax incentives are not the most influential factor for multinationals in selecting investment locations. More important to investors are such factors as basic infrastructure, political stability, and the cost and availability of labor. Both analysis and surveys have confirmed that tax incentives are a poor instrument for compensating for negative factors in a country’s investment climate.

| [22] | Oman, C., 2000. Policy competition for foreign direct investment: A study of competition among governments to attract FDI. Paris: OECD. |

[22]

.

According to

| [18] | Moran, T. H., 1998. Foreign direct investment and development: The new policy agenda for developing countries and economies in transition. Washington, D. C.: Institute for International Economics. |

[18]

, Tax incentives have direct effect on foreign direct investment. It is no coincidence that in 1985-94 foreign direct investment grew more than fivefold in tax havens in the Caribbean and South Pacific. This assertion is confirmed by Ireland’s tax incentives which have been recognized as key in attracting international investors over the past two decades. In recent years, evidence suggest that there has been growing tax rates and incentives influence the location decisions of investors within established regional economic zones to promote trade, such as the European Union, North American Free Trade Area, and Association of Southeast Asian Nations. Similarly, in the United States incentives have play a decisive role in investor location decisions of foreign companies once the choices are narrowed down to a handful of sites with similar characteristics. So, is follows more accurate to say that tax incentives have a direct relationship with investor decisions in setting up.

Ernst & Young noted that, another problem with incentive measures relates to the cost and difficulty of administering them effectively

| [4] | Ernst & Young, 1994. The impact of tax incentives on investment location. London: Ernst & Young International. |

[4]

. Incentive regimes generally impose a large administrative burden, with political inclinations, so they must be more than marginally effective to cover the costs of their implementation and produce a net benefit. These regimes result in delay and uncertainty for investors, which can increase the cost of investment. They have also led to significant corruption, and political attacks as investors are tagged with particular regime and effectively screened out desirable investments, and undermined sound policymaking and the development of competitive markets.

| [19] | Morisset, J., 2003. Tax incentives: Using tax incentives to attract foreign direct investment. Public Policy for the Private Sector Note No. 250. Washington, D. C.: World Bank. |

[19]

.

2.4. Historical Antecedent of Tax Incentives in Ghana

According to

| [9] | Gocking, R. S., 2005. The history of Ghana. Westport, CT: Greenwood Press. |

[9],

the historic background of Tax incentives in Ghana started with the regulatory framework of the GIPC Act, 2013 (Act 865) and the tax policy adjustments under the Economic Recovery Programme (ERP)

. The Tax incentives framework operated within an investment climate in Ghana backed by full-fledged policies initiated by the government for it to work effectively. The government came up with a clear vision and objectives in meeting its policy goals. The investment climate at any particular time determine, the suitable tax incentives offered for investors and this was clearly catered for in the policy framework. According to

the main FDI regulatory framework in Ghana is the GIPC Act which requires all foreign companies in which there is foreign participation register with the GIPC.

Ghana open up is economy under the ERP by liberalizing trade for effective development by overhauling its tax system as part of its sweeping reforms in 1983. A number of fiscal policy incentives to enhance trade were introduced to direct capital into the country and since then, successive governments have not turned back to intensify this policy through legislative reforms and continued to offer fiscal incentives to drive private sector participation in the economy. Investors are guaranteed all the general tax incentives provided for under the law, but special tax incentives may be available to investors depending on the sectors of the economy.

| [14] | International Monetary Fund (IMF), 2018. Ghana: 2018 Article IV Consultation-Press Release; Staff Report; and Statement by the Executive Director for Ghana. IMF Country Report No. 18/XX. Washington, D. C.: IMF. |

[14]

. According to

| [2] | Asafu-Adjaye, J., 2018. Tax incentives and foreign direct investment in Ghana: 1985-2017. Accra: Ghana Institute of Fiscal Studies. |

[2]

, the evidence of tax incentives on investment in Ghana from 1985 to 2017. It offers an outline of the effects of series of legislative reforms on FDI in Ghana, starting from the introduction of the ERP in 1983, continuing to the period of global decline of FDI in 2001.

2.5. Tax Incentives

Giving Tax incentives to investors presents an exceptions to the countries general tax regime to direct investors into the country and into specific sectors to promote development. Tax incentives are designed to induce investors by increasing the rate of return on their investment and to also reduce the costs or risks investors face in promoting their business in the country. It is important for tax incentives not to only favour foreign investors at the expense of local business but should be available to domestic investors to benefit from such policies to promote local business too. The reason is that domestic investors are likely to be operating in fundamental sectors of the economy which promote coordinated development that brings positive impact to promote development, as against FDI which may be located in sectors that are not key to the economy. Notwithstanding, tax incentives may be designed to focus on the attraction of FDI to diversify the export base of a country. Generally, tax incentives can be classified into two broad categories based on their mode of operation cost-based tax incentives and profit-based tax incentives.

2.5.1. Cost-based Tax Incentives

According to Klemm

Cost-based tax incentives operate to reduce the cost of investment which enables investors to get the right equipment’s for set-up. Normally, exemptions from import duties are targeted to reduce the cost of plant, machinery and equipment, mainly meant to support production in an economy through tax holidays. Incentives that reduce the cost of production present a benefit to investors by taking advantage to invest their capital in the country. This is targeted for long-term investments in industries, like mining, oil and gas, in which returns are realized over a longer period.

| [31] | Zolt, E. M., 2015. Tax incentives and tax base protection issues. In: United Nations, Handbook on Selected Issues in Protecting the Tax Base of Developing Countries, pp. 99-140. |

[31]

.

2.5.2. Profit-based Tax Incentives

Profit-based tax incentives are better suited to attract short-term investments. Profit-based incentives such as tax holidays are offered to investors engaged in short-term, low capital investments, which generates quick returns. They are usually granted during the early years of an investment, and their benefits are designed to be realized only in the short-term. Profit-based incentives have their benefits accruing as soon as the firm begins to make profits. This makes them suitable for short-term projects with low upfront investment costs, and quick returns.

| [20] | Morisset, J. and Pirnia, N., 2001. How tax policy and incentives affect foreign direct investment: A review. Washington, D. C.: World Bank. |

[20]

.

2.6. Tax Incentives Framework Design

The design framework of tax incentives is categorized into six (6) different types mostly dependent on the investment type and governance structure of the host country. They are: tax holidays, accelerated depreciation, special size or scale tax incentives, special sectors, and special regions or zones.

2.6.1. Tax Holidays

Tax holidays consists of profit-based incentive with complete or limited exemptions from tax obligations from firms. New firms are allowed a period of time during which the burden of income taxation is waived to give a breather on their investment actions. A tax holiday may take the form of a complete exemption from profits tax (and other taxes), a reduced rate of tax or a combination of the two for a period. Although tax holidays are to encourage investment by reducing or eliminating the tax liability of firms over the holiday period, they generally deny firms deductible expenses, such as, depreciation costs, and interest tax deductions, to partly compensate for the loss in revenue resulting from the exemption.

2.6.2. Capital Allowance Incentives

Accelerated depreciation or capital allowance enables investors to deduct the cost of their expenses especially on equipment’s more quickly than they decline in value. These incentives come in the form of deductions or credits which reduces the taxable income of the firm. Tax credits reduce the outstanding taxes to be paid and therefore are worth the same to taxpayers regardless of their tax rate assigned under the tax laws of the land. Accelerated capital allowance are cost-targeted incentives which provide tax benefits over and above the depreciation allowed for the asset. Investment allowances may apply to all forms of capital investment, or may be limited to only plant and machinery, and may grant in addition to, or in place of the normal depreciation allowance.

The advantages with investment tax allowances are that they target the incentive at the desired activity, are tied to current capital spending, and may result in lower revenue foregone, than tax holidays.

| [11] | Holland, D. and Vann, R., 1998. Tax incentives and foreign direct investment: A global survey. Paris: OECD. |

[11]

.

2.6.3. Special Size or Scale Tax Incentives

Special size or scale tax incentives grant investments with assets valued above a threshold amount, or which create a minimum number of new jobs, and a negotiated package of tax incentives. They may be cost- or profit-based and are suitable for countries or regions that need major transformational investments, financial or technical ease ups in their economies. According to

| [7] | Ghana Investment Promotion Centre (GIPC), 2019. Annual Report 2019. Accra: GIPC. |

[7]

In Ghana, for example, an investor making investment worth over USD 50 million in one of the identified key sectors, including, energy, infrastructure, and railways, can negotiate tax concessions on import duties and other development costs. One other advantage of this approach is that, because it limits incentives to large investments, which may be few, governments may be able to monitor their use at minimal cost.

| [20] | Morisset, J. and Pirnia, N., 2001. How tax policy and incentives affect foreign direct investment: A review. Washington, D. C.: World Bank. |

[20]

.

2.6.4. Import Duty or Tariff Exemptions

Import duty or tariff exemptions can be used to reduce or eliminate tariffs on imported capital equipment and spare parts for qualifying investment projects. The effect is to reduce the cost of investment and boost new technology and machinery to support the industrial base of a country. The advantage of import duty or tariff exemptions schemes is that import duty relief may be necessary to attract investment in capital intensive projects, such as, mining investment, because it helps reduce cost of inputs, and other financial risks, considering the substantial amount of capital investment that may be required in such projects. Charging import duties may reduce the incentive to inflate the cost of imported equipment and machinery, granting a waiver.

| [26] | United Nations Conference on Trade and Development (UNCTAD), 2000. Tax incentives and foreign direct investment: A global survey. New York and Geneva: UNCTAD. |

[26]

.

2.6.5. Reduced CIT Rates

Table 1. Locational incentives for manufacturing businesses.

Location | Tax rate |

Location within Accra and Tema | 25% |

Location in regional capitals of Ghana | 18.50% |

Location in free zone enclave after 10 years tax holiday | 15% |

Location elsewhere in Ghana | 12.5% |

Source: Ghana Revenue Authority; 2021

A reduced CIT rate are set as an exception to the general tax regime in a country, in order to attract FDI into specific sectors or regions to align sectoral or regional development agenda. It may be targeted at foreign investment which meet specified criteria, or it may be granted to particular industries as a whole.

| [26] | United Nations Conference on Trade and Development (UNCTAD), 2000. Tax incentives and foreign direct investment: A global survey. New York and Geneva: UNCTAD. |

[26]

.

2.7. Foreign Direct Investment (FDI)

Foreign Direct investment according to

| [23] | Organisation for Economic Co-operation and Development (OECD), 2008. Benchmark definition of foreign direct investment: Fourth edition. Paris: OECD Publishing. |

[23]

, is defines as incorporated or unincorporated enterprise in which a single foreign investor either owns 10 per cent or more of the ordinary shares or voting power of an enterprise or owns less than 10 per cent of the ordinary shares or voting power of an enterprise, yet maintains an effective voice in management. In simple terms, foreign direct investment (FDI) occurs when there is investment in a business entity by investors from another nation; cross border investment. A number of factors are being considered while determining foreign direct investment (FDI) destination, one of which is tax incentives.

2.8. Agro Processing Industry Landscape in Ghana

The agricultural sector remains pivotal in the Ghanaian economy by contributing largely to the Gross Domestic Product of the nation

| [5] | Feder, G., Murgai, R. and Quizon, J. B., 2003. Sending farmers back to school: The impact of farmer field schools in Indonesia. Review of Agricultural Economics, 26(1), pp. 45-62. https://doi.org/10.1111/1467-9353.00073 |

[5]

. The Agro Processing industry then has the potential to play a major socio-economic role and source of employment to the people of Ghana. However, despite the various contributions made by the agro-business sector, the sector is besieged with challenges thus limiting the productivity capacity of the sector.

| [15] | Kerali, H., 2018. World Bank Country Director for Ghana-Remarks on Agricultural Transformation. Accra: World Bank Ghana Office. |

[15]

the World Bank Country Director for Ghana, the agriculture sector has a potential to be one of the leading sectors for a more diversified economy and could be transformed to be an engine of growth and job creation. Agriculture is an important contributor to Ghana’s export earnings, and a major source of inputs for the manufacturing sector. It is also a major source of income for a majority of the population.

| [29] | World Bank, 2017. Enabling the Business of Agriculture 2017. Washington, D. C.: World Bank. Available at: https://eba.worldbank.org |

[29]

, reforms are needed to improve the quality and efficiency of regulatory systems that govern access to key agricultural factors such as seed, fertilizer, machinery, finance, markets, transport and information and communication technologies. Despite the challenges, the report cites key opportunities and policy options to transform agriculture through Agro processing

| [29] | World Bank, 2017. Enabling the Business of Agriculture 2017. Washington, D. C.: World Bank. Available at: https://eba.worldbank.org |

[29]

.

Ghana, like any other developing countries is a predominately raw material producing nation, with little investment in converting raw materials into finished commodities to guarantee higher exports earnings. The World Bank report indicates that, our country’s over-reliance on exportation of raw cocoa beans is depriving the country billions of dollars in the cocoa value chain. Government’s recent interest in industrial revolution through the one district one factory initiative with much emphasis on converting our abundance raw materials into finished goods with the Agro-processing industry as a pilot will contribute immensely to the growth of the industry.

However, there are several constraints that affect the establishment of Agro processing industry notably are high cost of credit, non-regulated land tenure system, stringent regulatory standards. These factors tend to increase the cost of production especially during the formative period of its establishment. This phenomenon prolongs the period to breakeven and retards the profitability of industries. The persistent production losses witness by the sector makes it unattractive for investment

| [29] | World Bank, 2017. Enabling the Business of Agriculture 2017. Washington, D. C.: World Bank. Available at: https://eba.worldbank.org |

[29]

.

The Specific Objective of this paper is to evaluate how the provision of tax incentives promotes sustainability and growth of the Agro-Processing industry and to assess the various tax incentives given to foreign direct investment (FDI) in the Agro-Processing Industry.

4. Findings and Discussions

These findings present the results of the analysis performed on the data collected. The discussion is done in relation to the pertinent concepts and theories discussed in the review of literature. Constraints facing the establishment of agro processing industry, effect of tax incentive on the performance of the Agro Processing Industry, various tax incentives given to foreign direct investment (FDI) in the Agro Processing Industry had important role in attracting foreign direct investment (FDI) into Ghana’s Agro Processing Industry. In all, sixty (60) questionnaires were administered to targeted respondents appropriately with fifty-one (51) valid, representing 85% response rate. Out of this number, thirty-five (35) representing 68.6% were managers of (HPW Fresh & dry Ghana Limited.) while sixteen (16), representing 31.20%, were non-management staff. The 85% recovery rate of the questionnaires distributed for the study could be assumed to be representative enough to make enough conclusions on the study.

4.1. Summary of Financial Performance of the Agro Processing Industry (HPW Fresh & Dry Ghana Limited)

Table 2 shows the level of sales and profit of Agro processing company (HPW Fresh & Dry Ghana Limited) from 2014 up to 2019, where the sales and profit had been increasing year by year. Based on these results from their financial statements the financial performance of the Agro processing company looked good. As profitability is a measure of the amount by which a company's revenues exceeds its relevant expenses, the results reveal that an increase in the sales has raised profitability of the Agro processing industry during the study period. However, the Agro processing was able to perform in terms of profitability based on the 25% tax holidays enjoyed under the tax incentive package for Agro Processing Companies. This means that tax incentives influence the sales and profitability of the organization. The findings relate to the study carried out by

| [17] | Külter, H. and Demirgüneş, K., 2007. Effects of tax incentives on profitability and investment behavior of companies. Journal of Financial Research, 8(2), pp. 145-158. |

[17]

who point out that revenue and profitability of a company are affected by tax incentive.

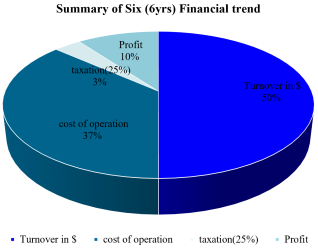

According to

Table 2, a six (6) years trend of Financial Summary was considered extensively for analysis. The summary compared sales turnover, operational cost, tax and profit for a period of six years. Sales grew exponentially from $6,765,146.07 in 2014 to $40,050,935.75 in 2019. Total sales for the six years period stood at $135,091,760.40 whiles total cost of operation was $98,599,914.97 and Profit before tax is $36,491,845.43 for the six years in operations representing 27% of sales turnover. A statutory corporate tax of 25% of sales turnover is $9,122,961.36 which is considered as tax to be paid in absence of tax concessions for a period of six years of operations as an Agro-Processing Company. However, considering the nature of the entity and location of business, HWP Fresh and Dry is allowed to pay only 1% as corporate tax for the first five years of operation and 10% subsequently. This resulted in the payment of concessional tax liability of $3,135,014.54 as against tax payment of $9,122,961.36 representing 8.59% of total profit for the six years of operations. This implies that HPW Fresh & Dry Ltd was profitable for the six years in operations due to about 16.41% tax incentive offered to support their fruitful operations and contribute meaningfully towards Ghana Gross Domestic Product and the level of jobs created along the value chain.

4.2. Summary of Finding and Analysis

To understand and appreciate the crucial role Tax Incentives plays in developing economies towards its profitability, sustainable growth and attracting foreign direct Investment especially in the Agro Processing Industry. Company Establishments have profited greatly because the tax incentive policies are adequately encouraging for foreign investments. According to our findings, total tax for the six years period was $9,122,961.36 whiles tax incentive and tax holidays tax was $3,135,014.54 giving as an accumulated Tax free of $5,987,946.82 representing 65.64% of accumulated Taxation (25%) of $9,122,961.36 for the six years of operation. This suggests that, tax incentive sufficiently aided HPW Fresh & dry Ltd for its early years of business commencement.

Figure 1. Summary of Six years Financial Trend.

In addition, there were other attributes which were discovered of being hindrance to Agro Processing Company operations. Access to raw materials, inadequate funds & high interest rate on lending capital and Environmental & Sustainable Compliance were the key hindrance to the growth and sustainability of Agro Processing Companies aside tax incentives. According to

| [7] | Ghana Investment Promotion Centre (GIPC), 2019. Annual Report 2019. Accra: GIPC. |

[7]

, only five (5%) of food products harvested in Ghana are processed. Therefore, from a health and nutrition perspective, Agro-processing has the potential to increase nutritional value for the population and increase food security, through a reduction in food spoilage and wastage. Processed foods will also ensure greater price stability on the world market and create market opportunities for exports, contributing to income securities particularly in rural communities, which are mostly engaged in farming. The development of the Agro-processing industry may also promote employment generation, contribute to enterprise development, diversification of rural economies, import substitution, among others. According to

| [24] | Quartey, P. and Darkwah, S. A., 2015. Agro-processing industry and its potential for job creation and value addition in Ghana. Accra: Institute of Statistical, Social and Economic Research (ISSER), University of Ghana. |

[24]

, Agro-processing is the most important sub-sector of the manufacturing sector, with food and beverages representing the largest component of processed commodities.

4.3. Conclusion

The study revealed that provision of tax incentives for Agro-processing industries as means to support the conversion of raw materials into finished goods for export to enhance export earnings will enormously attract both foreign and local investors in the sector. The provision of tax incentives through tax holidays, locational and entity-based tax concession will enable companies to breakeven early and be profitable in the earliest period. The lower tax rate offered to Agro-processing industries will reduce tax liability and optimize profitability to provide assurance to investors of returns of their investment. The perceived and guaranteed returns on investment will attract foreign direct investment for the Agro-processing industries.

Though tax incentives offered to the Agro processing sector are contributing to the sterling performance in the industry, but on the blind side, major problems like the depreciation of the Cedi and other micro-economic issues like cost of production, price determination and consumer choice, as well as limited access to credit, high interest rates and fluctuating exchange rates, high transportation costs, lack of support facilities and poor quality raw materials with its unreliable supply are significant issues that need to be tackled first in the bid to encourage the establishment of Agro-based industries due to 70% of the final product which are mandatory meant for export under the tax incentive regime of free zone category, continuous fall of our local currency create foreign exchange loses anytime profit is supposed to be repatriated back to Ghana as a plough back for operational activities. Lack of financial markets, failure to adapt to changes, and the failure to search out for prospective market niches followed closely. Emerging competitive environment and the changing customer satisfaction were regarded as the least significant problems faced in marketing Agro-based industries.

This research work clearly confirms that tax incentives are relevant to the performance, growth, development and continuous sustainability of Agro processing industry. However, most of the tax incentives that are available in the tax law are not fully enjoyed as being spelled out in their policy document but the industry players have to negotiate their way out and prove beyond other circumstance that they deserve such incentives. It is only the large taxpayers that enjoy most of the tax incentives. Tax incentives play a vital role in ensuring that Agro processing industries thrive because the government has made available tax holidays for pioneer companies, and the government also grants a number of general and industry specific incentives. Finally, for many Agro processing industry, the decision to remain informal is deliberate because of the cost and procedural burden of joining the formal sector out weight the benefit of staying in the informal sector. Informal sectors make large contributions to nation economies, in both human and financial terms. But being visible to government agencies and formal sector companies, they can be easily reached with capacity building improvement schemes. However, they cannot compete for business with larger companies and thus there is a need for governments to accelerate their growth by creating more enabling and engaging environment for them via appropriate tax incentives to enhance their sustainability and growth.

5. Recommendations

In the light of the findings and conclusions, we recommend some policy directions following from the study to address the establishment, production and marketing challenges associated with Agro-business in Ghana.

5.1. Export Led Approach to Agro-processing

Policy support for export led approach that ensures Agro-processing industries are incentivize to export more to earn more foreign exchange. A stable currency is needed to ensure such approach succeed to make them competitive in the mist of international trade boosted by the African Continental Free Trade Area (AfCFTA). This support can be tailored towards a central bank initiative to maintain stable currency through a regulatory framework that ensures that the country earns more foreign exchange into the country. Among other factors, the government can incentivize manufacturing companies to increase their export volumes and at the same time ensure that non-traditional exports are encouraged to increase the country’s balance of trade and earn more foreign exchange to strengthen the local currency. For example, concessions should be given by the central bank to Agro processing industries for lower interest rates and operating cost. This will entail HPW Fresh & Dry Ghana Ltd identifying the competitive forces in the local and international market, noting its strength and weaknesses and determining the means to create a competitive advantage for the institution.

5.2. Limited Access to Credit

Low access to credit could be partly addressed through the establishment financial institutions like ADB and EXIM Bank through a fair and non-political disbursement of support at the right time, right amount and with the right credit conditions at concessional rate for Agro-Processing Industries to be competitive and accelerate growth.

5.3. High Logistics Cost and Efficient Process

Efficient Airport operations that minimizes delays with its attendant high shipping charges could be addressed through a structured system that support trade facilitation for agro processing. In addition, space could be designated in the airport warehouses to augment speedily facilitation for shipping final products of Agro processing goods due to its short lifespan and shelve life. Assisted Custom desk can be created in the Agro processing factory to facility inspection and standards so that certain delays at the port of shipping can be reduced. If goods produced are checked and inspected by custom and standard officials at the factory, there could be easy facilitation and avoid delays due to airport inspections before the final product are shipped to their destined market for consumption.

5.4. Continuous Uninterrupted Power Supply

A stable uninterrupted power supply is key for Agro-based industries to be efficient in the delivery of quality products, and to sustain employment of young people. Some Resourceful Energy companies can be consulted to build, operate and transfer Power Plants solely dedicated for delivery of power to HPW Fresh & Dry Company Ltd. Energy Company like Genser has similar projects for Unilever Ghana and several mining Companies in Ghana.

5.5. Limitation of the Study

Generally, the objective is to assess the effects of tax incentive in attracting foreign direct investments in the Agro-processing sector and evaluating the various tax incentives and its impact on performance, growth and sustainability of the Agro-processing sector. This requires an assumption to be made on the amount of investment without the tax incentive Programme, and the amount of revenue foregone due to the award of tax incentive by government. It was practically difficult to distinguish investments influenced by the tax incentive as investors do not solely based their investment decisions on one factor.

It is important not to generalise the outcomes to other Manufacturing sector although, the available the study draws on data and other information from other Agro-procession for comparative analysis, the study focused more on the tax incentive regimes in Agriculture sector and narrow it to the Agro-processing.

Due to the limited availability of data, much of the review of the impact of tax incentives on foreign direct investments was based on existing research findings, and analysis of secondary data. Time and resource constraints limit the scope of the study hence, was limited to Agro- processing industry and more specifically, the HWP Fresh and DRY Company Limited. Key respondents were reluctant to provide relevant information to assist the study and some respondents failed to return the completed questionnaire and withheld significant information which would greatly influence the outcome of the project.