1. Introduction

These rules of fiscal control of Member States with the Euro as a single currency constitute a unique mechanism on a world scale. Since their inception they enjoy a great meaning for both Member States and the EU as their community. Yet, despite the relevance of this sophisticated legal regime, research has not sufficiently contributed to discuss this new legal framework, suggest its strengthening or a simple change of the existing mechanism. The current study aims to close this gap.

The legislative package of ‘Six-Pack’

| [1] | Regulation 1175/2011 amending Regulation 1466/97: On the strengthening of the surveillance of budgetary positions and the surveillance and coordination of economic policies, OJ L 306/54, 23 November 2011. |

[1]

brought a concrete step towards ensuring fiscal discipline, helping to stabilize the EU economy and preventing a new crisis in the EU, in response to the European debt crisis of 2009. The ‘Six-Pack' was a part of the reform of the Stability and Growth Pact in 2011, which drew the lessons of the economic and financial crisis. The Stability and Growth Pact contained the so-called preventive arm that aimed to guide Member States towards a country-specific, medium-term budgetary objective (MTO) which sets out to ensure public finance sustainability.

Due to the fact, that the greater macroeconomic surveillance introduced 2011 with Six-Pack

might have turned insufficient, EU introduced 2013 a new legislation

the so-called “Two-Pack”

| [4] | Regulation (EU) No 473/2013 of the European Parliament and of the Council of 21 May 2013 on common provisions for monitoring and assessing draft budgetary plans and ensuring the correction of excessive deficit of the Member States in the euro area, OJ L 140, 27.5.2013, p. 11–23. |

[4]

. However, this legal framework turned out to be inadequate as well. Due to the insufficient political will to adhere to hard budget constraints, stakeholders looked for further mechanism. Subsequently, also other measures, like the Public Sector Purchase Programme (PSPP), in 2015 – 2018 and 2019, were introduced. The current research addresses questions of the influence of EU institutions on national budget plans. It deals with the topic of the control of national draft laws and budgetary plans and answers the question of possible strengthening of the existing legal framework increasing legal certainty in the euro area.

Notably, that experience highlighted the need for specific provisions in the EU's fiscal rules to allow for a coordinated and orderly temporary deviation from the normal requirements for all Member States in a situation of generalized crisis caused by a severe economic downturn of the euro area or the EU as a whole.

Since 2013 – the “Two-Pack” – each euro area Member State must notify its budget plan to the European Commission before it adopts its budget law. The added value of this exercise is the direct guidance that it introduces within the budgetary procedure, thereby equipping all stakeholders with the information they need.

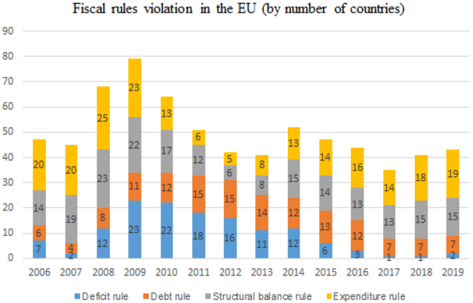

The graph below presents non-observance of fiscal rules in the European Union. It shows that there is a strong need for new legislation regarding budgetary control of Member States’ budgets.

Figure 1. Fiscal rules violations in the EU.

European institutions addressed non-compliance with EU fiscal rules by several legislation reforms. Six-Pack

| [5] | Regulation (EU) No 1173/2011 of the European Parliament and of the Council of 16 November 2011 on the effective enforcement of budgetary surveillance in the euro area, OJ L 306, 23.11.2011, p. 1–7. |

[5]

and Two-Pack

| [4] | Regulation (EU) No 473/2013 of the European Parliament and of the Council of 21 May 2013 on common provisions for monitoring and assessing draft budgetary plans and ensuring the correction of excessive deficit of the Member States in the euro area, OJ L 140, 27.5.2013, p. 11–23. |

[4]

succeeded to increase compliance of some fiscal rules. These legislative packages did succeed to reduce the number of countries that violate the deficit and debt rules, as can be seen in the graph.

However, measures introduced did not succeed to reduce the number of non-observance of fiscal violations of countries regarding the structural balance rule and the expenditure rule. The number of countries that do not observe these types of rules has increased rather than decreased over the years. Moreover – depending of the rule – the number of countries not complying with it differs. There are at least few countries not following a rule each year. In some years however the vast majority of the EU countries did not follow some of the rules. This research proposal originates to increase the compliance with those fiscal rules.

The structural balance rule assumes that additional income from natural resources is going to remain indefinitely, and therefore all the accumulated funds are saved with the idea of exhausting them in case of a severe recession. At the same time, there are many different expenditure rules in the Member States of the EU. Depending on their design, they may promote divergent goals.

This shows that the review of Member States’ budget plans exercised by the European Commission needs a new design that would address these discrepancies. Under the new financial recovery plan

| [6] | Communication from the Commission to the European Parliament, the European Council, the Council, the European Economic and Social Committee and the Committee of the Regions, Europe's moment: Repair and Prepare for the Next Generation, COM(2020) 456 final. |

[6]

, it could be beneficial to introduce a far-reaching control of the EU towards national budgetary laws. Maybe, “the added value of the exercise” of the preventive control is not appropriate and some stronger mechanism would be advantageous. It is rather unlikely, that the respected wording of recital 21 (“budget plan”) and 22 (“budget law”) differ.

Extending the legal mechanism in question can be done for example by extending the rights of the European Commission during national legislative process on a budget draft. Possibly a right of the Commission to issue an opinion to the budget plan connected to a stand-still clause respecting the draft budget law itself would be better to stabilize the markets sustainably.

2. Legal Environment

According to article 7 of the Regulation 473/2013

| [4] | Regulation (EU) No 473/2013 of the European Parliament and of the Council of 21 May 2013 on common provisions for monitoring and assessing draft budgetary plans and ensuring the correction of excessive deficit of the Member States in the euro area, OJ L 140, 27.5.2013, p. 11–23. |

[4]

the European Commission shall adopt its opinion on the Member State’s draft budgetary plan. The interpretation of this article with recitals allows a first conclusion, that article 7 refers indirectly to a budget law of Member States, although the wording itself covers solely a budget plan. In this respect, recital 21 of this regulation clarifies that Member States are invited to take the Commission’s opinion on their draft budgetary plan into account, in the process of adopting their budget law. However, recital 22 specifies that the extent to which that opinion has been taken into account in a Member State's budget law should be part of the assessment, if and when the conditions are met, leading to a decision on the existence of an excessive deficit in the Member State concerned. The respected wording of recital 21 (“budget plan”) and 22 (“budget law”) differ. Since these recitals are situated close to each other, one must read and interpret them coherent. Thus, the impact of the remarks of the European Commission reaches not only to a budget plan, but also to the budget law itself.

Second conclusion, the power to review draft national plans does not give the European Commission the right to change national budget plans (or budget laws), nor does it create an obligation for the Member States to follow the European Commission's opinion.

According to the existing legal environment, the European Commission may issue an opinion to national budget plan and shall request a revised plan. Only in exceptional cases of ‘particularly serious non-compliance’ the European Commission shall request a revision of a draft budgetary plan and shall adopt a new opinion (so the wording). It may not require any specific changes on the draft budget law itself. However, there are no consequences attached, if a Member State would not fulfill criteria foreseen in the wording of a given duty or in the opinion of the Commission on its budget plan.

Moreover, a budget plan may not correspond with a budget law. In theory, national budget law may (or even should) differ from the budget plan, which a Member State notifies to the European Commission. There is no legal duty that they match, which may create legal uncertainty. Therefore, very often there is no legal mechanism to enforce the fulfillment of the criteria of Stability and Growth Pact, but a political process.

2.1. Institutional and Member States’ Practices Regarding the Legislative Status quo

Using these tools, the European Commission was already considering stopping budgetary plans of some Member States

| [7] | European Commission. Commission opinion of 15.11.2013 on the Draft Budgetary Plan of FRANCE. Brussels, 15.11.2013, C(2013) 8004 final. |

[7]

. The European Commission was going to stop the budgetary plan of France 2014

| [7] | European Commission. Commission opinion of 15.11.2013 on the Draft Budgetary Plan of FRANCE. Brussels, 15.11.2013, C(2013) 8004 final. |

| [8] | European Commission. Communication from the Commission. 2014 Draft Budgetary Plans of the Euro area: overall assessment of the budgetary situation and prospects. Brussels, 15.11.2013, COM (2013) 900 final. |

| [9] | European Commission. COMMISSION RECOMMENDATION of 5.3.2014 regarding measures to be taken by France in order to ensure a timely correction of its excessive deficit. Brussels 5.3.2014. C (2014) 1498 final. |

| [10] | Frankfurter Allgemeine Zeitung GmbH. EU will Frankreichs Haushaltsplan stoppen. Available from:

https://www.faz.net/aktuell/wirtschaft/wirtschaftspolitik/stoppt-die-eu-frankreichs-haushalt-13191811.html (accessed on 24.03.2026) |

[7-10]

. In November 2018 the Commission rejected Italy’s budget plan

| [11] | European Commission. Press release. European Commission requests that Italy presents a revised draft budgetary plan for 2019. Strasbourg, 23 October 2018. Available from:

www.ec.europa.eu/commission/presscorner/detail/en/ip_18_6174 (accessed 31. March 2026). |

| [12] | European Commission. Report. Italy. Report prepared in accordance with Article 126(3) of the Treaty on the Functioning of the European Union. Brussels, 21.11.2018 COM(2018) 809 final. |

[11, 12]

. Also, the European Parliament criticized the Italian budget

. In response to that, Italy did revise its budget law

| [14] | European Commission. Annex to the Communication from the Commission. 2014 Draft Budgetary Plans of the Euro area: overall assessment of the budgetary situation and prospects. Brussels, 15.11.2013, COM (2013) 900 final. Annex I. |

[14]

. However, since the European Commission does not have right to demand that the Member State changes its budget plan or that it waits with the adoption of budget law until it receives an opinion on the revised budget plan, its right is more of a political than legal nature.

Experience shows that Member States do follow the opinions of the Commission issued regarding their budget laws. For instance, 2018 the European Commission had remarks respecting the budget plan submitted by Italy. In the course of the consultation process, Italy did change its draft. However, since the Commission may not issue a binding decision on a given budget plan, the Member State in question has discretion respecting following of Commission’s opinion or not. The solution suggested in this paper will improve the present situation. The current legal situation does not provide a sufficient legal certainty since the established system does not foresee any deadlines or concrete steps that must be taken within specified terms. Thus, actors involved do not know what to expect at which state of the process. The outcome of the consultation procedure may thus depend on diplomatic solutions or political measures, which can make it little transparent. Solution offered in this research will provide a faster tool and thus accelerate the process of imposing changes to a budget draft.

Due to the fact, that Member States do follow Commission’s opinions, there already exists a de facto consultation process with following of its – actually not binding opinions in national draft budgetary laws. The current proposal suggests a sophisticated legal mechanism that will increase legal certainty both on the side of the European institutions and Member States. It will enhance the cooperation of stakeholders and thus contribute to the legal certainty: the rights and obligations of both parties during the process will be clearer what will enhance legal certainty. Finally, the exchange of information and cooperation between the Member States would deepen the mutual trust and help.

A stronger legislative framework could shape the existing practices and lead to a more efficient approach. Possibly, other solutions and stronger rights of the Commission would be helpful and expedient in this regard. There are more sophisticated mechanisms in other areas, regarding obligations to consult (French:

obligation de consultation, German:

Pflichten der Mitgliedstaaten, die EU-Organe an der nationalen Rechtsetzung zu beteiligen, or simply

Beteiligungspflichten, Spanish:

obligación de consulta)

| [15] | an overview: Skowron-Kadayer, M. Obligations to Consult EU Institutions on National Draft Laws: A Dogmatic Analysis, European Review, 28.2.2020, pp. 343 – 356,

https://doi.org/10.1017/S1062798719000474 |

[15]

.

There are many obligations to consult EU institutions on national draft laws and one could attempt to find common ground between the obligation to consult in question (anchored in Two-Pack) and other (spread all over EU primary and secondary law). This comparison could enrich the current knowledge and thus offer and contribute new insights. The current knowledge misses comparisons between the tool to control national budget laws (as a new obligation this kind in fiscal law) and other measures, maybe similar, in different areas of European law. These may contain tools to avoid new crisis and support the stability of the financial markets.

The wording used by the EU legislature regarding different obligations to consult EU institutions on national draft laws differs very often, also does the impact. Different duties foresee e.g. consultation process or stand-still clauses. It could be advantageous to draw comparisons to the duty to notify national budget law and apply it to different scenarios, for example, if the Commission would have a right to propose changes to a national budget plan or it could stop the process due to a stand-still clause laid down in a regulation of the EU. This comparison could enrich the current knowledge and thus offer and contribute new insights. In this case it would not have to enforce changes by means of diplomatic pressure.

There are several obligations to consult EU institutions on national draft laws that foresee more sophisticated mechanisms than the one of the youngest ones – as known from Two-Pack

. Due to older provisions, a Union body may issue an approval

| [17] | Council Directive (EEC) 91/671 on the approximation of the laws of the Member States relating to the compulsory use of safety belts in vehicles of less than 3.5 tonnes (1991) OJ L 373/26. |

| [18] | Directive (EC) 2006/126 of the European Parliament and of the Council on driving licences (Recast) (2006) OJ L 403/18. |

| [19] | Directive of the European Parliament and of the Council laying down technical requirements for inland waterway vessels and repealing Council Directive 82/714 (EEC) (2006)OJ L 389/1. |

[17-19]

or

a confirmation in terms of Article 114 TFEU

| [20] | Consolidated version of the Treaty on the Functioning of the European Union, OJ C, 26.10.2012, pp. 47 – 390. |

[20]

. Further examples of a confirmation are laid down in different provisions

| [21] | European Parliament and Council Directive 94/62 on packaging and packaging waste (EC) (1994) OJ L 365/10. |

| [22] | Council Regulation (EC) No 2013/2006 amending Regulations (EEC) No. 404/93, (EC) No. 1782/2003 and (EC) No. 247/2006 with regards to the banana sector (2006) OJ L 384/13. |

| [23] | Council Regulation (EC) No. 247/2006 laying down specific measures for agriculture in the outermost regions of the EU (2006)OJ L 42/1. |

[21-23]

. Similar legal impact like a confirmation enjoys also a resolution, like laid down in Article 108 TFEU

| [20] | Consolidated version of the Treaty on the Functioning of the European Union, OJ C, 26.10.2012, pp. 47 – 390. |

[20]

, which foresees a resolution of an EU institution towards a national draft law. An EU institution may also foresee a specific content of national draft. Due to some laws, it is also possible to prevent the enforcement of national law that does not fulfill the requirements of the Commission. The content of the new Member State law depends on the upstream consultation process and – in some cases – the act of consultation of an EU institution

| [24] | Streinz R. in: Streinz, Vertrag über die Europäische Union/Vertrag über die Arbeitsweise der Europäischen Union (2012) Art. 4 EUV (para 59). |

[24]

. The EU institutions influence the process of national legislation and the substantive national law by their participation.

2.2. Different Mechanisms Included in Obligations to Consult EU Institutions on National Draft Laws

The duty to notify a national budget plan according to article 7 of the Regulation No. 473/2013 constitutes an obligation to consult

| [15] | an overview: Skowron-Kadayer, M. Obligations to Consult EU Institutions on National Draft Laws: A Dogmatic Analysis, European Review, 28.2.2020, pp. 343 – 356,

https://doi.org/10.1017/S1062798719000474 |

[15]

. The preventive control of national laws exercised under Two-Pack is nothing new. EU law knows similar obligations to consult EU institutions on national law drafts since tens of years

| [15] | an overview: Skowron-Kadayer, M. Obligations to Consult EU Institutions on National Draft Laws: A Dogmatic Analysis, European Review, 28.2.2020, pp. 343 – 356,

https://doi.org/10.1017/S1062798719000474 |

[15]

.

In the light of different provisions, the given EU institution proposes content to, postpones, or prevents the enforcement (by exercising a right of veto) of a national law that would disturb the internal market. In some cases, the national legislative procedure may only be continued if the competent EU institution does not issue a statement or a negative opinion

| [25] | Commission Regulation (EC) 423/2008 on laying down certain detailed rules for implementing Council Regulation (EC) No. 1493/1999 and establishing a Community code of oenological practices and processes (2008) OJ L 127/13; Decision of the Council (1983) OJ L 347/48 – 49. |

[25]

in due time with respect to national law

| [16] | Skowron-Kadayer, M. Effet utile du contrôle préventif by hybrid legislative procedures, European Review, 28.3.2020, pp. 470 – 482, https://doi.org/10.1017/S1062798719000607 |

| [17] | Council Directive (EEC) 91/671 on the approximation of the laws of the Member States relating to the compulsory use of safety belts in vehicles of less than 3.5 tonnes (1991) OJ L 373/26. |

[16, 17]

. A Union institution can give its approval or confirmation or issue a resolution.

First obligations were anchored in the Treaty on the Functioning of the European Union – the primary EU law. Art. 117 and 108 TFEU

| [20] | Consolidated version of the Treaty on the Functioning of the European Union, OJ C, 26.10.2012, pp. 47 – 390. |

[20]

constitute examples of such obligations to consult

| [15] | an overview: Skowron-Kadayer, M. Obligations to Consult EU Institutions on National Draft Laws: A Dogmatic Analysis, European Review, 28.2.2020, pp. 343 – 356,

https://doi.org/10.1017/S1062798719000474 |

[15]

. The Contracting States agreed on respected duties anchored in the Treaty. A Union institution can recommend to the States concerned some measures (Art. 117 TFEU) or issue a decision (Art. 108 TFEU). These and other provisions did not change over the years. However, with the passage of time, more and more secondary law acts contain obligations to consult. Regarding obligations to consult anchored in secondary law acts the EU legislature decided on participation of EU institutions in national legislative procedures.

2.2.1. Consultation of an EU Institution – the European Commission

According to Article 117 para 1 TFEU

| [20] | Consolidated version of the Treaty on the Functioning of the European Union, OJ C, 26.10.2012, pp. 47 – 390. |

[20]

a Member State desiring to proceed with national law shall consult the Commission, if there is a reason to fear that the adoption or amendment of a provision laid down by law, regulation or administrative action may cause distortion within the meaning of Article 116

| [20] | Consolidated version of the Treaty on the Functioning of the European Union, OJ C, 26.10.2012, pp. 47 – 390. |

[20]

. After consulting the Member States, the Commission shall recommend to the States concerned such measures as may be appropriate to avoid the distortion in question, Article 117 para 2 TFEU

| [20] | Consolidated version of the Treaty on the Functioning of the European Union, OJ C, 26.10.2012, pp. 47 – 390. |

[20]

.

2.2.2. Consultation of an EU Institution – the ECB

According to article 127 para 4 TFEU

| [20] | Consolidated version of the Treaty on the Functioning of the European Union, OJ C, 26.10.2012, pp. 47 – 390. |

[20]

the European Central Bank shall be consulted by national authorities regarding any draft legislative provision in its fields of competence, but within the limits and under the conditions set out by the Council in accordance with the procedure laid down in Article 129(4) TFEU

| [20] | Consolidated version of the Treaty on the Functioning of the European Union, OJ C, 26.10.2012, pp. 47 – 390. |

[20]

. The European Central Bank may submit opinions to the appropriate Union institutions, bodies, offices or agencies or to national authorities on matters in its fields of competence.

Article 5 of the Directive 2006/87 foresaw a consultation of the Commission on national technical requirements that each Member State may adopt

| [26] | 2006/87/EC Directive of the European Parliament and of the Council of 12 December 2006 laying down technical requirements for inland waterway vessels and repealing Council Directive 82/714/EEC, OJ L 389, 30.12.2006, p. 1–260 (no longer in force). |

[26]

.

2.2.3. Approval of the European Commission Regarding National Draft Law

Examples for an approval of the European Commission are anchored in primary and secondary law. Article 114 TFEU foresees an approval of the Commission regarding measures of Member States (“the Commission shall … approve …”).

Article 6 of the Directive of 16 December 1991 on the approximation of the laws of the Member States

| [27] | Council Directive of 16 December 1991 on the approximation of the laws of the Member States relating to compulsory use of safety belts in vehicles of less than 3,5 tonnes (91/671/EEC), Official Journal L 373, 31/12/1991 P. 0026 – 0028. |

[27]

relating to compulsory use of safety belts in vehicles of less than 3,5 tonnes (91/671/EEC) foresees an agreement of the Commission regarding national regulations.

Art. 5 para 2 subpara 2 of the Directive 2006/87/EC

| [26] | 2006/87/EC Directive of the European Parliament and of the Council of 12 December 2006 laying down technical requirements for inland waterway vessels and repealing Council Directive 82/714/EEC, OJ L 389, 30.12.2006, p. 1–260 (no longer in force). |

[26]

foresaw a “prior approval” of the Commission regarding amendments to technical requirements of Member States.

2.2.4. Confirmation of the European Commission Regarding National Draft Law

According to article 6 para 6 of the Directive 94/62

| [28] | European Parliament and Council Directive 94/62/EC of 20 December 1994 on packaging and packaging waste, OJ L 365, 31.12.1994, p. 10–23. |

[28]

Member States set programmes going beyond the targets set in this legal act. They shall inform the Commission thereof. The Commission shall confirm these measures, after having verified, in cooperation with the Member States, that they are consistent with the considerations laid down in this legal act and do not constitute an arbitrary means of discrimination or a disguised restriction on trade between Member States (article 6 para 6 sentence 3). The legal act the Commission issues in this case is a confirmation of national measures.

2.2.5. Decision of the European Commission Regarding National Draft Law

Council Regulation No 2013/2006 foresaw in article 3 an amendment of the Regulation No 247/2006

| [29] | Council Regulation (EC) No 247/2006 of 30 January 2006 laying down specific measures for agriculture in the outermost regions of the Union, OJ L 42, 14.2.2006, p. 1–19 (no longer in force). |

[29]

. Article 24a shall be inserted. This provision foresaw in para 1 that Member States submit to the Commission the draft amendments to their overall programme to reflect the changes introduced by Regulation (EC) No 2011/2006. According to para 2 the Commission shall evaluate the amendments proposed and decide on their approval within four months of their submission. This regulation ruled on an approval of the Commission regarding national measures.

2.2.6. Right of the European Commission to Propose Amendments Regarding National Draft Law

There are also provisions that confer the right to propose amendments in the EU law. According to those rules, the Commission may propose changes to national draft laws. If the Commission exercises its right, it corresponds with the obligation of a Member State to change the national draft, respectively.

Article 7 para 1 of the Regulation No 336/2006

| [30] | Regulation (EC) No 336/2006 of the European Parliament and of the Council of 15 February 2006 on the implementation of the International Safety Management Code within the Community and repealing Council Regulation (EC) No 3051/95, OJ L 64, 6.3.2006, pp. 1 – 36. |

[30]

a Member State may derogate from the rules laid down in this act. Member State may establish alternative certification and verification procedures. In this case, it shall notify the Commission of the derogation and of the measures which it intends to adopt. According to para 3 lit b) the Member State may be required to amend or refrain from adopting the proposed provisions, if “it is decided” – within six months of the notification – that the proposed derogation is not justified or that the proposed measures are not sufficient. In this case the Commission – issuing amendments – proposes changes to national draft law.

2.2.7. Statement of an EU Institution or Another Member State Regarding National Draft Law

Other rules of EU law allow Member States to continue national legislative procedures within certain period of time or if neither the Commission nor different Member State complained that the planned and notified measure does not satisfy the goals of the EU.

The provisions of the Information-Directive

| [31] | Directive (EU) 2015/1535 of the European Parliament and of the Council of 9 September 2015 laying down a procedure for the provision of information in the field of technical regulations and of rules on Information Society services, OJ L 241, 17.9.2015, p. 1–15. |

[31]

constitute an example for this kind of rules of law. Article 6 Para 2 foresees detailed opinions of the Commission regarding the national draft technical regulation. Within a certain period of time, the Commission reviews the national draft in order to see if it could create obstacles to the free movement of goods within the internal market.

2.2.8. Submission of Changed National Draft

According to article 5 para 1 of the Council regulation 479/2008

| [32] | Council Regulation (EC) No 479/2008 of 29 April 2008 on the common organisation of the market in wine, amending Regulations (EC) No 1493/1999, (EC) No 1782/2003, (EC) No 1290/2005, (EC) No 3/2008 and repealing Regulations (EEC) No 2392/86 and (EC) No 1493/1999, OJ L 148, 6.6.2008, p. 1–61. |

[32]

each producer Member State referred to in Annex II shall, for the first time by 30 June 2008, submit to the Commission a draft five-year support programme containing measures in accordance with this Chapter. These programmes shall become applicable three months after their submission to the Commission. Should the submitted support programme not comply with the conditions laid down in this regulation, the Commission shall inform the Member State thereof. In such case, the notifying Member State shall submit a revised support programme to the Commission. The revised support programme shall become applicable two months after its notification unless an incompatibility persists in which case this subparagraph shall apply.

3. Results

The present study invites to develop solutions respecting SGP. Based on the above one can differ between simple and qualified obligations to consult EU institutions on national draft laws

| [15] | an overview: Skowron-Kadayer, M. Obligations to Consult EU Institutions on National Draft Laws: A Dogmatic Analysis, European Review, 28.2.2020, pp. 343 – 356,

https://doi.org/10.1017/S1062798719000474 |

| [33] | Skowron-Kadayer M. (2018) Die Beteiligung der Organe Europäischen Union an der Rechtsetzung der Mitgliedstaaten [The participation of the EU institutions in national legislative procedures]. C. H. Beck, Warsaw. |

[15, 33]

. Art. 117 TFEU is an example for a

simple obligation to consult. Examples for qualified obligations to consult constitute Article 108, 114 TFEU and Articles 5 and 6 of the Information Directive

| [31] | Directive (EU) 2015/1535 of the European Parliament and of the Council of 9 September 2015 laying down a procedure for the provision of information in the field of technical regulations and of rules on Information Society services, OJ L 241, 17.9.2015, p. 1–15. |

[31]

. Qualified obligations to consult contain duties to notify and to conduct a consultation process (just as simple obligations to consult) as well as a stand-still clause, as the qualifying element. Not all the qualified obligations to consult contain a stand-still clause. Respected duties may contain a stand-still clause in their wording or a similar element forcing a Member State to wait with the finalization of the national legislative procedure until the EU institution did not issue an act respecting national draft, constituting qualified obligations to consult. Some obligations to consult foresee an approval of the Commission towards national law draft. In this case, the essence of an approval is similar – the notifying Member State may not pursue the national legislative procedure until it does not obtain the approval of the EU institution. Moreover, Member State’s legislative procedures must wait in these cases for this act of an EU institution and – in some cases – respect its essence in their wording.

3.1. Goals of the Process of Consultation and Participation of EU Institutions in National Legislative Proceedings

The interference in the national legislative process by the participation of a competent EU institution constitutes a rather strong measure so that it cannot be an end in itself but it serves further purposes. The goal of an ex ante participation of EU institutions in national legislative procedures is the protection of the internal market. A single Member State cannot examine effects of a given national law provisions on other Member States’ legal orders or on Europe as a whole. That is why it depends on the know-how of EU institutions. They possess the required expertise and ability to assess the Europe-wide effect of a new national law in question. This makes up the background of the influence of those institutions on national draft laws.

While the notifying Member State fulfills its secondary duty

| [15] | an overview: Skowron-Kadayer, M. Obligations to Consult EU Institutions on National Draft Laws: A Dogmatic Analysis, European Review, 28.2.2020, pp. 343 – 356,

https://doi.org/10.1017/S1062798719000474 |

[15]

resulting from an obligation to consult an EU institution on national draft and takes the detailed opinion of the Commission or other Member States into account (for example Article 6(2) of the Information-Directive

| [31] | Directive (EU) 2015/1535 of the European Parliament and of the Council of 9 September 2015 laying down a procedure for the provision of information in the field of technical regulations and of rules on Information Society services, OJ L 241, 17.9.2015, p. 1–15. |

[31]

) or follows the Commission’s recommendation (Article 117 TFEU

| [20] | Consolidated version of the Treaty on the Functioning of the European Union, OJ C, 26.10.2012, pp. 47 – 390. |

[20]

), it transfers the content of the respected opinion or recommendation into national draft law. This legal act (either of the EU institution or another Member State) contains substantive provisions that a Member State must respect and follow in the draft. It offers advice and help to shape national draft in a way that fulfills requirements of the EU institutions and thus make the notified draft confirm with EU law.

Thus, the fulfillment of the primary duty (to notify, inform a given EU institution) resulting from an obligation to consult EU institution on national draft laws does not guarantee that this respected draft complies with EU law. Only the following of the secondary duty to transfer the content of the recommendation or opinion respecting national draft can provide some security that the national draft in question will comply with EU law. This also makes the essence of obligations to consult EU institutions and – as in case of Information-Directive – Member States on national draft laws. However, the legal act of the EU Commission, issued based on article 117 para 1 TFEU

| [20] | Consolidated version of the Treaty on the Functioning of the European Union, OJ C, 26.10.2012, pp. 47 – 390. |

[20]

also contains the opinion of other Member States on national draft. This is due to the sentence 2 of this paragraph, foreseeing that the Commission – “after consulting the Member States” – shall recommend to the States concerned such measures as may be appropriate to avoid the distortion in question.

One of the obligations constitutes the control of Member States’ budgetary laws. It does not refer to the internal market matters but deals with the Stability and Growth Pact. Since its inception, the SGP has known the requirement to submit stability [ins] (Section 2 of Council Regulation) or convergence [outs] programmes (Section 3 of Council Regulation), including on the ‘medium-term objective for the budgetary position of close to balance or in surplus’

| [34] | Council Regulation (EC) No. 1466/97 of 7 July 1997 on the strengthening of the surveillance of budgetary positions and the surveillance and coordination of economic policies, OJ L 209, 2.8.1997, p. 1–5. |

[34]

. For instance, article 3 para 1 of this Regulation speaks of “information” necessary for the purpose of multilateral surveillance. It specifies that a stability programme shall present ‘a description of budgetary and other economic policy measures being taken and/or proposed to achieve the objectives of the programme, and, in the case of the main budgetary measures, an assessment of their quantitative effects on the budget’. Article 7 contains similar regulations regarding a convergence programmes.

Thus, some matters respecting national budgets had already been the subject of prior notification requirements under the SGP since 1997. However, they have been less incisive, strict and specific than the provisions of Two-Pack. Two-Pack Regulation

| [4] | Regulation (EU) No 473/2013 of the European Parliament and of the Council of 21 May 2013 on common provisions for monitoring and assessing draft budgetary plans and ensuring the correction of excessive deficit of the Member States in the euro area, OJ L 140, 27.5.2013, p. 11–23. |

[4]

established the first obligation of its kind in EU fiscal law. The scope of application of obligations to consult has thus been extended from internal market issues (direct obligations to consult) to sensitive fiscal policy matters (for indirect obligations to consult EU institutions on draft plans (not laws)). The duty to notify budgetary plans established a new coordination policy and it thus could constitute a pre-stage of a uniform (harmonized) Eurozone budget, as France suggests it. At the same time, current knowledge may lack efficient tools for preventing financial crisis or a thorough discussion about it. It also overlooks that the obligation to consult EU institutions on national budget laws (Two-Pack) is not the only one in the EU law. That is why a detailed research on obligations to consult can and should enjoy greater practical importance.

3.2. Direct and Indirect Obligations to Consult EU Institutions

Art. 7 of Regulation No. 473/2013 (Two-Pack)

| [4] | Regulation (EU) No 473/2013 of the European Parliament and of the Council of 21 May 2013 on common provisions for monitoring and assessing draft budgetary plans and ensuring the correction of excessive deficit of the Member States in the euro area, OJ L 140, 27.5.2013, p. 11–23. |

[4]

foreseeing an ex ante control of national budgetary plans is constructed in a similar way as Article 117 TFEU

| [20] | Consolidated version of the Treaty on the Functioning of the European Union, OJ C, 26.10.2012, pp. 47 – 390. |

[20]

and thus constitutes a simple obligation to consult. However, since it does not foresee a consultation on the legislative draft itself, but on a plan, it may be seen as a rather untypical obligation to consult, since the opinion of the Commission refers to the national plan and not the draft national (budget) law itself. One could thus introduce a further category of obligations to consult: direct and indirect ones. Direct obligations to consult would be the ones that refer to the draft national law itself. An example for the category of the indirect obligations to consult constitutes the control of national budgets that refers to a plan (regarding a law) and not the draft law itself. At the same time, it is not clear what is the legal nature of the budget plan in terms of Regulation 473/2013 under national laws. One thus can not specify it this obligation means a real “law” or rather interior administrative regulation without any external effect(s). The legal nature of this specific obligation to consult may differ in several ways from all the other obligations described above.

3.3. Application of Solutions Known from Direct Obligations to Consult to the Category of Indirect Ones

Some of the areas in which obligations to consult rule the relationships between the Member States and EU institutions during national legislative procedures are sensible and demand a clear demarcation of competences between the Member States and the European Union. At the same time, based on previous statements it is worth considering if the duty to consult EU institution anchored in article 7 of the Regulation 473/2013 is perfect as it is or if there is some possibility to draft this provision clearer. Some other (typical) obligations to consult contain clear demarcation of competences between the EU institutions and national legislatures.

Among the two categories of obligations to consult known from previous research

| [15] | an overview: Skowron-Kadayer, M. Obligations to Consult EU Institutions on National Draft Laws: A Dogmatic Analysis, European Review, 28.2.2020, pp. 343 – 356,

https://doi.org/10.1017/S1062798719000474 |

| [31] | Directive (EU) 2015/1535 of the European Parliament and of the Council of 9 September 2015 laying down a procedure for the provision of information in the field of technical regulations and of rules on Information Society services, OJ L 241, 17.9.2015, p. 1–15. |

[15, 31]

– simple and qualified obligations to consult – the duty to participate the Commission during national legislative procedure constitutes a simple obligation to consult

| [15] | an overview: Skowron-Kadayer, M. Obligations to Consult EU Institutions on National Draft Laws: A Dogmatic Analysis, European Review, 28.2.2020, pp. 343 – 356,

https://doi.org/10.1017/S1062798719000474 |

[15]

. It is thus worth consideration to apply solutions known from direct simple obligations to consult to this indirect duty to consult EU Commission on national budget plan.

4. Conclusions

The European Commission and Member States, once they review the functioning of the budgetary control and prepare a new impact assessment, may be keen to look for different solutions in other areas of EU law. The strengthening of the legal framework regarding the budgetary control exercised by the EU Commission should be based on already existing similar cases (review of national draft laws – direct obligations to consult), such as a process of consultation according to article 127 TFEU

| [20] | Consolidated version of the Treaty on the Functioning of the European Union, OJ C, 26.10.2012, pp. 47 – 390. |

[20]

or issuing a statement according to article 117 TFEU

| [20] | Consolidated version of the Treaty on the Functioning of the European Union, OJ C, 26.10.2012, pp. 47 – 390. |

[20]

. The review of competencies transferred to the European institutions in the past, can provide a basis for a comparative analysis and suggest new tools for supervision of national budget laws.

The existing mechanism should be extended by further and more specific opinion rights of the European Commission or – if possible, maybe even some rights of other Member States (as it is in case of the Information-Directive) – regarding national budget plans and laws. One can think of implementing a stand-still clause into article 7 of the Regulation 473/2013. In this case a Member State could not issue a budget law if the budget plan would not have the content, the EU Commission foresaw in its opinion towards the notified national plan. One could think of a stand-still clause that would not allow a Member State in question to adopt the budget law until the European Commission did not issue an opinion on it or a consultation process between a European institution and national constitutional body on budget plan is still ongoing.

Different solution would be to expect a positive opinion of the European Commission towards national budgetary plan. According to that a Member State could not adopt its legislation on budget law before European Commission has issued a positive opinion on draft budgetary plan. This would add more legal certainty to the process. The consultation process itself would be more transparent and open.

Worth noticing is that Member States laws may not know the category of a “budget plan”, as article 7 of the Regulation 473/2013 states. This may require a further legislation in national law (national constitutions or rule of law regarding the budgetary procedure) that would establish a connection between a (budget) plan, that may not enter into force until its content does not comply with the content of the opinion of the Commission. Otherwise, article 7 of this Regulation might be changed and foresee a budget law (and not a plan) as well as a stand-still clause in its wording. The necessity to have a budget prior to a new calendar year is met by the wording of article 7 para 1 of the Regulation 473/2013 that foresees the adoption of the Commission’s opinion until 30th November each year.

One could also dare a comparison with article 117 TFEU and change the article 7 of the Regulation 473/2013 itself. This proposal contains a resignation on “plan” and implementation of “budgetary law” in the wording of para 1 of article 7. However, the obligation to notify the budgetary law should not apply unconditionally as it is now but it should be effective solely if there is a reason to fear that the adoption of the national budgetary law may cause distortion within the meaning of SGP, a Member State desiring to proceed therewith shall consult the Commission. In this case the distortion of competition in terms of article 117 TFEU will be replaced by criteria origination from SGP. Its goals are sound government finances, price stability and strong sustainable growth conducive to employment creation or – as article 1 of the Regulation No 1466/97

| [34] | Council Regulation (EC) No. 1466/97 of 7 July 1997 on the strengthening of the surveillance of budgetary positions and the surveillance and coordination of economic policies, OJ L 209, 2.8.1997, p. 1–5. |

[34]

foresees it – the prevention of the occurrence of excessive general government deficits and to promote the surveillance and coordination of economic policies. Since some Member States adopted the single currency or are going to participate in a common budget, it could be beneficial to establish an exchange of their experiences and let the Commission consult other Member States on a budget plan of the notifying Member State. Member States experiencing problems could exchange information, necessary data and experience with countries who follow strict fiscal policy and save.

Another conceivable approach would be also to divide a given budget plan to different sections and introduce an appropriate approach respecting to a specific section. For example, national expenses regarding national security could depend solely on an opinion of the European Commission, while other costs (e.g. education or investment in renewable energy (“Green Deal”)) could depend on a consultation process and a stand-still clause.