Abstract

Pension expenditures have become a critical fiscal challenge for the Government of Punjab, surging to Rs. 312 billion in the fiscal year 2022-23. The accrued pension liability now stands at Rs. 6.5 trillion, significantly constraining the government's capacity for current and development expenditures. This study explores the existing regulatory framework for pension liability management and proposes actionable solutions based on global best practices. Through a comprehensive methodology that includes literature reviews, data analysis, comparative studies of national and international practices, and stakeholder interviews, the research highlights alarming trends: a 300% increase in government revenues over the past decade, contrasted with a staggering 650% rise in pension costs. Key contributors to this fiscal burden include the Defined Benefit pension scheme, regularization of temporary employees, and adverse judicial rulings. To address these challenges, the study recommends transitioning to a contributory pension scheme, reducing commutation rates, aligning pensionable pay with basic pay, indexing pension increases, and leveraging biometric verification systems. Additionally, amendments to the Civil Servants Act and better management of the Punjab Pension Fund are proposed to ensure fiscal sustainability. These measures aim to mitigate the growing financial strain, ensuring long-term stability and efficient pension liability management for the Government of Punjab.

Keywords

Compound Annual Growth Rate, Implementation and Coordination, Consumer Price Index, Pension, National Pension System, Financial Year, Government of Pakistan

1. Introduction

Pension is defined as a “stated allowance out of the public treasury granted by government to an individual or his representative for his valuable services upon retirement”.

| [1] | Abonyi, S. E., & Okoye, U. O. (2023). A comparative assessment of the social and emotional wellbeing of Nigerian retirees under the Defined Benefits and contributory pension system. Indian Journal of Gerontology, 37(1), 126-154. |

[1]

Historically, pension in Pakistan draws its legal sanction from the following legislations:

1) The British Pension Act, 1871

2) Pension-cum-gratuity Scheme, 1954

3) Provisions of Civil Servant Act, 1973

4) The Liberalized Pension Rules and Ancillary Instrutions, 1977

The Government of Punjab currently offers a Defined-Benefit (DB) Pension Scheme for its permanent employees under Section 18 of the Punjab Civil Servants Act, 1974. The pension scheme is being managed on a ‘pay-as-you-go’ basis, meaning that pension payments during a year are made out of that year’s government revenues, regardless of the time of accrual of pension liability. Pension has now become one of the largest expenses of the Government of Punjab’s current revenue expenditure. The exponential growth of pension expenditure has consequently emerged as a key fiscal risk. A number of initiatives have been made over the last 15 years to address these problems. These attempts apparently fell short of yielding tangible outcomes since pension expenditures continue to rise. An additional challenge has been to find the delicate balance between the financial outlay and the well-being of the retired government employees.

Pension expenditure has risen rapidly over the last decade making it a key fiscal risk for the Government of Punjab. It has increased exponentially by 767% from Rs. 36 billion in FY 2010-11 to Rs. 312 billion in FY 2022-23 and is being paid from the Provincial Consolidated fund. The ratio of pension expenditure as against General Revenue Receipts has increased from 6.8% in FY 2010-11 to 14.9 % in FY 2021-22 effectively doubling in just a decade. The total accrued liability of pensions of the Government of Punjab today stands at Rs. 6.5 trillion which, being twice the total provincial budget, creates a lot of uncertainty in the provincial fiscal operations. If this trend persists, pension expenditure will reach unsustainable levels drastically affecting the capacity of the province to fund its public service delivery and development priorities.

Although the problem of managing pension liabilities exists at Federal and Provincial levels. However, the comparison is limited to the extent of KPK for this study. This research has made strenuous efforts to address the following scope:

a) To analysis of the existing financial burden of pension liabilities on the Government of Punjab.

b) Evaluate the efficiency of the existing pension system with regards to managing the rising economic load on the finances of the Government of Punjab.

c) Review the efforts of the Government of Punjab in introducing reforms in the current legal and procedural framework.

d) Develop an implementation strategy with an action plan for a sustainable and effective pension management system acceptable to all stakeholders.

e) Suggest a contingency plan in case of roadblocks in the implementation of the proposed reforms.

How is the Government of Punjab managing the pension liability and what could be done to reduce the burden of pension liability on the Provincial Consolidated Fund?

2. Literature Review

Effective management of pension liabilities demands a comprehensive and integrated strategy, it includes actuarial assumptions, risk management

| [1] | Abonyi, S. E., & Okoye, U. O. (2023). A comparative assessment of the social and emotional wellbeing of Nigerian retirees under the Defined Benefits and contributory pension system. Indian Journal of Gerontology, 37(1), 126-154. |

[1]

, communication, investment strategies, funding policies, plan design,

| [2] | Ahmad, R., Mi, H., Keyao, R., Khan, K., & Navid, K. (2018). Aging and social security system in Pakistan: policy challenges, opportunities, and role of China–Pakistan Economic Corridor (CPEC). Educational gerontology, 44(9), 537-550. |

[2]

governance and education

| [3] | Awais, M., Laber, M. F., Rasheed, N., & Khursheed, A. (2016). Impact of financial literacy and investment experience on risk tolerance and investment decisions: Empirical evidence from Pakistan. International Journal of Economics and Financial Issues, 6(1), 73-79. |

[3]

. The literature emphasizes how crucial it is to coordinate these numerous factors in order to guarantee the long-term viability of pension plans and reduce the financial risks related to pension liabilities

| [4] | Berstein, S., Fuentes, O., & Villatoro, F. (2013). Default investment strategies in a Defined Contribution pension system: a pension risk model application for the Chilean case. Journal of Pension Economics & Finance, 12(4), 379-414. |

[4]

. The government and organizations in charge of handling pension plans in Pakistan face considerable issues due to the country's pension accountability

| [5] | Ebbinghaus, B. (2015). The privatization and marketization of pensions in Europe: A double transformation facing the crisis. European Policy Analysis, 1(1), 56-73. |

[5]

. In Pakistan, managing the pension liabilities requires accurate actuarial assumptions. Awais, Laber

| [5] | Ebbinghaus, B. (2015). The privatization and marketization of pensions in Europe: A double transformation facing the crisis. European Policy Analysis, 1(1), 56-73. |

[5]

, suggests that estimating factors such as life expectancy, salary growth rates, and inflation rates specific to the Pakistani context is essential. Additionally, efficient risk management methods, such as the application of stochastic modelling and stress testing, can assist in determining and minimizing the impact of market turbulence and demographic changes on pension liabilities

| [4] | Berstein, S., Fuentes, O., & Villatoro, F. (2013). Default investment strategies in a Defined Contribution pension system: a pension risk model application for the Chilean case. Journal of Pension Economics & Finance, 12(4), 379-414. |

[4]

.

Another research emphasizes that pension liabilities are mostly managed through the funding strategy and investment tactics implemented by pension schemes

| [6] | Josa-Fombellida, R., López-Casado, P., & Navas, J. (2023). A Defined Benefit pension plan model with stochastic salary and heterogeneous discounting. ASTIN Bulletin: The Journal of the IAA, 53(1), 62-83. |

[6]

. Previous studies have highlighted the need for maintaining a suitable capital level and implementing a diversified investment strategy that takes into account local market conditions and risk appetite

| [7] | Naqvi, B., Rizvi, S. K. A., & Shahzad, A. (2023). Selection of Retirement Saving Plan for a Private-sector Employee in Pakistan. Asian Journal of Management Cases, 20(1), 23-34. |

| [8] | Naughton, J. P. (2019). Regulatory oversight and trade-offs in earnings management: evidence from pension accounting. Review of Accounting Studies, 24, 456-490. |

[7, 8]

. Ahmad, Mi

| [9] | Oladeinde, O. (2021). Political economy of pension reforms in Nigeria: Evaluating the institutional trajectory and roles of international policy advisors. International Journal of Developing and Emerging Economies, 9(1), 48-63. |

[9]

, indicated that that it may be advantageous to match the investment strategy with the specific obligations of the plan.

Reforms include changing Defined Benefit (DB) pension plans to Defined Contribution (DC) pension plans or implementing hybrid pension plans can assist limit future pension liabilities and manage risks

| [10] | Sandberg, J. (2013). (Re-) interpreting fiduciary duty to justify socially responsible investment for pension funds? Corporate Governance: An International Review, 21(5), 436-446. |

[10]

. Additionally, modifying retirement ages, payout formulae, and cost-sharing agreements may help Pakistani pension programs remain viable in the future.

3. Research Methodology

The Research has used both qualitative and quantitative methods for a holistic research. Structured and semi-structured interviews of the subject specialists and public policy practitioners were conducted. The secondary sources consulted for this report include the following:

a) The Constitution of the Islamic Republic of Pakistan, 1973

b) Punjab Civil Servants Act 1974

c) Punjab Pension Fund Act 2007

d) Punjab Civil Services Pension Rules 2008

e) Khyber Pakhtunkhwa Civil Servants Pension Rules 2021

f) Khyber Pakhtunkhwa Contributory Pension Rules 2022

g) State Bank of Pakistan Quarterly report 2021-22

h) Burgeoning Pension Bill Implications and Way forward

i) Management of Pension Liabilities-The case of Punjab 2018

j) Pakistan Assessment of Civil Service Pensions 2020

k) Assessing Chile's Pension System: Challenges and Reform Options IMF Working Paper 21

The data collected from primary and secondary sources has been summarized and presented through charts and summary statistics. This has helped in understanding the basic characteristics and patterns in the data. Moreover, the exploratory analysis in which relationship patterns and trends in the data were explored. In addition, time series analysis has also been employed to understand the accrued pension liabilities and future projections through actuarial analysis.

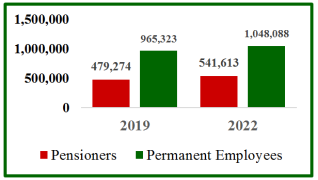

3.1. Pensioner & Employees Statistics

At the very outset, the RG observed that the number of pensioners in Punjab has significantly increased to 0.5 million (S&GAD, GoPb) which is equal to fifty percent of working employees thus posing a major challenge. The comparative data of pensioner’s vis a vis permanent employee as on 30

th June 2019 and 30

th June 2022 reveals that number of pensioners increased by 13% as compared to permanent employees which approximates increased by 8.57% in the said period

| [15] | Wahab, M., Mufti, O., & Khan, M. A. (2017). The Effects of Population Ageing on the Public Pension System in Pakistan. Abasyn University Journal of Social Sciences, 10(2). |

[15].

This shows that not only the number of pensioners is significantly high as compared to working employees but also increasing at a higher rate which will further aggravate the situation in future.

Figure 1. The Pensioners and Employees Statics, Punjab.

Policy and Institutional Arrangement

Pension Benefits and Magnitude of Employee Related Benefits

This research found that after liberal interpretation of the Courts, pension benefits last longer than the active service rendered by employees. The calculation of pension period is as under:

1) The average pension duration after superannuation (life expectancy of 82 years) is 22 years.

2) Average pension duration of family considering that Spouse is 5 years younger than husband; life expectancy of 87 years adds 10 years.

3) Another addition in pension duration is added by widowed/divorced daughter for 10 years.

4) Therefore, total pension duration after superannuation is 42 years as against average 32 years of active service by the employee (Finance Department, GoPb, 2023).

3.2. Government of Punjab’s Efforts to Manage Pension Liability

3.2.1. Pension Benefits and Magnitude of Employee Related Benefits

Over the last one and half decade, the Government of Punjab took several steps to manage the pension liability on corporate lines and thus reduce the burden on the provincial exchequer. Government’s flagship project in this regard was the enactment of Punjab Pension Fund Act 2007 and resultantly establishment of Punjab Pension Fund.

3.2.2. Punjab Pension Fund

The Government of Punjab introduced Punjab Pension Fund Act in 2007 to handle pension liability. The government was supposed to make regular contributions to the fund, however, the government only invested Rs. 40 billion since 2007 and the total portfolio as of today stands at Rs. 105 billion which is not sufficient to handle the pension liabilities

| [12] | Baggot, D. M., Hensinger, B., Parry, J., Valdes, M. S., & Zaim, S. (2005). The new hire/preceptor experience: cost-benefit analysis of one retention strategy. JONA: The Journal of Nursing Administration, 35(3), 138-145. |

[12]

. The details of investment made by PPF is as in table:

Table 1. Pension Investment Categories and Current Status.

Investment Category | 31st March 2023 | 30th June 2022 |

Amount | % | Amount | % |

PIBs – Floating Rate | 45,813 | 45.58% | - | - |

PIBs – Fixed Rate | 901 | 0.90% | 771 | 0.82% |

National Saving Schemes | 23,815 | 23.69% | 42,812 | 45.53% |

Mutual Funds - Equity | 12,052 | 11.99% | 13,051 | 13.88% |

Shares of Listed Companies | 7,717 | 7.68% | 7,953 | 8.46% |

Accrued Markup | 3,207 | 3.19% | 979 | 1.04% |

Corporate Bonds & Preference Shares | 4,090 | 4.07% | 2,947 | 3.13% |

Mutual Funds - Fixed Income | 817 | 0.81% | 9,419 | 10.02% |

T-Bills | 941 | 0.94% | - | - |

Total Fund Size | 100,515 | 100.00% | 94,026 | 100.0% |

Evidently, the Punjab Pension Fund has so far implemented a very conservative investment policy mainly investing in government securities and national saving scheme which did not yield high profit margins hovering around 12% only

| [15] | Wahab, M., Mufti, O., & Khan, M. A. (2017). The Effects of Population Ageing on the Public Pension System in Pakistan. Abasyn University Journal of Social Sciences, 10(2). |

[15]

. Moreover, the profits earned by the PPF are not remitted to the GoPb to help ease the burden on the Provincial consolidated fund. Instead, the profits are reinvested and thus creates the façade of pension liability management on corporate lined but instead, the fund seems to have become an end in itself. As the government did not invest in the Pension Fund the fund is unable to contribute significantly to the discharge of pension liabilities that today stand at Rs. 320 bn for which the size of the fund needs to be around Rs. 2 trillion at current interest rates (Sajid, M. GM PPF, 2023).

3.2.3. Defined Benefit (DB) Pension Scheme

In 2022, ostensibly, seeking inspiration seeking inspiration from the pension liability management reforms introduced by the government of KP, with the support of World Bank, the Government of Punjab, too introduce the parametric reforms in DBPS. Appreciating the evidence made available by the data analytics, the parametric reforms in DBPS try to address the voluntary early retirements after the putting the requisite length of service (called the qualifying service).

In DB, the following reforms are being introduced:

a) The proportion of voluntary early retirements has seen a significant increase in recent years, accounting for 64% of total retirements in the year ending June 30th, 2020, and 63% in the year ending June 30th, 2019. The long-term consequence of this trend is a higher number of pensioners and increased monthly recurring pension expenditure. Now amendments have been approved by the Cabinet to notify a minimum retirement age of 55 years, contingent upon completing 25 years of service whichever is later. The Government of Punjab expects an annual deferment (not savings) of approximately Rs 15-18 billion in the commutation of pension. It will be available for a period of 3 to 4 years, gradually diminishing thereafter (Finance Department, 2023).

b) The Pensionable Pay equal to Basic Pay. Currently, the pensionary benefits are tied to the last basic pay, although it was initially linked to the average of the last three years' basic pay. However, this was modified in 1986. The government has the option to revert to the previous pension formula, of calculating the pension based on the average of the last three years' basic pay. This adjustment would lead to approximately 5% reduction in pension (Finance Department, 2023).

c) Reduction in commutation rate from 35% to 25%. The commutation of pension is currently set at 35% of the gross pension. Previously, it was at 50% of the gross pension but was gradually reduced to 35%. By implementing a reduction in the commutation rate, approximately 28% reduction in commutation expenditure was estimated. With this the budget allocation for commutation, which was Rs 65 billion for FY 2020-21 was reduced for Rs 46 billion. However, adjustment also represents a form of deferred expenditure, with the impact being deferred for a significantly staggered period of 12 to 15 years (Finance Department, 2023).

d) Discount factors for early retirement. The government is trying hard to rationalize discount factor in the light of the World Bank proposal as per the following reduction factor:

Table 2. Age at Retirement and Discount Factor.

Age at retirement | 53 | 54 | 55 | 56 | 57 | 58 | 59 | 60 |

Discount factor | 21% | 18% | 16% | 13% | 10% | 7% | 4% | 0% |

e) Indexation of annual pension increases. Over the years, pension and salary increases have been arbitrary in nature. However, international best practices suggest that pensions and salaries should be indexed to inflation. The Consumer Price Index (CPI) can be utilized to determine annual adjustments for pensions and salaries. On average, pension increases have exceeded CPI by 2.9% over the past 11 years. As reported by Government of Punjab 1% decrease in pension reduces accrued pension liability by Rs. 613.707 billion. If the government had allowed annual pension increases equivalent to the weighted average of three years' CPI, it would have reduced accrued pension liability by Rs. 1,780 billion (Finance Department, 2023).

f) Medical Allowance is being received by Pensioners amounting to Rs 19 billion. The budget allocation for "Medical Allowance for Pensioners" linked to their net pay is very generous. Beside that pensioners claim medical reimbursement for indoor treatments and medications for chronic diseases. They can also have other medical treatment from government-run facilities. Government of Punjab's plan to provide 'Sehat Sahulat' health insurance coverage to all citizens, including pensioners making out a case for partially or fully withdrawing the Medical Allowance (Finance Department, 2023).

g) Direct Credit System (DCS) for monthly recurring pension payments has aided in digitizing records and verifying the existence of pensioners, it was a one-time exercise. It will establish a recurring biometric-based verification system that is more reliable than the current practice of pensioners submitting a periodic 'life certificate' These changes will ensure secure efficient verifications for accurate and timely disbursement of pensions with reduced risk of fraudulent pension claims.

3.2.4. Defined Contribution Pension – Parameters and Rates

In the past, employers in the public sector frequently provided their employees with Defined Benefit (DB) pension plans

| [11] | Sweeting, P. (2017). Financial enterprise risk management: Cambridge University Press. |

[11]

. However, the unexpected financial anxiety and encumbrance caused by these schemes on the budget have headed to a shift towards Defined Contribution (DC) schemes as the preferred arrangement

| [10] | Sandberg, J. (2013). (Re-) interpreting fiduciary duty to justify socially responsible investment for pension funds? Corporate Governance: An International Review, 21(5), 436-446. |

[10]

. DC schemes provide employers with the pledge that no unfunded liabilities will arise

| [11] | Sweeting, P. (2017). Financial enterprise risk management: Cambridge University Press. |

[11]

. Nevertheless, this change has a negative impact on employees since the exact value of their accumulated pension assets, and subsequently the level of pension they will receive, remains undetermined until retirement

| [12] | Baggot, D. M., Hensinger, B., Parry, J., Valdes, M. S., & Zaim, S. (2005). The new hire/preceptor experience: cost-benefit analysis of one retention strategy. JONA: The Journal of Nursing Administration, 35(3), 138-145. |

[12]

. Many pension plans give employees a vote in the investments made with their pension funds as a solution to this problem. This gives prospects the ability to customize the investment management to their own risk/reward preferences and to take into account their ethical or religious convictions, such as buying Islamic equity securities.

| [7] | Naqvi, B., Rizvi, S. K. A., & Shahzad, A. (2023). Selection of Retirement Saving Plan for a Private-sector Employee in Pakistan. Asian Journal of Management Cases, 20(1), 23-34. |

[7]

. By incorporating these considerations into the management of their pension assets, employees have more control over their investments and can reflect their personal values. The contribution pension package is proposed for new hires in the service with the provisions of the rules being duly amended and the standard terms and conditions being part of the terms and conditions for appointment to be accepted by the hired entrants in service.

| [13] | Chybalski, F., & Marcinkiewicz, E. (2016). The replacement rate: An imperfect indicator of pension adequacy in cross-country analyses. Social indicators research, 126, 99-117. |

[13]

. This will rule out the possibility of entangling the state machinery in the litigation which is presently a formidable challenge for any modification in the Defined Contribution scheme. Several parameters have been defined in the DC scheme for its successful implementation and operationalization. These are:

1) Pensionable Pay will be equal to Basic Pay and allowances as per additional indexation will not be the part of the payable pension.

2) Contribution Rate will be 22% (12% Government; 10% Employee). This scheme is basically based on the premise that in future pension the employee will be partner with the government in sharing the burden of pension.

3) Funding Strategy Fully funded, 100% deduction and deposit at source both for government and employee.

4) SECP licensed banks and pension managers. The government contribution will simultaneously be deposited with pension fund regulated by SECP with enabling choices to the subscriber of pension to prefer portfolio for seeking better return on investment including option for Sharia compliant instruments.

5) The government will give option to the Employees for investing in different financial institutions and instruments after assessing his/her potential risks– subject to risk limits.

6) For the success of the scheme it is essential that amendment in CSA 1974, along with the enactment of rules governing Defined Contribution (DC) pension.

7) There will be a bar on immediate withdrawals of the deposited amount to ensure that pensionary benefit continue to flow. so Limits to be imposed will be enforced in its later and spirit.

8) It is also proposed that there will be initial role of the PPF in the contribution towards government share but overall it will have a supervisory role in its performance management and regulations. All civil servants are also required to make employee contributions of between 3 and 8 per cent of their basic salary to the GPF according to their basic salary level.

9) This scheme necessitates that income plan be a mandatory part of this scheme.

10) Early Withdrawal for ensuring the full benefits of the scheme the government is envisaging that it will restrict its withdrawals during the service period of the person. This trend is required for discouraging early withdrawals and safeguarding the pensionable amount of the person.

The Defined Contribution rate has Linkages with the Replacement Rates.

Replacement Rate is defined as % of last pensionable pay replaced by first pension (Chybalski & Marcinkiewicz, 2016). Expected Replacement Rates under new DCP scheme are as under;

Table 3. Defined Contribution Pension – Rates.

Cont. Rate | 2% p.a. | 3% p.a. | 4% p.a. |

25 yrs | 30 yrs | 35 yrs | 40 yrs | 25 yrs | 30 yrs | 35 yrs | 40 yrs | 25 yrs | 30 yrs | 35 yrs | 40 yrs |

25% | 34% | 41% | 48% | 54% | 43% | 52% | 63% | 73% | 48% | 61% | 74% | 89% |

30% | 41% | 49% | 57% | 65% | 51% | 63% | 75% | 88% | 58% | 73% | 89% | 107% |

35% | 48% | 57% | 67% | 76% | 60% | 73% | 88% | 103% | 67% | 85% | 104% | 125% |

3.3. Status and Comparison (Secondary Data Analysis)

3.3.1. Pension Expense of Punjab

These facts lead to higher budgetary expenses and material amount of budget has to be allocated for pensioners and employees. The table below shows the budget allocation figures for FY 2022-23. 1.6 million (employees and pensioners) are beneficiaries of Rs.1275 bn.

Table 4. Employees Related Budgetary Allocations.

Expense Item | Budget Allocation 22-23 (Billion) |

Salary | 435 |

Pension | 312 |

Grants to LGs under PFC | 528 |

Total | 1,275 |

This shows that out of total budget of Rs. 3000 bn (Finance Department, GoPb, 2023) over one third is being spent on Salaries and Pension which puts immense pressure on the provincial government.

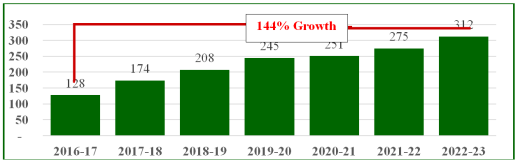

The provincial government’s data reveal that while the Revenue increased 3.1times, Salary expense increased 3.2 times and Pension expense increased 6.5 times. Consequently, the pension expenditures have increased by 144% from Rs. 128 bn to Rs. 312 bn in the last 6 years.

Figure 2. Overall Pension Growth from 2017 to 2023.

3.3.2. Growth of Pension Expenses

It has been noted with concern that not only has the pension bill grown, it has grown faster than the increase in revenue over the last five years leading to a point that pension expense is now 12.4% of total revenue and 18.2% of total current expenses.

Table 5. Annual Pension and Revenue Growth.

Year | Annual Pension (Billion) | General Revenue (Billion) | Pension Expense as % of Revenue | Current Expenditure (Billion) | Pension Expense as % of Current Expenditure |

FY16-17 | 141 | 1,405 | 10.0 | 900 | 15.7 |

FY17-18 | 173 | 1,387 | 12.5 | 961 | 18.0 |

FY18-19 | 205 | 1,426 | 14.4 | 1,129 | 18.2 |

FY19-20 | 229 | 1,478 | 15.5 | 1,200 | 19.1 |

FY20-21 | 236 | 1,665 | 14.1 | 1,258 | 18.7 |

FY21-22 | 253 | 2,194 | 11.5 | 1,380 | 18.3 |

FY22-23 | 312 | 2,521 | 12.4 | 1,712 | 18.2 |

Furthermore, due to the generous pension increases overall annual pension expenditure increased considerably on account of additional allowances and benefits extended by the courts from time to time. This has resulted in increase in annual pension expenditure which is even higher than Consumer Price Index (CPI) which is not desirable by any means.

Table 6. Annual Pension Expenditure Increase.

Years (2011-2022) | Annual Pension Expenditure | CPI (YoY) % | Pension Increase % |

Average Annual Growth | 17.8% | 7.3% | 8.9% |

3.3.3. Reasons for Steep Rise in Pension Expense

At least 7 reasons can be attributed to the steep rise in pension expenditure in the last decade:

a) Regularization of contractual/ temporary employees by various political governments and enactment of Punjab Regularization Act of 2018 paved the way for regularization of thousands of contract employees inducted after 2004 led to steep rise in pension expense.

b) Liberal increase in pension by political governments without indexing to inflation or increase in salary.

c) Favorable Reduction factor for early retirees led many employees to opt for early retirement. Percentage of early retirees rose to 63% in 2019.

d) Average Pension has increased over the years beyond average pay liberal increase in pension by political governments.

e) Increase in pension family hierarchy by the courts added up to 42 years to pension period after superannuation.

f) Post facto adhoc increase in pensions after retirement by liberal interpretation by the courts.

g) Indexation of pension has been pegged to last pay drawn instead of average pay of last three years has increased.

4. Analysis

4.1. SWOT Analysis of Punjab Pension Fund

The SWOT Analysis of the Punjab pension fund reveals that it has institutionalized structures and expertise to manage reserve fund but not fully operationalized to optimum capacity. Professional enrichment of 16 years’ area expertise is available to it for large scale market interventions in the funding of pension liability if made available by the government. The legal mandate is broad enough to enable the fund to resort to capital gains as provisions of PPF rules 2009 supplement PPF for an elaborate framework. PPF is not in control of macro-level deviations. The pension liability profiling is based on specific assumption that employee hiring by Government of Punjab will not exceed 10000/annum whereas currently government is hiring 25000/annum. PPF has the opportunity to achieve confidence of contributors by extending them options of lucrative returns through Pension Voucher schemes (PVS) and minimizing the risk of government. Still PPF cannot rule out collapse of financial markets in the event default against sovereign debt obligation of the country. The case laws holding the field also enable the pensioners to resort to judicial review and favorable ruling by the superior judiciary are beyond the control of PPF.

Table 7. SWOT Analysis.

Strengths | Weaknesses |

1) Legislative backing 2) 16 Years fund management credentials 3) Professionals from private sector | 1) Absence of viable business plan 2) Inadequate contribution from Government 3) Limited portfolio 4) Inadequate preparedness |

1) Mainstream agency for pension liability 2) Pension investment profiling 3) Beneficial choice for PVS | 1) Judicial Interference 2) Lacking populist support 3) Systemic collapse |

Opportunities | Threats |

4.2. Impact Analysis: Anticipated Savings and Cash Flows Pension Plan 2022-25

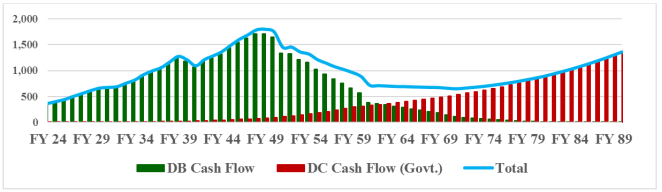

In order to calculate the impact of reforms the RAG approached the Finance department and with the data available attempted to produce a graphic representation of future course provided that Defined Contribution Scheme is initiated immediately:

Figure 3. Convergence of DC and DB and DB Phase Out – Cashflows.

The chart shows that the liability of pension under the existing employees on DB scheme will continue to rise to the year 2049 when the expense will be around Rs.1700 bn but after that the DC scheme will start to takeover and government expenditure will decline. If the Dc Scheme is not introduced the expense on pensions in Punjab will be Rs. 2700 bn by the year 2049 (World Bank, 2019). So, it is the need of the hour that DC Scheme is rolled out immediately.

The above analysis has however been made on the basis of few important assumptions:

a) No hiring under DB scheme beyond 01

st July, 2023. There will no hiring under the present pension regime of direct benefit scheme henceforth. DC scheme is the only way forward if any entity is trying to cut costs or is dealing with financial difficulties

| [14] | Ortiz, I., Duran, F., Urban, S., Wodsak, V., & Yu, Z. (2018). Reversing pension privatization: Rebuilding public pension systems in Eastern European and Latin American countries (2000-18). Available at SSRN 3275228. |

[14]

.

b) Avg. annual hiring of 10,000 employees in the DC scheme. The induction into the government service in Punjab shall be capped at 10,000 per annum only which is currently double that number.

c) Contribution of Government and the employee. The government will be making 12% contribution while employees be making 10% into the pension.

d) The annual increase in salaries per annum is not more than 12% on an average.

4.3. Issues, Challenges & Findings

The Government of Punjab put in the pension management regime in 2007 with the establishment of Punjab Pension Fund and has recently augmented with a number of proposed reforms analyzed in the preceding section. Following are the issues and challenges in implementing the reforms proposed by the Government of Punjab:

4.3.1. Legal Challenges

1) The current regime of pension was inherited from British India and it has been gradually developed over time with a number of legal interventions as discussed before however, the Courts has liberally interpreted the law paving the way for more liberalization in the pension increments. Few examples of challenges posed by judicial interventions are as follows:

a) In 2015 SCMR 1472 the Supreme Court of Pakistan ruled that “the right to pension is conferred by law and could not be abridged or arbitrarily reduced except in accordance with law.

b) In 2007 SCMR 886 the Supreme Court of Pakistan held that no action could ever be taken that could adversely affect terms and conditions of the retirement benefits such as pension, the gratuity or provident fund etc.

c) In a recent case where the Finance Department was asked to review the question as to whether an unmarried daughter can draw family pension of both her parents simultaneously, the Supreme Court ruled that Finance department had no authority under the law to clarify, interpret, abridge or extend the right of pension.

2) The necessary amendments to the effect of parametric amendment in DBS and rolling out DCP scheme on the lines of KP model have to be introduced to roll out both schemes. Changes in the Act would require consent from the upcoming assembly.

3) Similarly, specific rules for enabling Defined Contribution Pension Scheme have to be approved. Currently the draft Rules have been sent by Finance Department to the Regulation Wing S&GAD for vetting and approval.

4) PPF Act and Rules need to be more responsive to allow diversified investment portfolio and incorporate long term investment plans. Legal fencing for PPF to secure the fund from interference or utilization in any government project.

5) Agreements with SECP regulated Fund Managers: Agreements with SECP regulated pension fund managers to increase the return on investment for the pensioners.

4.3.2. Political Challenges

a) Pension reforms carry a lot of political leverage. Over the year’s political governments have increased the pension benefits liberally to appease its political vote bank.

b) Despite rising replacement rate, the pension has remained out of the ambit of taxation due to political and social considerations.

c) The assumption of catering for the job provisions into the public sector only vis a vis shrinking private sector capacity in this regard has compelled the political elite to tilt towards increasing pensions.

d) Despite liberal interpretation by the courts the political governments also did not show willingness to draft any legislation for pension management.

e) In 2004 when induction began in Punjab on contract basis aiming at reducing pension liability by 2038, yet successive political governments allowed regularization of all contractual employees.

f) Lastly enactment of Punjab Regularization Act 2018 has virtually created a hurdle against curbing the pension burden over time.

4.3.3. Economic Challenges

1) Punjab Pension Fund:

a) Inadequate funding of Punjab Pension Fund: The funding for PPF is far below the international standard. 80% of accrued liability should be available to a pension fund however the current funding stands at only 1%.

b) Sharing profits with Provincial Consolidated Fund: There is absence of a comprehensive sharing plan for profits earned with the Government of Punjab towards discharge of pension liabilities.

c) Lopsided Portfolio management: The fund has maintained a very risk averse and limited portfolio thereby not earned profits as compared to other private funds.

2) Defined Benefit Scheme

a) Pensioners are enjoying double benefits as early retirees having demand in the market get rehired and take salary and pension. Similarly, in some cases beneficiaries enjoy pension from both parents.

b) Due to absence of proper verification mechanism many ghost pensioners in connivance with bank staff are taking the benefit of pension.

c) The government has failed to implement a reduction factor (4% widely accepted) to discourage early retirees.

4.3.4. Technological Challenges

a) There is lack of data to estimate the exact liability of pension. The actuarial calculations are based on certain assumption that can change and totally change the estimates which can seriously compromise decision making.

b) The globally accepted 3 lock system suggests pegging the calculation of pension increase with CPI, rate of increase in salaries or 2% after adjustment of CPI/ inflation.

c) Data cleansing is required along with reconciliation to ensure that data available with all stakeholders such as AG, PPF and Finance Department is the same for uniformity of planning and decision making.

4.3.5. Social Challenges

a) Pension has always been regarded in society as a tool of welfare and benevolence that creates social pressure against any decision to rationalize pension schemes.

b) Like society, media also gives negative projection to any reform initiative in the pension management.

c) Resistance is faced against DC Schemes as they promote investment in private funds which render more risk towards the employee.

d) Society is averse to any change especially in case of a reform initiatives that involves pensioners.

4.4. Global Best Practices

Before suggesting recommendations and action plan, it is imperative to study a few global best practices and examples from the private sector. A brief overview of comparison of employee / employer share towards pension in various countries is as under:

Table 8. International Pension System.

Country | Overall | Employee Share | Employer Share |

India | 24% | 10% | 14% |

Kenya | 22.5% | 7.5% | 15% |

Malaysia | 21%-22% | 9% | 12%-13% |

Nigeria | 18% | 8% | 10% |

Chile | Increased employee salary by 18%-10% attributed to pension- 5% for Health Insurance and 3% for Life Insurance. This not only reduced the government burden but also helped built pension and insurance markets. |

This research analyzed of pension regimes of India, Kenya, Nigeria, and Malaysia with a view to draw pertinent lessons to tailor an alternate pension model for Punjab. The case of India and Chile are going to be discussed in detail:

India replaced its traditional Defined Benefit Scheme to Contributory Scheme National Pension Scheme in 2004. It established the Pension Fund Regulation and Development Authority (PFRDA) with technical assistance from the Asian Development Bank. The initial contribution was 10% each from the employee and the government which was enhanced to 14% in 2019. This scheme was extended to corporate entities as well as 400 million informally employed workforces. The returns are totally market linked. The employee can encash up to 60% on retirement and 40% is used to acquire an annuity for monthly income (Asian Development Bank, 2015).

Chile revolutionized its pension system in 1981 popularly known as the “Mercedes Benz” model. The pension was abolished. Salaries were raised by 18%. Out of this 10% was contributed towards pension through a private fund from the market, 5% was contributed towards health insurance and remaining 3 % for life insurance. This not only reduced the burden on the government but also revolutionized health and insurance markets in the country. All workers became investors and capitalists. By the age of superannuation, the most valuable asset of the people of Chile was not a house or a car but the amount of savings in the pension fund. This gave them freedom to invest in the best possible fund making the market more and more competitive. It also gave them the liberty to decide their own retirement age depending on the amount of annuity they could get for monthly income. The system did suffer in the midst of COVID-19, and the government is thinking of reforming the system to help people unable to achieve minimum wage from annuities due to poor economic conditions in the last couple of years. The Chilean model has been replicated in many countries with modifications.

4.5. Comparison with Private Sector

The RAG selected two companies for comparison. Coca Cola Export Corporation which is a private limited company and Fauji Foods Limited which is a Public Limited Company:

Table 9.

Comparison. Comparison. Comparison. Coca Cola Export Corporation | Fauji Foods Limited |

1) Age must be 45 years and employee should have at least served 15 years for qualifying for retirement benefits. 2) 6.5% contribution in fund of choice by the employer based on actuarial calculations. 3) Contribution by employer is part of total benefits of employee. 4) Encashment either lumpsum or monthly over 5 years 5) (Source: CFO Coca Cola Export Corp.) | 1) No Pension 2) Only Gratuity & Provident Fund 3) Gratuity equal to one basic last drawn salary subject to a maximum of 20 basic salaries 4) Provident Fund is contributory and compulsory with contribution of 10% by employee and employer. 5) Lumpsum encashment at separation 6) (Source: GM Fauji Foods Limited) |

Comparison with Khyber Pakhtunkhwa (KPK)

KPK became the first province to roll out the contribution scheme in June 2022 (Sustainable Development Policy Institute, 2022) after realizing that in 2027 their salary and pension expense will surpass their revenue receipts.

Table 10. Provincial Pension Comparison.

Key Area | KPK | Punjab |

Total Pensioners | 167,809 | 541,613 |

Total Expenditure | 69.94 (B) | 312(B) |

Accrued liability | 3000 (B) | 6500 (B) |

CAGR | 17.79% | 19.37% |

Pension as % of GRR | 8% | 12% |

Pension Fund | 60(B) | 105(B) |

Their accrual liabilities stood at Rs. 3000 bn while their pension fund had only Rs. 50 bn. They pursued amendments in the SECP’s Voluntary Pension System (VPS) Rules 2005 to leverage the existing pension model and notified the Provident Fund Rules 2022 to govern its new pension scheme. Necessary amendments have also been made to the Khyber Pakhtunkhwa Civil Servants Rules 1973 in Section 19 that governs pension and gratuity. The minimum retirement age has been fixed at 55 years which is estimated to save Rs. 12 bn. The beneficiaries of pensioners have been reduced to direct dependents and parents only and one pension can be received by dependents. The Defined Contribution Pension Scheme became applicable to all employees joining after June 2022 and 9000 new entrants have been enrolled in this scheme. The initial impact assessment suggests that through this scheme the province will save Rs. 700 bn by 2050. The case of KP is an example for other provinces to follow.

5. Conclusion

Pension liability has escalated beyond sustainability due to frequent regularization of contractual employees and liberal increase in pensions by political governments treating pension as a form of social protection without considering its economic viability. Moreover, absence of Punjab Pension Act has led to unfavorable interpretations by the courts. The staggering pension bill thus forced the Government of Punjab to overhaul the pension management system, however, previous attempts such as creation of Punjab Pension Fund has not worked. With each passing day, lack of political will, conflict of interest, and rising future pension liabilities are making reforms increasingly challenging. It is now imperative that the pension scheme is transformed immediately through short-term and long-term measures.

6. Way Forward

The research underscores the need for a three-pronged strategy to effectively manage present and future pension liabilities. The first component is strengthening the Punjab Pension Fund (PPF). This involves reconstituting the PPF Board to include professionals such as investment bankers, fund managers, financial analysts, and actuaries, ensuring comprehensive representation from all stakeholders. Regular funding is essential for expanding the investment portfolio, and a framework should be established to share the pension burden using profits earned. Quarterly performance evaluations should be conducted, and a research wing should be developed to explore both short-term and long-term investment opportunities and strategies for managing pension liabilities.

The second component focuses on parametric changes to the Defined Benefit (DB) Scheme. Key measures include de-incentivizing early retirements, fully implementing the Direct Credit System (DCS), and introducing a three-lock indexing mechanism for pensionable emoluments. Additionally, a freeze on retrospective increases is recommended to stabilize liabilities. The third component is the adoption of the Defined Contribution (DC) Scheme, which requires a strong legislative framework, including a Pension Act, amendments to the Civil Servant Act of 1974, and rules for implementing the DC Scheme. Monthly contributions should be deducted at the source to eliminate discretion, and the baseline for emoluments must be redefined. SECP-licensed fund managers should be engaged to oversee the implementation of the DC Scheme, with a focus on exploring the best investment options to maximize returns for pensioners. The Punjab Pension Fund (PPF) will play a critical role in managing these investments through stringent performance monitoring. This holistic strategy aims to ensure the sustainability and efficiency of the pension system while addressing liabilities both now and in the future.

The action plan, given below and summarized in a table below that outlines necessary interventions that must be made, the concerned authority who must enact them, the resources that they require, key performance indicators (KPI’s) and goals, broken down over the short, medium, and long-term.

The action plan for implementing the Defined Contribution (DC) pension scheme includes a series of targeted interventions across short, medium, and long-term timeframes. Initially, legal amendments will be introduced to enable the implementation of the DC scheme, involving the Finance Department (FD), Services & General Administration Department (S&GAD), the Law Department, and the Punjab Assembly. This will require the expertise of pension and legal professionals to amend the Pension Act and the Civil Servant Act, 1974, with a target of completion in the short term.

Simultaneously, the formulation of rules for the DC scheme will be undertaken by FD, S&GAD, and the Provincial Cabinet. Governance, pension, and legal experts will ensure that the rules are developed and enforced within the short term. Additionally, FD will engage with the Securities and Exchange Commission of Pakistan (SECP) to upgrade the Voluntary Pension System (VPS) rules of 2005 with the help of financial and HR experts, targeting short-term completion. Further collaboration with SECP-licensed pension fund managers will be formalized through agreements involving FD, S&GAD, and the Law Department, leveraging legal and financial expertise to achieve this milestone in the short term.

To operationalize the DC scheme, S&GAD will upgrade existing HR recruitment instruments and rules to align the terms and conditions for new employees, with a medium-term target. The Punjab Pension Fund (PPF) will also undergo an upgrade to enhance its capacity for regulating and monitoring pension fund managers. This initiative, led by FD and PPF, will involve hiring new HR personnel and allocating Rs. 50 million to implement performance monitoring regulations, aiming for medium-term completion.

To ensure fiscal sustainability, tax incentives for the DC pension scheme will be developed in collaboration with FD, SECP, and the Federal Board of Revenue (FBR). Tax experts will draft, secure approval, and implement these incentives within the medium term. Alongside these efforts, parametric reforms in the existing Defined Benefit (DB) scheme will be implemented through a phased approach. In the short term, reforms will include biometric proof of life, a discount factor for early retirement, and adjustments to pension pay and basic pay. Medium-term reforms will focus on pension indexation and eliminating the medical allowance, while long-term reforms will target a reduction in commutation. These reforms will require cross-departmental coordination, led by FD, S&GAD, and PITB.

Abbreviations

KPK | Khyber-Pakhtunkhwa |

FBR | Federal Board of Revenue |

SECP | Social Exchange Commission of Pakistan |

S&GAD | Services and General Administration Department |

PITB | Punjab Information Technology Board |

Conflicts of Interest

The authors declare conflicts of interest.

References

| [1] |

Abonyi, S. E., & Okoye, U. O. (2023). A comparative assessment of the social and emotional wellbeing of Nigerian retirees under the Defined Benefits and contributory pension system. Indian Journal of Gerontology, 37(1), 126-154.

|

| [2] |

Ahmad, R., Mi, H., Keyao, R., Khan, K., & Navid, K. (2018). Aging and social security system in Pakistan: policy challenges, opportunities, and role of China–Pakistan Economic Corridor (CPEC). Educational gerontology, 44(9), 537-550.

|

| [3] |

Awais, M., Laber, M. F., Rasheed, N., & Khursheed, A. (2016). Impact of financial literacy and investment experience on risk tolerance and investment decisions: Empirical evidence from Pakistan. International Journal of Economics and Financial Issues, 6(1), 73-79.

|

| [4] |

Berstein, S., Fuentes, O., & Villatoro, F. (2013). Default investment strategies in a Defined Contribution pension system: a pension risk model application for the Chilean case. Journal of Pension Economics & Finance, 12(4), 379-414.

|

| [5] |

Ebbinghaus, B. (2015). The privatization and marketization of pensions in Europe: A double transformation facing the crisis. European Policy Analysis, 1(1), 56-73.

|

| [6] |

Josa-Fombellida, R., López-Casado, P., & Navas, J. (2023). A Defined Benefit pension plan model with stochastic salary and heterogeneous discounting. ASTIN Bulletin: The Journal of the IAA, 53(1), 62-83.

|

| [7] |

Naqvi, B., Rizvi, S. K. A., & Shahzad, A. (2023). Selection of Retirement Saving Plan for a Private-sector Employee in Pakistan. Asian Journal of Management Cases, 20(1), 23-34.

|

| [8] |

Naughton, J. P. (2019). Regulatory oversight and trade-offs in earnings management: evidence from pension accounting. Review of Accounting Studies, 24, 456-490.

|

| [9] |

Oladeinde, O. (2021). Political economy of pension reforms in Nigeria: Evaluating the institutional trajectory and roles of international policy advisors. International Journal of Developing and Emerging Economies, 9(1), 48-63.

|

| [10] |

Sandberg, J. (2013). (Re-) interpreting fiduciary duty to justify socially responsible investment for pension funds? Corporate Governance: An International Review, 21(5), 436-446.

|

| [11] |

Sweeting, P. (2017). Financial enterprise risk management: Cambridge University Press.

|

| [12] |

Baggot, D. M., Hensinger, B., Parry, J., Valdes, M. S., & Zaim, S. (2005). The new hire/preceptor experience: cost-benefit analysis of one retention strategy. JONA: The Journal of Nursing Administration, 35(3), 138-145.

|

| [13] |

Chybalski, F., & Marcinkiewicz, E. (2016). The replacement rate: An imperfect indicator of pension adequacy in cross-country analyses. Social indicators research, 126, 99-117.

|

| [14] |

Ortiz, I., Duran, F., Urban, S., Wodsak, V., & Yu, Z. (2018). Reversing pension privatization: Rebuilding public pension systems in Eastern European and Latin American countries (2000-18). Available at SSRN 3275228.

|

| [15] |

Wahab, M., Mufti, O., & Khan, M. A. (2017). The Effects of Population Ageing on the Public Pension System in Pakistan. Abasyn University Journal of Social Sciences, 10(2).

|

Cite This Article

-

-

@article{10.11648/j.jfa.20251301.11,

author = {Aqsa Ghazi and Umar Farooq Salamat},

title = {Effective Management of Provincial Pension Liability},

journal = {Journal of Finance and Accounting},

volume = {13},

number = {1},

pages = {1-13},

doi = {10.11648/j.jfa.20251301.11},

url = {https://doi.org/10.11648/j.jfa.20251301.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.jfa.20251301.11},

abstract = {Pension expenditures have become a critical fiscal challenge for the Government of Punjab, surging to Rs. 312 billion in the fiscal year 2022-23. The accrued pension liability now stands at Rs. 6.5 trillion, significantly constraining the government's capacity for current and development expenditures. This study explores the existing regulatory framework for pension liability management and proposes actionable solutions based on global best practices. Through a comprehensive methodology that includes literature reviews, data analysis, comparative studies of national and international practices, and stakeholder interviews, the research highlights alarming trends: a 300% increase in government revenues over the past decade, contrasted with a staggering 650% rise in pension costs. Key contributors to this fiscal burden include the Defined Benefit pension scheme, regularization of temporary employees, and adverse judicial rulings. To address these challenges, the study recommends transitioning to a contributory pension scheme, reducing commutation rates, aligning pensionable pay with basic pay, indexing pension increases, and leveraging biometric verification systems. Additionally, amendments to the Civil Servants Act and better management of the Punjab Pension Fund are proposed to ensure fiscal sustainability. These measures aim to mitigate the growing financial strain, ensuring long-term stability and efficient pension liability management for the Government of Punjab.},

year = {2025}

}

Copy

|

Copy

|

Download

Download

-

TY - JOUR

T1 - Effective Management of Provincial Pension Liability

AU - Aqsa Ghazi

AU - Umar Farooq Salamat

Y1 - 2025/01/24

PY - 2025

N1 - https://doi.org/10.11648/j.jfa.20251301.11

DO - 10.11648/j.jfa.20251301.11

T2 - Journal of Finance and Accounting

JF - Journal of Finance and Accounting

JO - Journal of Finance and Accounting

SP - 1

EP - 13

PB - Science Publishing Group

SN - 2330-7323

UR - https://doi.org/10.11648/j.jfa.20251301.11

AB - Pension expenditures have become a critical fiscal challenge for the Government of Punjab, surging to Rs. 312 billion in the fiscal year 2022-23. The accrued pension liability now stands at Rs. 6.5 trillion, significantly constraining the government's capacity for current and development expenditures. This study explores the existing regulatory framework for pension liability management and proposes actionable solutions based on global best practices. Through a comprehensive methodology that includes literature reviews, data analysis, comparative studies of national and international practices, and stakeholder interviews, the research highlights alarming trends: a 300% increase in government revenues over the past decade, contrasted with a staggering 650% rise in pension costs. Key contributors to this fiscal burden include the Defined Benefit pension scheme, regularization of temporary employees, and adverse judicial rulings. To address these challenges, the study recommends transitioning to a contributory pension scheme, reducing commutation rates, aligning pensionable pay with basic pay, indexing pension increases, and leveraging biometric verification systems. Additionally, amendments to the Civil Servants Act and better management of the Punjab Pension Fund are proposed to ensure fiscal sustainability. These measures aim to mitigate the growing financial strain, ensuring long-term stability and efficient pension liability management for the Government of Punjab.

VL - 13

IS - 1

ER -

Copy

|

Download