It measures the risk that a system or company fails to maintain its elf over time. In this article, we provide an approximation of the probability of ruin at the infinite horizon whose inter-arrivals of claims follow the Hawks process and the amount of claims follows the Weibull distribution, with independence between these two processes. Using the Finite Volume Method is a numerical approach for solving partial differential equations. It consists of dividing the computational domain into discrete volumes and applying local approximations to obtain a global solution. This method can be used to estimate complex probabilities., a stochastic model with variable memory, it is possible to capture the temporal dependence of events. This allows us to analyze situations where the past directly influences the probability of occurrence of future events. This approximation is done using the finite volume method, which is a numerical approach for solving partial differential equations. It consists of dividing the computational domain into discrete volumes and applying local approximations to obtain a global solution. This method can be used to estimate complex probabilities. This is the case in our work; which consists of solving a second-order integro-differential equation, two cases of which are considered on the Weibull parameter η: if η=1, then the distribution of claim amounts is exponential. On the other hand, if η≥2, then the results lead us to a system of linear equations for which we use the finite volume method to obtain a numerical solution.

| Published in | American Journal of Theoretical and Applied Statistics (Volume 14, Issue 4) |

| DOI | 10.11648/j.ajtas.20251404.11 |

| Page(s) | 118-125 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Finite Volume Method, Integro-differential Equation, Probability of Ruin, The Finite Volume Method

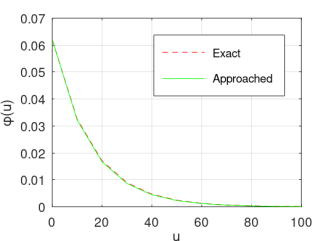

0 | 0.0600 |

10 | 0.0358 |

20 | 0.0183 |

30 | 0.0108 |

40 | 0.0056 |

50 | 0.0028 |

60 | 0.0015 |

70 | 0.0005 |

80 | 0.0003 |

| [1] | Souleymane BADINI, Frédéric BERE, Delwendé bdoul-Kabir KAFANDO, 2024. Integro-differential equation and Laplace transform of the infinite-horizon probability of ruin of a variable-memory counting process (Hawkes process). Contemporary Mathematics. 1-16 p. |

| [2] | Hawkes, AG, 1971. Specters of a self-exciting and mutually exciting process. Biometry. 58(1), 83-90 p. |

| [3] | LAMIEN K., 2017. Numerical resolution of some hyperbolic conservation laws using the moving grid method under the finite volume method. Unique doctoral thesis, applied mathematics option, specialty numerical analysis and simulation. UFR/SEA, University Ouaga 1 Pr Joseph KI-ZERBO, Burkina Faso. 131 p. |

| [4] | LAMIEN K., SOME L. and OUEDRAOGO M., 2020. Using an adaptive mesh hig order finite volume method to solve three hyperbolic Conservation laws with diffusion or source term, African Mathematical Annals, (8): 113-124 p. |

| [5] | SOME L., 2007. Mobile grid method under the line method for the numerical resolution of partial differential equations modeling evolutionary phenomena. Unique doctoral thesis, option applied mathematics, specialty numerical analysis and computer science., UFR/SEA, University of Ouagadougou, Burkina Faso. 161 p. |

| [6] | An Analysis of finite Difference and Finite volume Formulations of Conservation Laws (Review Article). M. VINOKUR, Journal of computational Physics 81, 1-52, 1989. |

| [7] | A 3-D Finite Volume numerical model of compressible multicomponent flow for fluid-structure interaction applications. A. SALA, F. CASADEI and A. SORIA, IV Congreso de métodos Numéricos en Ingeniera, Seville, Espagne, 1999. |

| [8] | P. Blanc, R. Eymard, R. Herbin, A staggered finite volume scheme on general meshes for the gene ralized Stokes problem in two space dimensions, Int. J. Finite Volumes, 2(2005), n 1, 31 pp. |

| [9] | A. Ern, J. L. Guermond, Finite elements: theory, applications, implementation, Mathematics and Applications, Springer Berlin Heidelberg, 2002. |

| [10] | R. Eymard, R. Herbin, A staggered finite volume scheme on general meshes for the Navier-Stokes equations in two space dimensions, Int. J. Finite Volumes, 2(2005), n 1, 19 pp. |

| [11] | I. Mishev, Finite Volume Methods on Voronoï Meshes, Num. Meth. P. D. E, vol. 14, p. 193-212, 1998. |

| [12] | J. M. Sánchez and F. Baltazar-Larios. Approximations of the ultimate ruin probability in the clas sical risk model using the banach's fixed-point theorem and the continuity of the ruin probability. Kybernetika, 58(2), 2022. |

| [13] | D. J. Santana and L. Rincón. Approximations of the ruin probability in a discrete time risk model. Modern Stochastics: Theory and Applications, 7(3), 2020. |

| [14] | A. Quarteroni, A. Valli, Numerical Approximation of Partial Differential Equations, Springer Berlin Heidelberg, 2009. |

| [15] | D. A. Hamzah, T. S. A. Siahaan, and V. C. Pranata. Ruin probability in the classical risk process with weibull claims distribution BAREKENG: J. Math. & App., 17(4): 2351-2358. |

APA Style

Badini, S., Bere, F. (2025). Weibull Distribution and Approximation, by the Finite Volume Method, of the Ultim Ruin Probability Constructed from the Hawkes Variable Memory Process. American Journal of Theoretical and Applied Statistics, 14(4), 118-125. https://doi.org/10.11648/j.ajtas.20251404.11

ACS Style

Badini, S.; Bere, F. Weibull Distribution and Approximation, by the Finite Volume Method, of the Ultim Ruin Probability Constructed from the Hawkes Variable Memory Process. Am. J. Theor. Appl. Stat. 2025, 14(4), 118-125. doi: 10.11648/j.ajtas.20251404.11

@article{10.11648/j.ajtas.20251404.11,

author = {Souleymane Badini and Frédéric Bere},

title = {Weibull Distribution and Approximation, by the Finite Volume Method, of the Ultim Ruin Probability Constructed from the Hawkes Variable Memory Process

},

journal = {American Journal of Theoretical and Applied Statistics},

volume = {14},

number = {4},

pages = {118-125},

doi = {10.11648/j.ajtas.20251404.11},

url = {https://doi.org/10.11648/j.ajtas.20251404.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ajtas.20251404.11},

abstract = {It measures the risk that a system or company fails to maintain its elf over time. In this article, we provide an approximation of the probability of ruin at the infinite horizon whose inter-arrivals of claims follow the Hawks process and the amount of claims follows the Weibull distribution, with independence between these two processes. Using the Finite Volume Method is a numerical approach for solving partial differential equations. It consists of dividing the computational domain into discrete volumes and applying local approximations to obtain a global solution. This method can be used to estimate complex probabilities., a stochastic model with variable memory, it is possible to capture the temporal dependence of events. This allows us to analyze situations where the past directly influences the probability of occurrence of future events. This approximation is done using the finite volume method, which is a numerical approach for solving partial differential equations. It consists of dividing the computational domain into discrete volumes and applying local approximations to obtain a global solution. This method can be used to estimate complex probabilities. This is the case in our work; which consists of solving a second-order integro-differential equation, two cases of which are considered on the Weibull parameter η: if η=1, then the distribution of claim amounts is exponential. On the other hand, if η≥2, then the results lead us to a system of linear equations for which we use the finite volume method to obtain a numerical solution.},

year = {2025}

}

TY - JOUR T1 - Weibull Distribution and Approximation, by the Finite Volume Method, of the Ultim Ruin Probability Constructed from the Hawkes Variable Memory Process AU - Souleymane Badini AU - Frédéric Bere Y1 - 2025/07/04 PY - 2025 N1 - https://doi.org/10.11648/j.ajtas.20251404.11 DO - 10.11648/j.ajtas.20251404.11 T2 - American Journal of Theoretical and Applied Statistics JF - American Journal of Theoretical and Applied Statistics JO - American Journal of Theoretical and Applied Statistics SP - 118 EP - 125 PB - Science Publishing Group SN - 2326-9006 UR - https://doi.org/10.11648/j.ajtas.20251404.11 AB - It measures the risk that a system or company fails to maintain its elf over time. In this article, we provide an approximation of the probability of ruin at the infinite horizon whose inter-arrivals of claims follow the Hawks process and the amount of claims follows the Weibull distribution, with independence between these two processes. Using the Finite Volume Method is a numerical approach for solving partial differential equations. It consists of dividing the computational domain into discrete volumes and applying local approximations to obtain a global solution. This method can be used to estimate complex probabilities., a stochastic model with variable memory, it is possible to capture the temporal dependence of events. This allows us to analyze situations where the past directly influences the probability of occurrence of future events. This approximation is done using the finite volume method, which is a numerical approach for solving partial differential equations. It consists of dividing the computational domain into discrete volumes and applying local approximations to obtain a global solution. This method can be used to estimate complex probabilities. This is the case in our work; which consists of solving a second-order integro-differential equation, two cases of which are considered on the Weibull parameter η: if η=1, then the distribution of claim amounts is exponential. On the other hand, if η≥2, then the results lead us to a system of linear equations for which we use the finite volume method to obtain a numerical solution. VL - 14 IS - 4 ER -

Department of Mathematics, Université Joseph KI ZERBO, Ouagadougou, Burkina Faso

Department of Mathematics, Ecole Normale Supérieure, Ouagadougou, Burkina Faso

Information