1. Introduction

Sustainability reporting refers to the structured disclosure of a firm’s environmental, social, and governance (ESG) policies, practices, risks, and outcomes to help stakeholders evaluate how the firm creates value and manages non-financial risks alongside profitability

| [14] | Global Reporting Initiative. (2024). About GRI / GRI Standards. |

| [27] | KPMG. (2024). The move to mandatory reporting: Survey of sustainability reporting 2024. |

[14, 27]

. Over the past decade, ESG reporting has shifted from largely voluntary narrative CSR statements toward investor-oriented disclosure linked to enterprise risk management, cost of capital, and long-run competitiveness

| [49] | Wooldridge, J. M. (2016). Introductory econometrics: A modern approach (6th ed.). Cengage Learning. |

[49]

. This shift is occurring alongside the expansion of sustainable finance: the Global Sustainable Investment Alliance reported US$30.3 trillion in sustainable investing assets globally

| [16] | Global Sustainable Investment Alliance. (2022). Global sustainable investment review 2022. |

[16]

. Standard-setting has also accelerated. A major milestone was the issuance of IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures) by the International Sustainability Standards Board in June 2023, aimed at creating a global baseline for sustainability-related financial disclosures in capital markets

| [19] | IFRS Foundation/International Sustainability Standards Board. (2023). Introduction to the ISSB and IFRS sustainability disclosure standards. |

| [20] | IFRS Foundation/International Sustainability Standards Board. (2023, June 26). ISSB issues inaugural global sustainability disclosure standards—IFRS S1 and IFRS S2. |

[19, 20]

. In parallel, the GRI Standards remain widely used for impact-oriented sustainability reporting, with KPMG’s 2024 survey highlighting their continued dominance among reporting firms globally

| [14] | Global Reporting Initiative. (2024). About GRI / GRI Standards. |

| [27] | KPMG. (2024). The move to mandatory reporting: Survey of sustainability reporting 2024. |

[14, 27]

.

Together, these developments signal rising expectations that listed companies provide credible ESG information to support efficient pricing of risk and capital allocation.

The ESG–financial performance relationship is commonly explained through complementary theories of the firm. From a stakeholder view, disclosures that demonstrate responsiveness to employees, communities, regulators, and investors can reduce conflict, protect reputation, and secure access to critical resources channels that can translate into stronger performance. Empirically, however, findings are mixed, partly because ESG is measured differently across studies (ratings vs disclosure indices), performance is proxied differently (accounting vs market measures), and results depend on endogeneity controls and institutional context. Large evidence syntheses still tend to find that ESG is more often positively associated with financial performance and downside-risk protection, but also emphasize heterogeneity across markets and methodologies

| [23] | Khan, M. A. (2022). ESG disclosure and firm performance: A bibliometric and meta-analysis. Research in International Business and Finance, 61, 101668. |

| [49] | Wooldridge, J. M. (2016). Introductory econometrics: A modern approach (6th ed.). Cengage Learning. |

[23, 49]

. The implication is that ESG disclosure can be value-relevant, but its payoffs may be contingent on enforcement quality, firm strategy, industry materiality, and whether ESG investments generate operational efficiencies or simply add compliance and reporting costs.

Within ESG, the environmental pillar has become especially salient as climate risks increasingly affect firm cash flows through physical disruption, transition policy, and reputational pressure

| [21] | Intergovernmental Panel on Climate Change. (2023). Climate change 2023: Synthesis report (AR6). |

[21]

. Environmental disclosure may enhance performance if it reflects real eco-efficiency gains and innovation that reduce waste and costs, consistent with the argument that well-designed environmental responses can support competitiveness

| [41] | Porter, M. E., & van der Linde, C. (1995). Toward a new conception of the environment-competitiveness relationship. Journal of Economic Perspectives, 9(4), 97–118. |

[41]

. Yet environmental reporting can also impose short-run costs (data systems, audits, compliance spending) and heighten scrutiny, producing negative or insignificant contemporaneous performance effects in some settings. The social pillar covering labor practices, human capital, product responsibility, and community relationships can strengthen productivity and stakeholder loyalty, but it may also be viewed as costly if initiatives are poorly targeted or weakly integrated into business strategy. Governance disclosure, meanwhile, is often expected to strengthen performance by signaling stronger oversight and reducing agency costs, though the credibility of governance reporting depends on whether disclosures represent substantive practices rather than symbolic “box-ticking.”

A key issue motivating newer research is that ESG reporting does not operate in isolation; it interacts with firm size in ways that can shape both ESG disclosure levels and their performance consequences. First, size is strongly related to disclosure capacity and visibility: larger firms typically face greater stakeholder scrutiny and have more resources for ESG data production, reporting systems, and assurance.

| [10] | Drempetic, S., Klein, C., & Zwergel, B. (2020). The influence of firm size on the ESG score: Corporate sustainability ratings under review. Journal of Business Ethics, 167(2), 333–360. |

[10]

show that ESG ratings can be systematically influenced by firm size and data availability. raising questions about comparability between large and small firms and implying that observed ESG–performance links may partly reflect scale-related reporting capacity rather than “true” sustainability performance. Second, firm size can condition the economic consequences of ESG. Evidence suggests ESG disclosure effects may differ across size strata

| [29] | Minutolo, M., Kristjanpoller, W., & Stakeley, J. (2019). Exploring environmental, social, and governance disclosure effects on firm performance. |

[29]

, with some studies finding stronger ESG–performance relationships among smaller firms (where ESG information can reduce information asymmetry more sharply) and different patterns among large firms (where ESG is expected and thus less differentiating. Third and central to this study firm size may act as a mediating mechanism through which ESG disclosure affects performance. ESG disclosure can influence financing conditions and stakeholder trust, which may ease constraints on investment and growth; one recent study documents that ESG disclosure can increase firm value by alleviating financing constraints

| [5] | Chen, Z., [et al.]. (2024). Does ESG information disclosure increase firm value? The mediation role of financing constraints. Journal of Corporate Finance. |

[5]

, indicating a financing channel through which firms can expand capacity (and potentially scale). It is therefore theoretically plausible that ESG disclosure affects firm performance not only directly (via efficiency, risk management, governance quality) but also indirectly by shaping firm scale, and then performance.

Regionally, sustainability reporting in African capital markets has expanded but remains uneven across countries, reflecting differences in enforcement, investor composition, and disclosure infrastructure. Stock exchanges have increasingly become policy actors in ESG adoption through guidance and listing expectations. The UN Sustainable Stock Exchanges (SSE) initiative maintains an ESG guidance database that documents this diffusion of exchange-led disclosure guidance across markets

| [47] | Whelan, T., Atz, U., Van Holt, T., & Clark, C. (2021). ESG and financial performance: Uncovering the relationship by aggregating evidence from 1,000+ studies published between 2015–2020. NYU Stern Center for Sustainable Business & Rockefeller Asset Management. |

[47]

. In Africa, partnerships between the Global Reporting Initiative and the African Securities Exchanges Association have aimed to strengthen ESG integration and disclosure capacity across member exchanges, supporting market-level adoption of sustainability reporting practices

| [15] | Global Reporting Initiative. (2025). Partnership to advance ESG integration in African capital markets. |

[15]

.This regional movement matters because emerging markets often face higher information asymmetry and risk premier; credible ESG disclosure can be a tool for improving transparency and investor confidence, potentially influencing both access to capital and firm performance.

In Kenya, ESG reporting has gained urgency due to climate vulnerability, governance reform pressures, and the role of the capital market in mobilizing long-term finance. A landmark step was the publication of the Nairobi Securities Exchange ESG Disclosures Guidance Manual in November 2021

| [32] | Nairobi Securities Exchange. (2021). ESG disclosures guidance manual (November 2021). |

[32]

, developed with technical support from organizations including GRI and ASEA, to guide listed firms on collecting and disclosing ESG information in a more consistent and internationally aligned. Kenya’s regulatory architecture also emphasizes governance through the Capital Markets Authority Code of Corporate Governance Practices for Issuers of Securities to the Public (2015), which sets governance expectations for issuers and reinforces transparency and accountability norms

| [3] | Capital Markets Authority. (2015). Code of corporate governance practices for issuers of securities to the public, 2015 (Code-8). |

[3]

. These developments indicate that ESG disclosure is increasingly institutionalized in the Kenyan listed-firm environment, making the ESG–performance question practically important.

At the same time, recent market indicators illustrate performance pressures and volatility in the Kenyan equities market. The NSE’s annual report shows that equity market turnover declined in 2023 relative to 2022 (partly attributed to price erosion), signaling weakening trading value despite activity in volumes

| [33] | Nairobi Securities Exchange. (2023). Integrated report & financial statements (Annual report 2023). |

[33]

. Such conditions elevate the relevance of risk disclosure, governance credibility, and investor confidence areas directly connected to ESG reporting quality. In markets where investor sentiment is fragile, ESG disclosures can either reduce uncertainty (if credible and decision-useful) or be discounted (if symbolic or inconsistent), which helps explain why empirical results may vary across settings and periods.

The study is organized as follows. Section 2 reviews prior literature on the relationship between ESG sustainability reporting and firm financial performance, with particular emphasis on the mediating role of firm size, and identifies the key gaps that motivate the study in the Nairobi Securities Exchange (NSE) context. Section 3 describes the data sources, measurement of variables (ESG disclosure pillars, firm size, and financial performance indicators), and the empirical methods applied, including the mediation framework. Section 4 presents the empirical results and relevant diagnostic tests and robustness checks. Section 5 concludes by summarizing the main findings and outlining implications and recommendations.

1.1. Objective of the Study

The general objective of this study is to examine the effect of sustainability reporting on the financial performance of firms, and to determine whether firm size significantly mediate the relationship between sustainability reporting and financial performance.

1.2. Specific Objective

To examine whether firm size mediate the relationship between sustainability reporting and financial performance.

1.3. Research Hypothesis

H₀1: Firm size has no significant effect on the financial performance of firms.

H₀2: Firm size does not significantly mediate the relationship between sustainability reporting and financial performance.

2. Theoretical Review

2.1. The Triple Bottom Line (TBL) Theory

The Triple Bottom Line (TBL) theory, proposed by

| [12] | Elkington, J. (1997). Cannibals with forks: The triple bottom line of 21st century business. Capstone. |

[12]

, expands the traditional view of corporate performance by emphasizing that firms should be evaluated not only on their financial outcomes but also on their social and environmental impacts. The theory argues that sustainable business success requires a holistic approach in which profit, people, and the planet are treated as equally important dimensions of performance. Within this perspective, sustainability reporting provides a structured means through which firms communicate their economic, social, and environmental activities to stakeholders, thereby demonstrating accountability and long-term value creation beyond short-term profitability

| [12] | Elkington, J. (1997). Cannibals with forks: The triple bottom line of 21st century business. Capstone. |

| [44] | Suttipun, M. (2021). The influence of board composition on environmental, social and governance (ESG) disclosure of Thai listed companies. International Journal of Disclosure and Governance, 18(4), 391–402. |

[12, 44]

.

The theory assumes that firms operate within a broader social and ecological system and that long-term financial performance is influenced by how well organizations manage relationships with stakeholders and natural resources. It presumes that responsible environmental and social practices can reduce risks, enhance corporate reputation, and strengthen stakeholder trust, which may ultimately translate into improved financial outcomes. TBL theory also assumes that transparent sustainability reporting enables stakeholders to assess firms’ commitment to sustainable development and encourages firms to align managerial decisions with long-term sustainability objectives.

Despite its conceptual appeal, TBL theory has attracted criticism, particularly regarding its lack of clear measurement standards and operational clarity. Critics argue that the theory does not provide precise guidelines for balancing or quantifying economic, social, and environmental performance, making comparisons across firms difficult. Furthermore, there is concern that sustainability reporting under the TBL framework may become largely symbolic, allowing firms to engage in impression management rather than substantive sustainability practices.

| [35] | Norman, W., & MacDonald, C. (2004). Getting to the bottom of “triple bottom line”. Business Ethics Quarterly, 14(2), 243–262. |

[35]

contend that such ambiguity can weaken the theory’s practical relevance and undermine the credibility of reported sustainability outcomes.

The Triple Bottom Line theory is relevant to this study as it underpins the examination of sustainability reporting as a multidimensional construct that extends beyond financial disclosure. By linking environmental, social, and governance reporting to financial performance, the theory supports the argument that sustainability practices can contribute to long-term firm value. Additionally, the inclusion of firm size as a mediating variable is consistent with TBL theory, as larger firms often face greater stakeholder scrutiny and possess more resources to implement and disclose sustainability initiatives. Thus, the theory provides a useful framework for understanding how sustainability reporting may influence financial performance across firms of different sizes.

2.2. Empirical Review

2.2.1. Environmental Reporting and Financial Performance

Khan synthesised the fast-growing ESG disclosure literature (2012–2022) using bibliometric techniques and meta-regression, concluding that the ESG–performance relationship remains empirically contested because studies differ widely in ESG measurement approaches, performance proxies (accounting vs market), and endogeneity controls

| [23] | Khan, M. A. (2022). ESG disclosure and firm performance: A bibliometric and meta-analysis. Research in International Business and Finance, 61, 101668. |

[23]

. In a more recent and broader meta-analytic synthesis,

| [53] | Orodho, A. J. (2005). Elements of education and social science research methods. Nairobi: Masola Publishers. |

[53]

analysed 95 papers (60,247 firm-level observations) and reported that ESG disclosure is positively associated with firm performance overall, with environmental disclosure showing “pronounced” positive effects and consistent reductions in cost of capital. These global reviews imply that environmental reporting is most likely to matter financially when it improves capital market perceptions (risk, transparency, downside protection) and/or reduces financing costs, but also highlight that results depend strongly on context and measurement.

From an African and emerging-market perspective, examined listed firms on the Nairobi Securities Exchange (NSE) over 2011–2015 using a manually scored ESG index (58 disclosure items) and two-stage panel least squares to address endogeneity concerns. They found that ESG disclosure is positively associated with stock liquidity and firm value (Tobin’s Q), but also reported evidence of a negative association between ESG disclosures and (accounting-based) financial performance suggesting potential short-run cost burdens or implementation trade-offs even when market-based outcomes improve. This study is important for the Kenyan setting because it separates “capital market” channels (liquidity/value) from “profitability” channels, indicating that environmental (and broader ESG) reporting may first pay off through information-environment improvements before (or even without) boosting near-term profitability.

Focusing specifically on environmental disclosure,

| [26] | King’wara, R., Magali, J., & Mohamed, S. (2020). Environmental disclosure and financial performance of firms in Kenya: A stakeholder approach. Research Journal of Finance and Accounting, 11(14), 52–63. |

[26]

used panel data for NSE firms and measured environmental disclosure through quantitative content analysis of annual reports (environmental data 2007–2015, financial performance 2008–2016 with a lag structure). They found a statistically significant positive relationship between environmental disclosure and return on assets (ROA), but not with return on equity (ROE) or Tobin’s Q, and interpreted the overall pattern as “mixed/neutral” evidence on whether environmental disclosure improves financial performance. Methodologically, the study illustrates a common finding in environmental reporting research: accounting returns (ROA) may be more responsive to operational efficiencies and stakeholder relations than market-based measures, especially in markets where ESG information is still thinly priced or inconsistently disclosed.

At the disclosure–market microstructure interface, Mathuva and colleagues’ Kenya-focused work on environmental reporting and market outcomes (e.g., liquidity) further supports the argument that environmental reporting can create value indirectly by reducing information asymmetry and improving trading conditions, even when profitability effects are weak or lagged. Taken together, the Kenyan evidence suggests that environmental reporting may contribute to performance through (i) operational efficiency narratives and risk management (raising ROA in some contexts), and (ii) market-based channels such as liquidity and valuation yet profitability benefits are not guaranteed, and may depend on the credibility, comparability, and materiality of environmental disclosures.

Based on the theoretical and empirical reviews, we formulate the following hypotheses.

2.2.2. Social Reporting and Financial Performance

Corporate social performance–financial performance relationship has been tested

| [26] | King’wara, R., Magali, J., & Mohamed, S. (2020). Environmental disclosure and financial performance of firms in Kenya: A stakeholder approach. Research Journal of Finance and Accounting, 11(14), 52–63. |

[26]

. Using a large sample the invetigation reported significant associations between a social performance index and profitability outcomes (e.g., ROA/return on sales), reinforcing the argument that stronger stakeholder relations and social performance can coincide with superior financial outcomes.

| [38] | Orlitzky, M., Schmidt, F. L., & Rynes, S. L. (2003). Corporate social and financial performance: A meta-analysis. Organization Studies, 24(3), 403–441. |

[38]

provided one of the most cited meta-analytic syntheses of this relationship (52 studies; 33,878 observations), concluding that corporate social responsibility/social performance is, on average, positively associated with corporate financial performance, though effect sizes vary depending on how both CSR and performance are measured. Complementing this, reviewed the CSR–financial performance debate and highlighted persistent methodological inconsistencies (measurement and model specification) as a key reason why empirical findings sometimes conflict. These foundational works frame social reporting as potentially value-relevant, but also warn that research design and proxy choice can flip conclusions.

In capital-market-focused CSR disclosure research, Dhaliwal and colleagues showed that nonfinancial/CSR disclosure can improve the information environment and reduce financing frictions. For example,

| [48] | Wood, D. J. (1991). Corporate social performance revisited. Academy of Management Review, 16(4), 691–718. |

[48]

examined the initiation of CSR disclosure and reported evidence consistent with a subsequent reduction in firms’ cost of equity capital, particularly when CSR performance is stronger. further linked CSR disclosure to analyst-related outcomes, documenting evidence that CSR disclosure is associated with improved analyst forecast accuracy (an information-quality channel that can lower capital costs and improve valuation). These studies support the view that social reporting can influence financial performance indirectly through lower cost of capital, higher analyst coverage/forecast quality, and improved investor confidence.

Within Kenya and the NSE context documented CSR disclosure practices among NSE-listed firms by examining annual reports and websites, and showed that CSR disclosure themes often cover community involvement, human resources, and environmental issues, with disclosure patterns related to firm size proxies (paid-up capital, revenue, profit before tax). While this work is more about determinants and patterns than performance impacts, it provides the baseline that social disclosure has been present (though uneven) among NSE firms, enabling later performance tests. More performance-oriented evidence is provided by who examined corporate sustainability practices and financial performance among firms listed on the NSE and reported empirical links consistent with sustainability practices being performance-relevant in the Kenyan market context. Finally, provide NSE evidence that broader ESG disclosures (which include social disclosure items) are positively related to stock liquidity and firm value, reinforcing social reporting’s likely importance through market-based performance channels even when accounting profitability effects may be ambiguous.

Based on the theoretical and empirical reviews, we formulate the following hypotheses:

2.2.3. Governance Reporting and Financial Performance

constructed a governance index based on shareholder rights and documented that stronger shareholder rights are associated with higher firm value and profitability; they also showed that a trading strategy based on governance strength generated abnormal returns during their sample period. Examined multiple governance measures (1998–2007) and assessed how governance relates to company performance, highlighting that governance performance relationships can be sensitive to the governance proxy chosen and to regulatory regime shifts (e.g., pre- vs post-SOX). These studies underpin the argument that governance reporting (and governance quality more broadly) matters for performance because it shapes managerial discipline, agency costs, and investor protection channels that directly affect profitability, valuation, and risk.

At the intersection of governance and broader responsibility frameworks,

| [36] | Ntim, C. G., & Soobaroyen, T. (2013). Corporate governance and performance in socially responsible corporations: New empirical insights from a developing economy. Corporate Governance: An International Review, 21(5), 468–494. |

[36]

investigated governance and performance in socially responsible corporations using a neo-institutional perspective, showing that governance mechanisms can interact with CSR/ESG-related practices and influence financial outcomes. At the evidence-synthesis level, conducted a meta-analysis of corporate governance mechanisms and firm financial performance and reported that governance mechanisms can have differential effects across developed and developing country settings implying that institutional context strongly shapes whether governance structures translate into better financial performance. This is particularly relevant for emerging markets (including Kenya), where enforcement intensity, ownership concentration, and disclosure quality can alter how governance reporting is interpreted by investors.

In the NSE/Kenya context, examined the effect of corporate governance on the financial performance of NSE-listed firms (2019–2023), using a census approach and reporting that corporate governance has measurable effects on listed firm financial performance. Similarly,

| [11] | Eccles, R. G., Ioannou, I., & Serafeim, G. (2014). The impact of corporate sustainability on organizational processes and performance. Management Science, 60(11), 2835–2857. |

[11]

analyzed corporate governance practices and financial performance for NSE-listed firms and reported statistically significant effects on ROA and ROE, with specific board attributes (composition, independence, committee structures) showing differentiated relationships with performance. From a regulatory and reporting environment perspective, the Capital Markets Authority (CMA) has institutionalized governance assessment reporting for issuers and reports continued improvements in governance application, explicitly linking good governance and sustainability practices to improved performance expectations in its corporate governance reporting ecosystem. These Kenyan studies collectively support the proposition that governance reporting especially when it reflects substantive governance practices rather than boilerplate compliance can be performance-relevant through reduced

| [3] | Capital Markets Authority. (2015). Code of corporate governance practices for issuers of securities to the public, 2015 (Code-8). |

[3]

agency conflicts, improved oversight, and stronger investor confidence.

Based on the theoretical and empirical reviews, we formulate the following hypotheses:

2.3. Mediation Role of Firm Size

Firm size is frequently theorized as a

transmission mechanism through which sustainability reporting (ESG disclosure) can influence financial outcomes because scale shapes both (i) the

capacity to undertake and report ESG activities and (ii) the

economic consequences of those activities. First, the determinants literature shows that size strongly predicts sustainability reporting intensity.

| [42] | Shleifer, A., & Vishny, R. W. (1997). A survey of corporate governance. The Journal of Finance, 52(2), 737–783. |

[42]

demonstrate that larger and more visible firms are substantially more likely to issue voluntary sustainability reports, consistent with legitimacy and stakeholder arguments that scale increases public scrutiny and political costs while also providing resources for measurement and reporting. Related evidence from emerging markets also finds that firm size predicts the extent of environmental disclosure among listed firms, reinforcing that scale supports disclosure systems and stakeholder engagement capacity

| [46] | United Nations Sustainable Stock Exchanges Initiative. (2025). ESG disclosure guidance database. |

[46]

.

Second, the measurement literature cautions that “size” can confound ESG constructs, making mediation modelling especially relevant.

| [10] | Drempetic, S., Klein, C., & Zwergel, B. (2020). The influence of firm size on the ESG score: Corporate sustainability ratings under review. Journal of Business Ethics, 167(2), 333–360. |

[10]

show that ESG scores and disclosure-based ratings tend to be biased upward for large firms because they generate more observable data and disclosures, not necessarily because they have proportionally superior sustainability performance. This implies that in ESG–performance models, firm size may not only be a control but may represent a channel through which disclosure becomes “visible” to markets and raters supporting structural (path) approaches that separate direct and indirect effects through size.

Third, several empirical studies explicitly operationalise

firm size as a mediator using causal-path logic. In Nigeria,

| [45] | Ullmann, A. A. (1985). Data in search of a theory: A critical examination of the relationships among social performance, social disclosure, and economic performance. Academy of Management Review, 10(3), 540–557. |

[45]

model firm size as an intervening variable between CSR cost and financial performance, with mediation tests indicating that CSR outlays partly transmit performance effects through size-related scaling (i.e., larger firms both spend more and convert CSR into outcomes differently). Similarly,

| [1] | Adamu, A., Ibrahim, A. A., & Ismail, A.-K. M. (2023). Mediating effect of firm size on the relationship between working capital management and profitability of listed industrial goods firms in Nigeria. FUOYE Journal of Management, Innovation and Entrepreneurship, 2(1). |

[1]

apply PLS-SEM and find that firm size mediates key working-capital–profitability linkages, illustrating how scaling of assets and operations can translate financial policies into profitability outcomes. In Kenya’s financial co-operative sector,

| [30] | Mirichii, D., Akims, M., & Nyachae, S. (2023). Mediating effect of firm size on the nexus between CAMEL rating model and financial performance of deposit-taking SACCOs in Kenya. Journal of Finance and Accounting, 7(1), 116–128. |

[30]

also document a mediating role for firm size in explaining how CAMEL-related fundamentals relate to performance, suggesting that size can convert organisational capabilities into superior outcomes. In SME settings across Eastern Europe and Central Asia, firm size is likewise modelled as a mediator/boundary mechanism in performance pathways, implying that scale conditions how resources translate into results

| [24] | Kijkasiwat, P., & Phuensane, P. (2020). Innovation and firm performance: The moderating and mediating roles of firm size and small and medium enterprise finance. Journal of Risk and Financial Management, 13(5), 97. |

[24]

. Collectively, these studies justify mediation analysis in ESG contexts: ESG disclosure may affect performance partly by enabling growth/scale (or by interacting with scale-dependent visibility and reporting capacity), while size can also bias observed ESG signals so modelling size as a mediator helps distinguish “disclosure-to-scale” and “scale-to-performance” pathways from any remaining direct ESG effects.

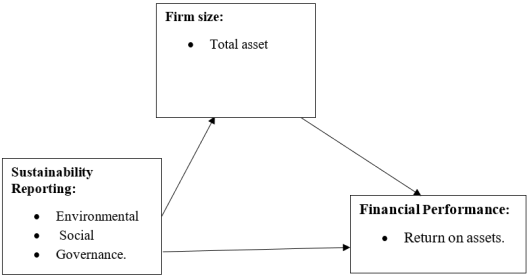

2.4. Conceptual Framework

Figure 1. Conceptual framework.

3. Material and Methods

3.1. Sample Size and Data

The target population comprised study subjects sharing similar characteristics from whom findings can be generalized

| [39] | Paolone, F., Celli, M., Nasta, L., & Sica, E. (2022). Does ESG disclosure influence firm performance? Evidence from Italy. Sustainability, 14(13), 7595. |

[39]

.

Accordingly, this study will target 67 firms listed on the Nairobi Securities Exchange (NSE) over 2012–2023. Firms were included only if they operated continuously throughout 2012–2023, had complete data, and did not undergo major restructurings such as mergers or acquisitions that could compromise data consistency. Firms with incomplete data or inconsistent operations were excluded and a final sample of 39 was used for analysis. The study used secondary data collected using a structured data collection schedule. Data collection involved gathering evidence to answer research questions or test hypotheses (Byers, 1995), and it was also described as a standardized process of gathering and analyzing accurate research data (Arun et al., 2022). Secondary data was considered more objective and reliable than primary data

| [43] | Shrivastava, P. (1995). The role of corporations in achieving ecological sustainability. Academy of Management Review, 20(4), 936–960. |

| [49] | Wooldridge, J. M. (2016). Introductory econometrics: A modern approach (6th ed.). Cengage Learning. |

[43, 49]

. Audited annual reports was sourced from firms’ websites, the Capital Markets Authority

| [4] | Capital Markets Authority. (2024). Quarterly statistical bulletin: Quarter ended December 2024. |

[4]

, and the African Financials database.

3.2. Measurement of Variables

The following section presents the measurement of the variables of the study which are financial performance as the dependent variable and environmental disclosure, social disclosure and governance disclosure as independent variables, firm size as the mediator variable and firm age and firm leverage as control variables.

Table 1 below show the measurement of each variable.

Table 1. Measurement of variables.

Variable | Measurement | Source |

ESG performance | Environmental, social and governance reporting index | GRI |

Financial performance | Return on assets | Umar et al., (2024), Pham et al., (2024) |

Firm age | Natural logarithm of number of years since incorporation | Firmansyah and Kartiko (2024). |

Firm size | Natural logarithm of total assets | Firmansyah and Kartiko (2024). |

Firm leverage | Firm leverage is commonly measured using the debt-to-equity ratio, which is calculated by dividing a firm's total debt by its shareholder equity | (Titman & Wessels, 1988; Frank & Goyal, 2009). |

Source: Authors

3.3. Regression Models

Drawing on previous panel-data literature on ESG disclosure and firm performance, this study employed a panel regression framework for the period 2012–2023 to examine the effect of ESG disclosure on financial performance and mediation effect of firm size on this relationship. Because the data consist of repeated observations for NSE-listed firms over time, the study was estimated using both fixed-effects models and panel structural model.

Model 1. Testing the effect of control variables on financial performance

Model 2. Testing the effect of ESG disclosure on financial performance

Model 3. Testing the effect of ESG on Firm asset

Model 4. Testing for mediation

4. Data Analysis and Interpretation

4.1. Descriptive Statistics

The descriptive statistics in

Table 2 indicate substantial dispersion in both financial outcomes and disclosure practices. Firm performance (n = 468) has a mean of 0.7962, suggesting slightly positive performance on average, but the standard deviation is large (4.9491) and the range is wide (−2.4566 to 42.3371). This implies strong heterogeneity, where some firms underperform while a few reports exceptionally high performance, potentially reflecting outliers or periods of unusually strong returns. Such variation is consistent with broader evidence that firm financial performance differs widely across firms and time because of differences in resources, strategy, and external conditions, and that ESG-related practices may associate with performance in context-specific ways. Firm age (n = 468) averages 38.55 years (SD = 18.41, min = 1, max = 74), indicating a largely mature sample but with meaningful lifecycle diversity. This matters because learning and selection dynamics imply that firms evolve unevenly: more efficient firms tend to survive and grow, while less efficient firms exit, producing performance differences across age cohorts. Leverage (n = 468) shows extreme dispersion (mean = 3.3905, SD = 26.0192, min = −11.7789, max = 568.1991), suggesting that firms employ very different financing structures, including potential net-cash positions (negative values) and very highly levered firms. Such heterogeneity aligns with capital structure theory, which emphasizes that leverage varies due to agency costs, asymmetric information, and firm-specific financing preferences. ESG disclosure levels are modest and uneven. The mean environmental disclosure score is 0.1073, social disclosure is 0.2227, and governance disclosure is highest at 0.3116, with minimum values of 0 across all pillars implying many non-disclosers alongside a smaller set of more transparent firms. This pattern is consistent with voluntary disclosure evidence showing wide cross-firm differences in CSR and environmental reporting incentives. The use of an ESG index anchored on the GRI Standards is also consistent with global practice in structuring comparable disclosures across environmental, social, and governance topics. Finally, firm size (mean = 7.1701, SD = 1.0389) indicates substantial scale differences; using log size is consistent with corporate finance guidance that different size proxies can affect inference and should be measured carefully.

Table 2. Descriptive statistics results.

Variable | Obs | Mean | Std. Dev. | Min | Max |

Firm performance | 468 | 0.796154 | 4.949137 | -2.456647 | 42.33706 |

Firm age | 468 | 38.55128 | 18.41328 | 1 | 74 |

Leverage | 468 | 3.390512 | 26.01921 | -11.77886 | 568.1991 |

Environmental disclosure | 468 | 0.1072917 | 0.194964 | 0 | 0.85 |

Social disclosure | 468 | 0.2227083 | 0.2365813 | 0 | 0.85 |

Governance disclosure | 468 | 0.3115741 | 0.2589709 | 0 | 0.9444444 |

Firm size | 468 | 7.170118 | 1.03889 | 4.425008 | 9.097318 |

Source: Authors computation

4.2. Correlation Results

The descriptive statistics in

Table 3 show wide variation in financial outcomes, capital structure, disclosure practices, and scale. Firm performance (n = 468) has a mean of 0.7962, indicating slightly positive average performance, but the standard deviation (4.9491) and broad range (−2.4566 to 42.3371) suggest substantial heterogeneity, including a few exceptionally high-performing observations that may reflect outliers or unusual firm-year conditions. Such dispersion is consistent with evidence that performance outcomes differ markedly across firms and time, and that ESG-related behavior can be associated with mixed financial effects depending on context and measurement

| [13] | Friede, G., Busch, T., & Bassen, A. (2015). ESG and financial performance: Aggregated evidence from more than 2,000 empirical studies. Journal of Sustainable Finance & Investment, 5(4), 210–233. |

[13]

. Firm age (n = 468) averages 38.55 years (SD = 18.41, min = 1, max = 74), implying a predominantly mature sample while still capturing firms at different lifecycle stages. This spread matters because learning and selection dynamics imply that firms evolve unevenly: efficient firms are more likely to survive and expand, while weaker firms exit, creating persistent differences in outcomes across cohorts

| [22] | Jovanovic, B. (1982). Selection and the evolution of industry. Econometrica, 50(3), 649–670. |

[22]

. Leverage (n = 468) shows extreme dispersion (mean = 3.3905, SD = 26.0192, max = 568.1991), indicating very different financing structures across firms; capital structure theory similarly emphasizes that leverage can vary widely due to asymmetric information, agency considerations, and firm-specific financing choices

| [18] | Harris, M., & Raviv, A. (1991). The theory of capital structure. The Journal of Finance, 46(1), 297–355. |

| [31] | Myers, S. C. (1984). The capital structure puzzle. The Journal of Finance, 39(3), 574–592. |

[18, 31]

. ESG disclosure scores are generally modest and uneven: environmental disclosure averages 0.1073, social disclosure 0.2227, and governance disclosure 0.3116, with minimum values of 0 across pillars, indicating many non-disclosers and a smaller group of more transparent firms. Such uneven voluntary disclosure patterns align with prior evidence on environmental and CSR reporting incentives and variability in disclosure quality

| [6] | Clarkson, P. M., Li, Y., Richardson, G. D., & Vasvari, F. P. (2008). Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Accounting, Organizations and Society, 33(4–5), 303–327. |

| [8] | Dhaliwal, D. S., Li, O. Z., Tsang, A., & Yang, Y. G. (2011). Voluntary nonfinancial disclosure and the cost of equity capital: The initiation of corporate social responsibility reporting. The Accounting Review, 86(1), 59–100. |

[6, 8]

, and they fit the broader finding that ESG–performance relationships are not uniform across settings

| [13] | Friede, G., Busch, T., & Bassen, A. (2015). ESG and financial performance: Aggregated evidence from more than 2,000 empirical studies. Journal of Sustainable Finance & Investment, 5(4), 210–233. |

[13]

. Finally, firm size (mean = 7.1701, SD = 1.0389) indicates notable scale differences; using log size is consistent with corporate finance guidance that size measurement choices matter for inference

| [7] | Dang, C., Li, Z. (Frank), & Yang, C. (2018). Measuring firm size in empirical corporate finance. Journal of Banking & Finance, 86, 159–176. |

[7]

.

Table 3. Correlation test results.

Variable | FP | FA | FL | ED | SD | GD | FS |

Firm performance | 1.0000 | | | | | | |

Firm age | -0.0533 | 1.0000 | | | | | |

Leverage | 0.0145 | 0.0264 | 1.0000 | | | | |

Environmental disclosure | -0.0493 | 0.0326 | -0.0410 | 1.0000 | | | |

Social disclosure | -0.0323 | -0.0207 | -0.0484 | 0.8172* | 1.0000 | | |

Governance disclosure | 0.0393 | -0.0415 | -0.0551 | 0.7446* | 0.8452* | 1.0000 | 0.0941* |

Firm size | -0.2489* | -0.0579 | 0.0622 | 0.0751 | 0.2153* | 0.0941* | 1.0000 |

Source: Authors computation

4.3. Regression Results

4.3.1. Control Effect Results

The regression results for firm performance and the control variables are presented in table 4. Based on the results of the Hausman Test, the fixed effect model is used for interpretations. The fixed-effects (within) regression explores how firm age and leverage influence firm performance (ROA) for 39 listed firms over 12 years (468 firm-year observations). The within R² of 0.9268 indicates that about 92.7% of the variation in ROA over time within firms is explained by firm age and leverage, after controlling for unobserved time-invariant firm characteristics. The overall F-statistic (F(2, 427) = 2704.52, p < 0.001) confirms that the explanatory variables are jointly highly significant. The strong correlation between the unobserved firm effects and the regressors (corr(uᵢ, Xb) = −0.8922) supports the use of fixed-effects rather than pooled OLS or random-effects, consistent with panel-data guidance that FE is appropriate when regressors are correlated with unobserved heterogeneity

| [49] | Wooldridge, J. M. (2016). Introductory econometrics: A modern approach (6th ed.). Cengage Learning. |

[49]

.

Firm age has a positive and highly significant coefficient (β = 0.3704, t = 41.16, p < 0.001), implying that, holding leverage and time-invariant firm traits constant, older firms exhibit higher ROA. This aligns with recent evidence that more mature firms exploit accumulated experience, routines and reputational capital to convert growth into sustainable profitability

| [28] | Mansikkamäki, S. (2023). Firm growth and profitability: The role of age and size in shifts between growth–profitability configurations. Journal of Business Venturing Insights, 19, e00372. https://doi.org/10.1016/j.jbvi.2023.e00372 |

[28]

. Older firms are also more likely to have refined internal processes, established stakeholder relationships and learning effects that reduce operating costs and performance volatility, enhancing financial outcomes.

By contrast, leverage has a negative and statistically significant coefficient (β = −0.3081, t = −8.01, p < 0.001), indicating that increases in debt ratios are associated with lower ROA within firms. This is consistent with studies showing that excessive leverage can erode firm performance through higher interest burdens, increased probability of financial distress and reduced strategic flexibility

| [17] | Guo, H., Legesse, T. S., Tang, J., & Wu, Z. (2021). Financial leverage and firm efficiency: The mediating role of cash holding. Applied Economics, 53(18), 2108–2124.

https://doi.org/10.1080/00036846.2020.1855317 |

| [25] | Kijkasiwat, P., Hussain, A., & Mumtaz, A. (2022). Corporate governance, firm performance and financial leverage across developed and emerging economies. Risks, 10(10), 185.

https://doi.org/10.3390/risks10100185 |

[17, 25]

. Recent Kenyan evidence similarly reports that capital structure choices matter: over-reliance on debt financing is associated with weaker profitability among commercial state corporations

| [37] | Nyongesa, E. M., & Jagongo, A. O. (2024). Capital structure and profitability of commercial state corporations in Kenya. Academic Journal of Social Sciences and Education, 12(4), 14–29. |

[37]

.

The estimated rho (ρ = 0.33) suggests that roughly one-third of the total variance in ROA is due to persistent firm-specific factors, such as management quality, corporate culture or business model. The insignificant F-test for all uᵢ = 0 (p = 0.2173) does not invalidate the FE choice; rather, model selection in practice relies on both statistical tests and economic reasoning about correlation between regressors and unobserved heterogeneity

| [49] | Wooldridge, J. M. (2016). Introductory econometrics: A modern approach (6th ed.). Cengage Learning. |

[49]

. Overall, the results indicate that, for listed firms, age is a strong positive driver of performance, whereas high leverage systematically depresses ROA, reinforcing the importance of life-cycle and capital-structure decisions for firm profitability.

Table 4. Testing the Effect of the Control Variables of Firm Performance.

Fixed-effects (within) regression | Number of obs | = | 468 |

Group variable: COMPANYID | Number of groups | = | 39 |

R-sq: within = 0.9268 | Obs per group: min | = | 12 |

between = 0.9995 | Avg | = | 12.0 |

overall = 0.9929 | Max | = | 12 |

| F(2,427) | = | 2704.52 |

corr(u_i, Xb) = -0.8922 | Prob > F | = | 0.0000 |

Firm performance | Coef. | Std. Err. | t | P>t | [95% Conf. | Interval] |

Firm age | .370405 | .0332964 | 41.16 | 0.000 | .304959 | .43585 |

Firm leverage | -.3080578 | .038474 | -8.01 | 0.000 | -.3836799 | -.2324358 |

_cons | .0061747 | .0039326 | 1.57 | 0.117 | -.001555 | .0139043 |

sigma_u | .05995106 | | | | | |

sigma_e | .08499718 | | | | | |

Rho | .33221609 | (fraction of variance due to u_i) |

F test that all u_i=0: F(38, 427) = 1.18 Prob > F = 0.2173 |

Source: Researcher (2025)

4.3.2. Mediation Test Results

The results in

Table 5 report a mediation path model in which environmental, social, and governance disclosure (ESG pillars) affect firm performance both directly and indirectly through firm size. This approach is important because the ESG–performance relationship is frequently found to be empirically mixed across studies due to differences in measurement, performance proxies, and model design, implying that intermediate “transmission channels” can meaningfully alter the sign and significance of findings

| [23] | Khan, M. A. (2022). ESG disclosure and firm performance: A bibliometric and meta-analysis. Research in International Business and Finance, 61, 101668. |

[23]

. In this model, three sets of relationships are estimated: (i) ESG pillars → firm size (the “a-paths”), (ii) firm size → firm performance (the “b-path”), and (iii) ESG pillars → firm performance (direct “c′-paths”), with indirect and total effects reported to show how firm size mediates the ESG–performance link.

Starting with the ESG → firm size paths, the results indicate that the disclosure pillars are associated with firm size in different directions. Environmental disclosure has a negative and statistically significant direct effect on firm size (β = −0.2617, z = −3.42, p = .001; 95% CI [−0.4117, −0.1118]). This means that higher environmental disclosure scores are associated with smaller firm size, holding the other ESG pillars constant. This sign is noteworthy because a large body of ESG measurement research shows that ESG scores and disclosure availability are often positively related to firm size, partly because larger firms possess more resources for data production and face greater stakeholder scrutiny.

| [10] | Drempetic, S., Klein, C., & Zwergel, B. (2020). The influence of firm size on the ESG score: Corporate sustainability ratings under review. Journal of Business Ethics, 167(2), 333–360. |

[10]

explicitly show that corporate sustainability ratings can be influenced by firm size through data availability and disclosure capacity, implying a potential size-related bias in ESG assessments. More recent evidence confirms that this “size bias” persists in widely used ESG datasets, including Refinitiv ESG, despite attempts to reduce it

| [9] | Dobrick, J., Klein, C., & Zwergel, B. (2023). Size bias in Refinitiv ESG data. Finance Research Letters, 58, 104014. |

[9]

. Against that background, your negative environmental disclosure–size relationship may suggest that, in the context of your sample and disclosure index, environmental transparency is not simply a “large-firm reporting luxury.” Instead, environmental disclosure may be used strategically by smaller firms as a legitimacy signal, or it may reflect industry composition where smaller firms disclose more environmental information relative to their scale. It may also reflect how your environmental disclosure indicator is constructed (e.g., content-scored intensity), which can produce patterns different from commercial ESG rating databases where large-firm coverage is structurally higher

| [9] | Dobrick, J., Klein, C., & Zwergel, B. (2023). Size bias in Refinitiv ESG data. Finance Research Letters, 58, 104014. |

| [10] | Drempetic, S., Klein, C., & Zwergel, B. (2020). The influence of firm size on the ESG score: Corporate sustainability ratings under review. Journal of Business Ethics, 167(2), 333–360. |

[9, 10]

.

In contrast, social disclosure has a strong positive and statistically significant direct effect on firm size (β = 0.6472, z = 6.77, p < .001; 95% CI [0.4599, 0.8345]). This suggests that larger firms tend to have higher social disclosure. Substantively, this is consistent with the practical reality that social reporting (employee welfare, human capital programs, community engagement, customer responsibility, supply chain standards) typically expands with organizational scope. It is also consistent with governance scholarship showing that board characteristics and oversight configurations can be associated with higher ESG disclosure levels features that are more prevalent in larger, more visible firms

| [34] | Nguyen, P. T. M., & Nguyen, L. T. M. (2023). The board profiles that promote environmental, social, and governance disclosure—Evidence from S&P 500 firms. Finance Research Letters, 57, 103925. |

| [44] | Suttipun, M. (2021). The influence of board composition on environmental, social and governance (ESG) disclosure of Thai listed companies. International Journal of Disclosure and Governance, 18(4), 391–402. |

[34, 44]

. Thus, the social pillar appears to follow the more “typical” disclosure pattern: as firms become larger, their social reporting tends to increase.

The governance pillar shows a different pattern: governance disclosure has a negative and statistically significant direct effect on firm size (β = −0.2580, z = −3.13, p = .002; 95% CI [−0.4197, −0.0963]). This indicates that higher governance disclosure is associated with smaller firm size in this model. One plausible interpretation is compensatory signaling: smaller firms may disclose more governance detail to reassure stakeholders where market visibility, analyst coverage, or reputational capital are limited. Another possibility is structural: if some smaller firms are in sectors with stronger governance compliance requirements or more concentrated ownership structures, governance disclosure intensity could be higher even without large scale. In addition, ESG disclosure is not purely a size-driven reporting outcome; board “profiles” and governance arrangements can produce high ESG reporting even within the same broad size category

| [34] | Nguyen, P. T. M., & Nguyen, L. T. M. (2023). The board profiles that promote environmental, social, and governance disclosure—Evidence from S&P 500 firms. Finance Research Letters, 57, 103925. |

| [44] | Suttipun, M. (2021). The influence of board composition on environmental, social and governance (ESG) disclosure of Thai listed companies. International Journal of Disclosure and Governance, 18(4), 391–402. |

[34, 44]

. The negative sign therefore suggests that governance disclosure may function differently from social disclosure in this sample less as a byproduct of organizational scale, and more as a targeted credibility mechanism.

The firm size → firm performance relationship is central because it determines the sign and strength of all mediated effects. Firm size has a negative and highly significant direct effect on firm performance (β = −0.2550, z = −5.54, p < .001; 95% CI [−0.3453, −0.1648]). This implies that larger size is associated with lower performance in the model. Importantly, the corporate finance literature warns that size effects can be sensitive to how size is measured (assets vs sales vs market value) and how models are specified, so interpretation should be tied to your operational definition of size

| [7] | Dang, C., Li, Z. (Frank), & Yang, C. (2018). Measuring firm size in empirical corporate finance. Journal of Banking & Finance, 86, 159–176. |

[7]

. Substantively, the negative size–performance link aligns with evidence that profitability can decline with size when the costs of complexity, bureaucracy, and coordination outweigh scale efficiencies. Large multi-country panel evidence similarly documents cases where firm size is negatively associated with profitability even when firm growth is beneficial, underscoring that “being large” and “growing efficiently” are not identical phenomena

| [50] | Yadav, I. S., Pahi, D., & Gangakhedkar, R. (2022). The nexus between firm size, growth and profitability: New panel data evidence from Asia–Pacific markets. European Journal of Management and Business Economics, 31(1), 115–140. |

[50]

.This negative b-path is crucial for your mediation logic: any ESG pillar that increases size will mechanically transmit a negative indirect effect to performance, while any ESG pillar associated with smaller size will transmit a positive indirect effect.

Turning to the direct ESG → firm performance paths (holding firm size in the model), the results again vary sharply across pillars. Environmental disclosure has a negative and statistically significant direct effect on firm performance (β = −0.1770, z = −2.27, p = .023; 95% CI [−0.3301, −0.0239]). A plausible explanation is that environmental disclosure (and the underlying environmental management systems it reflects) can impose short-run costs monitoring, compliance, verification, reporting systems, and operational adjustments that depress contemporaneous profitability. This is consistent with international evidence showing that disclosure of carbon and environmental information can be linked to financial performance in complex ways, with benefits depending on institutional setting and on whether improvements are operational or primarily reputational

| [51] | Zhang, Y., Wang, X., & Li, Z. (2025). Environment, social, and governance disclosures and firm performance: A meta-analysis. Journal of Applied Accounting Research. |

[51]

. It also fits the broader ESG literature where environmental effects are sometimes negative in the short run but may differ over longer horizons or under different market pricing of ESG information

| [23] | Khan, M. A. (2022). ESG disclosure and firm performance: A bibliometric and meta-analysis. Research in International Business and Finance, 61, 101668. |

[23]

.

Social disclosure has a near-zero direct effect on firm performance and is not statistically significant (β = 0.0082, z = 0.08, p = .935; 95% CI [−0.1896, 0.2059]). This suggests that, after accounting for firm size and the other ESG pillars, there is no detectable direct association between social disclosure and performance in this sample. This “null” result is not unusual in ESG research: many studies find that social disclosure effects can be contingent on context, stakeholder salience, and measurement approaches, and that significance may disappear once endogeneity and firm characteristics are controlled

| [23] | Khan, M. A. (2022). ESG disclosure and firm performance: A bibliometric and meta-analysis. Research in International Business and Finance, 61, 101668. |

[23]

. In other words, social disclosure may matter through channels other than immediate profitability (e.g., risk reduction, employee retention, or reputational resilience), or it may require longer horizons to manifest in accounting performance.

Governance disclosure has a positive and statistically significant direct effect on firm performance (β = 0.1882, z = 2.24, p = .025; 95% CI [0.0234, 0.3530]). This implies that improved governance transparency is associated with better performance, consistent with the idea that governance disclosure is tied to stronger monitoring, accountability, and decision discipline. Pillar-level studies frequently find governance to be the most performance-relevant ESG dimension because governance directly affects agency costs and resource allocation efficiency. For instance, empirical work in European settings reports that ESG disclosure can be associated with improved performance, with governance often exerting a comparatively robust relationship when considered by pillar

| [40] | Porter, M. E., & Kramer, M. R. (2011). Creating shared value. Harvard Business Review, 89(1–2), 62–77. |

[40]

. Evidence from other markets similarly finds positive profitability links with ESG dimensions (including governance), although magnitudes vary

| [2] | Aydogmus, M., Gulay, G., & Ergun, K. (2022). Impact of ESG performance on firm value and profitability. Borsa Istanbul Review, 22(Suppl. 2), S119–S127. |

[2]

.

The mediation analysis becomes clearer when interpreting the indirect effects (ESG → firm size → firm performance). Environmental disclosure has a positive and significant indirect effect on firm performance (β = 0.0667, z = 2.91, p = .004; 95% CI [0.0218, 0.1117]). This occurs because environmental disclosure reduces firm size (negative a-path), while larger size reduces performance (negative b-path); multiplying two negatives yields a positive mediated effect. Substantively, this indicates that environmental disclosure is associated with improved performance through its relationship with smaller size. One interpretation is that environmentally transparent firms in your sample may remain leaner or operate at a scale where efficiency is higher, and because size is negatively related to performance, this “leaner scale” pathway produces a positive performance implication. Importantly, this is a mediation story not proof that becoming smaller causes better performance but it does show that firm size is an economically meaningful channel that can offset some direct environmental costs.

For social disclosure, the indirect effect is negative and highly significant (β = −0.1651, z = −4.29, p < .001; 95% CI [−0.2405, −0.0896]). Here the logic is consistent with the signs: social disclosure increases firm size (positive a-path), and size reduces performance (negative b-path), creating a negative indirect effect. This suggests that social disclosure may be associated with lower performance mainly through its linkage with scale expansion and complexity. The result fits broader discussions in the size–performance literature that larger scale can depress profitability when coordination costs dominate

| [52] | Sekaran, U., & Bougie, R. (2019). Research methods for business: A skill-building approach (8th ed.). Wiley. |

[52]

, and it also resonates with the idea that size and resources shape how firms implement and report ESG sometimes producing disclosure patterns that are more about organizational scope than immediate value creation

| [9] | Dobrick, J., Klein, C., & Zwergel, B. (2023). Size bias in Refinitiv ESG data. Finance Research Letters, 58, 104014. |

| [10] | Drempetic, S., Klein, C., & Zwergel, B. (2020). The influence of firm size on the ESG score: Corporate sustainability ratings under review. Journal of Business Ethics, 167(2), 333–360. |

[9, 10]

. The key point is that social disclosure appears not to have a direct performance association, but it still matters indirectly because it is strongly related to firm size, and firm size is negatively related to performance.

For governance disclosure, the indirect effect is positive and significant (β = 0.0658, z = 2.72, p = .006; 95% CI [0.0184, 0.1132]). This is again due to governance disclosure reducing size (negative a-path) while size reduces performance (negative b-path), yielding a positive product. In practical terms, governance disclosure improves performance partly via the size channel (through association with smaller scale) and partly through its own positive direct effect. This “two-path reinforcement” is why governance disclosure stands out in the total effects.

Finally, the total effects summarize the net relationship between each ESG pillar and firm performance after adding direct and indirect components. Environmental disclosure’s total effect is negative but not statistically significant (β = −0.1102, p = .166; 95% CI [−0.2663, 0.0458]). This indicates that the negative direct association (−0.1770) is partly offset by a positive mediated effect (+0.0667), yielding a net effect that is not reliably different from zero. Such offsetting patterns are consistent with ESG research showing that environmental reporting may involve short-run costs but potential indirect benefits depending on firm structure and context

| [23] | Khan, M. A. (2022). ESG disclosure and firm performance: A bibliometric and meta-analysis. Research in International Business and Finance, 61, 101668. |

| [51] | Zhang, Y., Wang, X., & Li, Z. (2025). Environment, social, and governance disclosures and firm performance: A meta-analysis. Journal of Applied Accounting Research. |

[23, 51]

Social disclosure’s total effect is also negative but not significant (β = −0.1569, p = .115; 95% CI [−0.3517, 0.0380]). This result is driven almost entirely by the negative indirect pathway via size, since the direct effect is essentially zero. Governance disclosure’s total effect is positive and statistically significant (β = 0.2540, p = .003; 95% CI [0.0857, 0.4222]). This indicates that governance disclosure is the only pillar with a clear, net-positive association with firm performance in this model consistent with the argument that governance transparency is central to value creation and operational discipline, and consistent with empirical work showing that ESG disclosure can relate positively to performance, often with governance as a comparatively robust component

| [2] | Aydogmus, M., Gulay, G., & Ergun, K. (2022). Impact of ESG performance on firm value and profitability. Borsa Istanbul Review, 22(Suppl. 2), S119–S127. |

| [51] | Zhang, Y., Wang, X., & Li, Z. (2025). Environment, social, and governance disclosures and firm performance: A meta-analysis. Journal of Applied Accounting Research. |

[2, 51]

.

Overall, the results imply three high-level conclusions. First, ESG pillars should not be treated as interchangeable: they influence firm size differently and performance differently, producing distinct direct and mediated pathways. Second, firm size is a powerful channel in your model because it is strongly and negatively associated with performance; this makes mediation effects economically meaningful and explains why social disclosure though directly insignificant still has a significant indirect effect. Third, the findings reinforce a broader methodological message: because ESG disclosure and size are often entangled (and ESG datasets can exhibit size-related biases), researchers should interpret size-related mediation carefully and ensure robustness to alternative measurement choices

| [7] | Dang, C., Li, Z. (Frank), & Yang, C. (2018). Measuring firm size in empirical corporate finance. Journal of Banking & Finance, 86, 159–176. |

| [9] | Dobrick, J., Klein, C., & Zwergel, B. (2023). Size bias in Refinitiv ESG data. Finance Research Letters, 58, 104014. |

| [10] | Drempetic, S., Klein, C., & Zwergel, B. (2020). The influence of firm size on the ESG score: Corporate sustainability ratings under review. Journal of Business Ethics, 167(2), 333–360. |

[7, 9, 10]

.

Table 5. Mediation test results.

Predictor | Outcome | Effect type | Coef. | Std. Err. | z | p-value | 95% CI (Lower) | 95% CI (Upper) |

Environmental disclosure | Firm size | Direct | -0.2617 | 0.0765 | -3.42 | 0.001 | -0.4117 | -0.1118 |

Social disclosure | Firm size | Direct | 0.6472 | 0.0955 | 6.77 | 0.000 | 0.4599 | 0.8345 |

Governance disclosure | Firm size | Direct | -0.2580 | 0.0825 | -3.13 | 0.002 | -0.4197 | -0.0963 |

Firm size | Firm performance | Direct | -0.2550 | 0.0460 | -5.54 | 0.000 | -0.3453 | -0.1648 |

Environmental disclosure | Firm performance | Direct | -0.1770 | 0.0781 | -2.27 | 0.023 | -0.3301 | -0.0239 |

Social disclosure | Firm performance | Direct | 0.0082 | 0.1009 | 0.08 | 0.935 | -0.1896 | 0.2059 |

Governance disclosure | Firm performance | Direct | 0.1882 | 0.0841 | 2.24 | 0.025 | 0.0234 | 0.3530 |

Environmental disclosure | Firm performance | Indirect | 0.0667 | 0.0229 | 2.91 | 0.004 | 0.0218 | 0.1117 |

Social disclosure | Firm performance | Indirect | -0.1651 | 0.0385 | -4.29 | 0.000 | -0.2405 | -0.0896 |

Governance disclosure | Firm performance | Indirect | 0.0658 | 0.0242 | 2.72 | 0.006 | 0.0184 | 0.1132 |

Environmental disclosure | Firm performance | Total | -0.1102 | 0.0796 | -1.38 | 0.166 | -0.2663 | 0.0458 |

Social disclosure | Firm performance | Total | -0.1569 | 0.0994 | -1.58 | 0.115 | -0.3517 | 0.0380 |

Governance disclosure | Firm performance | Total | 0.2540 | 0.0858 | 2.96 | 0.003 | 0.0857 | 0.4222 |

Source: Authors computation

5. Conclusion and Recommendations

This study analyzed a mediation-based model that distinguishes direct, indirect, and total effects on how environmental disclosure (ED), social disclosure (SD), and governance disclosure (GD) influence firm performance, and whether firm size acts as an important transmission mechanism linking ESG disclosure to performance. The results demonstrate that ESG pillars affect firm outcomes through different pathways. First, the model shows that ESG dimensions are significantly associated with firm size in different directions. Environmental disclosure has a negative and significant relationship with firm size, implying that higher environmental disclosure is more prevalent among smaller firms or is associated with a reduction in firm size. Governance disclosure also has a negative and significant relationship with firm size. In contrast, social disclosure has a positive and significant relationship with firm size, suggesting that firms that are larger tend to report more on social issues or that increasing social disclosure is associated with greater firm scale. These contrasting patterns indicate that ESG disclosure does not evolve uniformly with scale; rather, different ESG pillars are linked to firm size in distinct ways, likely reflecting differences in reporting incentives, stakeholder pressures, and the operational scope required to implement and disclose each dimension.

Second, firm size has a negative and highly significant direct effect on firm performance. This implies that, within the model, increases in size are associated with a decline in performance, potentially reflecting rising coordination costs, bureaucratic complexity, or efficiency losses as firms expand. This negative size–performance relationship is critical because it determines the direction of mediation effects: ESG pillars that increase firm size transmit a negative indirect impact on performance, while ESG pillars associated with smaller firm size transmit a positive indirect effect.

Third, the direct effects of ESG disclosure on firm performance vary by pillar. Environmental disclosure has a negative and significant direct effect on performance, consistent with the interpretation that environmental reporting and related compliance or implementation requirements can impose short-run costs that weaken contemporaneous profitability. Social disclosure has an insignificant direct effect, suggesting that social transparency does not independently explain performance differences once firm size and other ESG pillars are considered. Governance disclosure has a positive and significant direct effect, implying that stronger governance transparency is associated with improved performance, likely due to better oversight, accountability, and reduced agency problems.

The mediation results show that firm size meaningfully reshapes the ESG–performance relationship. Environmental disclosure has a positive and significant indirect effect on performance through firm size, meaning that environmental disclosure contributes to better performance via its association with smaller firm size (and since smaller size is associated with higher performance in the model). However, when the negative direct effect and the positive indirect effect are combined, the total effect of environmental disclosure becomes statistically insignificant, indicating an offsetting relationship where environmental disclosure’s costs and size-mediated benefits largely cancel out. Social disclosure has a negative and significant indirect effect through firm size: because social disclosure increases size and size reduces performance, SD reduces performance indirectly even though its direct effect is insignificant. Nonetheless, the total effect of social disclosure remains statistically insignificant, implying that its adverse size channel is not strong enough to yield a net effect different from zero in the total relationship. Governance disclosure has a positive and significant indirect effect through firm size and also a positive direct effect, producing a positive and statistically significant total effect. Overall, governance disclosure emerges as the only ESG pillar with a clear net performance-enhancing relationship.

These findings contribute to ESG and corporate performance literature by demonstrating that ESG disclosure effects are not only pillar-specific but also channel-specific, with firm size functioning as a key mechanism that can either amplify or offset direct ESG effects. In this context, governance disclosure appears most closely aligned with value creation, while environmental disclosure reflects a trade-off between short-run costs and compensating indirect effects, and social disclosure primarily operates through scale-related complexity rather than direct profitability gains.

Several recommendations follow from these results. First, firms should strengthen governance practices and governance reporting quality, given the consistently positive direct and total performance effects. Boards should prioritize transparency in oversight, internal controls, audit quality, ethics systems, and accountability structures, ensuring governance disclosure reflects real operational discipline rather than symbolic reporting. Second, managers should approach environmental disclosure and environmental initiatives as long-term investments and manage their short-run cost burdens carefully. Firms can reduce the likelihood of performance decline by integrating environmental initiatives into core operational efficiency programs, linking environmental targets to measurable cost savings, risk reduction, and process improvements. Third, because social disclosure is linked to larger firm size and larger size is linked to lower performance firms should ensure that expansion in social programs and reporting is paired with strong cost control and productivity management. Social initiatives should be designed to deliver operational benefits (retention, productivity, reputational resilience) rather than adding unproductive complexity. For investors and stakeholders, the results imply that ESG disclosures should be interpreted with attention to which pillar is disclosed and through what mechanism it may affect performance. Governance disclosure is more likely to signal stronger performance, while environmental disclosure may indicate transitional costs and should be evaluated alongside operational efficiency indicators and longer-horizon outcomes. Finally, regulators and standard setters should encourage ESG reporting that emphasizes measurable outcomes and comparability, particularly for environmental and social disclosures, to reduce ambiguity and improve decision-usefulness. Future research should test whether the environmental and social effects change with time lags, whether industry differences alter the size-mediated pathway, and whether governance quality moderates the indirect channels linking ESG disclosure, firm size, and firm performance.