Abstract

The history of modern Chinese insurance is a history of foreign insurance industry to control and monopolize the old Chinese insurance market while the Chinese insurance industry tried to be independent and anti-monopoly. Insurance compradors have played an important role in the Western insurance “Indigenization” process in the 19th century China. Insurance buying is a form of western capital in modern insurance industry, which is born and comes for profit. This paper argues, to expand in Chinese market, Western insurers designed a set of system, based on social networks, incorporating marketing, incentive, and credit guarantee namely the insurance buying system; that is, the insurance comprador system, which has assisted Western insurers in monopolizing the Chinese insurance market and bred a group of parvenu insurance compradors. With the growth of both Western insurers and insurance compradors, their relationship has gradually turned from inter-dependence to independence. On the one hand, when Western insurers came to scale, risk control replaced market expansion as development priority, which necessitated the change from a business model weighing insurance compradors to that weighing professionalization and risk-control; on the other hand, insurance compradors founded Chinese insurance industry with the capital and know-how accumulated in working for Western insurers.

Keywords

Western Insurance Industry, Insurance Comprador, Social Networks, The System of Insurance Comprador, Dialectical Movement Relationship

1. Introduction

Insurance is a special commodity, bearing the function of sharing losses and transferring risks in commercial activities, which is separated from the production process as an independent department, and its necessary premise is the full development of the commodity economy and the high refinement of the social division of labor. In 19th century China, feudalism already had the original form of insurance organization and insurance ideas, but due to the lack of a certain economic and social foundation and commodity economic system, the transformation to modern insurance marked by commercial insurance was not completed. On the contrary, the rapid development of the Western capitalist economy and the expansion of the outside world, the insurance in the form of capitalism began the globalization movement early

, and Modern insurance was first introduced into China during the early nineteenth century

.

The development of Western insurance industry in China can be divided into three stages: (1) The early stage-first half of the 19

th century-saw the arrival of Western insurance in China, with Macau, Hongkong and Guangzhou as centers. In 1805, Guangzhou appeared China's first insurance company, the Canton Insurance Society

| [3] | G. C. Allen. Western Enterprise in Far Eastern economic development, China and Japan [M]. London: Jarrold and Sons Ltd Norwich, 1968. |

[3]

, opening up the prologue to the development of China’s modern insurance industry. In this stage, Western businesses mainly acted as agents for insurance business in a few coastal open port cities. (2) In the middle stage from 1860s to 1937, which saw the development of insurance with Shanghai as center and Tianjin, Hankow and Hongkong as quasi-centers, Western insurance came to gain ascendancy and monopoly in China’s insurance market. By the end of the 19

th century, Western insurance had finished its transformation from Western firms-affiliated agencies to standalone insurance institutions; and at the same time, the insurance business reached inland from port cities. And also, a nationwide insurance network, with British insurers taking the lead, took shape in China. (3) The late stage, from 1940s to 1950s, witnessed the break-off, resumption and retreat of Western insurance businesses. In short, the 19

th century saw a drastic development of Western insurance industry, which has managed to monopolize the Chinese market since its arrival only a few decades earlier. A combination of favorable timing, environment and network may account for the monopoly. Impotency of the Qing government, privileges granted to Western businesses and the galloping colonial economy provided the favorable timing; social networks of insurance compradors employed by Western insurers provided the favorable environment and network.

The definition of comprador varies in the scholarship.

This article adopts the viewpoint of “intermediary agent”, proceeding on the basis of regarding comprador as vocation. The term of comprador in the Ming dynasty refers to official agents responsible for purchasing goods for the imperial court; and under the Guangzhou business system in the Qing Dynasty, which boiled down to a privileged procurement system, compradors were responsible for purchasing Chinese goods for Western businessmen. after the First Opium War (1839–1842), the Qing government recognized free trade and abolished privileges granted to businessmen, so the scope extended of Westerners’ exploitation of compradors, whose population and functions have since dramatically changed. The appellations of comprador in Chinese also abound, for example, “Kang Badu”, “Kang Baidu” with different Chinese characters, “Hua Zhangfang”, “Ban Fang”, “Ling Shide”, “Shang Huo”, to name a few. Statistics indicates that the population of compradors stood at 250 in 1854, which rose to 700 in 1870 and over 10000 by the end of the 19

th century. According to the nature and business of companies which compradors work for, Sha Weikai divided comprador into 4 categories: banking comprador, shipping company comprador, insurance comprador and ordinary shop comprador. Insurance comprador stands between Western insurers and the Chinese people to facilitate the business of insurance, that is, introducing the insured to insurers and handling all the formalities involved

| [4] | Sha Weikai. China's Comprador System [M]. Beijing: The Commercial Press,1934. |

[4]

. In the context of this article, insurance compradors exclusively refer to compradors working for Western insurance industry, which includes Western insurance companies as well as insurance agencies.

Four phases can be divided from the rise to decline of insurance compradors in China. The first is the phase of initial involvement (from early- to mid-19th century). In the early stage of its development, Western insurance was mainly brokered by Western firms, and so compradors in Western firms double as insurance compradors. Tang Tingshu, Xu Run and Zheng Guanzheng, for example, were well-known compradors in the 1850s and 1860s. In their days as comprador, respectively, for Jardine Matheson, Dent & Co., and Taikoo, handling of insurance business was part of their work portfolio. The second is the phase of growth (from mid-19th century to 1875), when Western insurance industry began to stand on its own. Professional insurance companies were founded in China on a large scale; and at the same time, some big Western firms regarded insurance as their major business, and even set up insurance companies. In brief, both Western firms and insurance companies began to employ full-time insurance compradors to cater to the development of insurance business. In the 1860s, Jardine Matheson set up a position called comprador assistant to take care of insurance business. At this stage, compradors have gained experience in running insurance business and raised capital from bonuses, laying foundation for their dependence from Western insurance industry. The third is the phase of maturity, where some insurance compradors were strong enough to alienate from Western insurance industry. It was marked with the establishment of Insurance Merchants in 1875, under the efforts of Tang Tingshu, Xu Run and other compradors. At this stage, some insurance compradors were strong enough to set up insurance companies, yet at the same time, their social networks were of great value to the development of Western insurance industry. In 1891, for example, the restructured Yangtze Insurance Association, ltd., utilizing social networks to develop agents, quickly realized positive growth in premiums and profits from a negative one (see below detailed analysis). The fourth is the phase of decline (the early-20th century to 1943), with the ascendancy and monopoly of Western insurance industry established by the end of 19th century, insurance compradors were of lesser value to Western insurers. Since the beginning of the 20th century, some Western insurers no longer employed compradors; and the status of compradors dropped significantly even in those who continued to employ. By 1943, compradors no longer existed along with the abolition of “Treaty System”, nor did insurance compradors.

2. Historical Roots of Insurance Compradors

Insurance comprador, as a representation form of Western capital’s involvement in China’s modern insurance industry, was born of and came for profits. When Western insurers arrived in China, their intended subjects of service were Western firms. By the mid-19th century, China has been forced to open up wider with the signing of unequal treaties, leading to the rapid development of Western trade and steamship industry; with mounting demand of the market for insurance coverage, the enormous potential of China’s insurance market has gradually emerged. And yet, the chaos in financial market, shortage of insurance professionals, underdevelopment of transportation, language barriers and other factors impeded Western insurers in expanding the market, and therefore they needed compradors in this regard. In the late-Qing society, a degenerate tendency was all over China to work for and seek the patronage of Westerners; the Qing government was corrupt and incompetent, leading to the loss of sovereignty, and in the end of 19th century it even announced the humiliating policy of “Mobilizing the resources of China to the satisfaction of other countries”. The nation was so weak that Chinese businessmen, with a view to protect their interests, sought protection from Western forces by working for them as compradors; and therefore, Chinese businessmen responded positively and actively to Western insurers’ need for insurance compradors, providing Western insurance industry with many Chinese insurance practitioners, who had broad and deep social networks in China.

2.1. The Arrival of Western Insurance Industry Led in the Modern Insurance Industry in China

No risk, no insurance. Insurance-as a safeguard mechanism for business-came to China alongside the Western trade. Following the completion of industrial revolution, the Great Britain began to expand abroad. When British businesses came to China, insurance came as well to answer the call for need of their economic activity and trade development.

Since the early 19

th century, the Great Britain with its success of industrial revolution has turned into the biggest power of industry and trade. From the end of the 18

th century to the beginning 19

th century, the gradual collapse of British East India Company’s monopoly over trade in the East prompted Western businessmen’s competition in setting up firms in China; such prestigious firms as English Dent & Co., American Russell & Co. were set up during this period. By 1837, there were 156 Western firms in Guangzhou. Following the signing of

Treaty of Nanking, Western-financed firms came to Shanghai in succession. According to statistics, the number of Western firms in Shanghai was 11, which increased to 24 in 1847 and to 62 in 1859; and the period between 1876 and 1884 saw the increase from 160 to 245 in Shanghai

| [5] | Wang Chuifang. History of the West—Shanghai: 1843—1956 [M]. Shanghai: Shanghai Social Sciences Press, 2007. |

[5]

.

The increase of Western firms led to a growing demand for insurance. In 1801, a group of Western merchants in Guangzhou established a temporary insurance association; in 1805, W.S Davidson, Division manager of Opium of East India Company, initiated Canton Insurance Society in Guangzhou, which was operated, in turn, by Dent & Co. and Magniac & Co. (predecessor to Jardine Matheson)

. The birth of Canton Insurance Society has opened up the prologue to the modern insurance industry in China, and in the one and half centuries since, Western insurance industry has gained ascendancy and monopoly in China’s insurance market. Statistics indicate that in 1838 55 Western firms in Guangzhou brokered the business of insurance for 15 Western insurers

| [7] | Nie Baozhang. Materials on the History of Shipping in Modern China [M]. Shanghai: Shanghai People Publishing House, 1983. |

[7]

. By the 1950s and 1960s, some great Western firms have struggled to set up insurance divisions, for example, Jardine Matheson, Dent & Co., Augustine Heard & Co. and Russell & Co. have set up insurance divisions to provide insurance services; some Western firms even invested in opening new insurance companies.

“The Chinese people increasingly appreciated the benefits of marine insurance, which they use more widely with each passing day. Increasing number of Chinese people demanded of Western ships security guarantee for their goods. Was insurance available? Chinese shippers were quick enough to make the inquiry. Therefore, offering of insurance coverage for one third of the world population in their trade was put on the table for newly-coming adventurers”

| [8] | Yen-P'Ing Hao. The Comprador in Nineteenth Century China: Bridge between East and West[M].Shanghai: Shanghai Academy of Social Sciences Edition, 1989. |

[8]

. While Western insurers turned their eyes to the Chinese market, the importance of insurance got recognized in China, and at the same time the Chinese businessmen’s awareness of risk safeguard was also sprouting. In 1883, Zheng Guanying left Shanghai Mechanical Textile Bureau; and the successive Director-General Yang Zonglian stopped purchasing insurance for the bureau as he thought it was a false spending. In October of 1983, a big fire burnt the estate to ashes, causing a damage of over 700,000

liang (unit of measurement, 1

liang equals 50 grams)

| [9] | Xu Run. Shanghai Miscellaneous[M]. Zhuhai: Zhuhai Publishing House, 2006. |

[9]

. Thus, Chinese businessmen remarked that “since the insurers are set up with the opening up, we businessmen have been pleased to purchase insurance so that we may save hard-earned money in case of losses when shipping goods abroad”.

2.2. Western Insurance Industry Fell Short of Professionals to Run Insurance in China

Western insurance industry needed personnel to develop its business in China, and yet, in the 19

th century, there was a shortage of Western professionals in the industry, and even a small population of Westerners in China. Xu Run notes that “when Shanghai opened up for trade in 1843, there were only 462 Westerners in mainland China, of whom were few women and children. …… in the 24

th year of Period of Emperor

Dao Guang (year of 1844), the population increased to 700; in around July and August of the 26

th year (year of 1846), there were 108 Westerners in Shanghai, 13 of whom had dependents […] in the 29

th year (year of 1850), the population amounted to 1007, with 153 in Shanghai, 298 in Guangdong. In the 4

th year of the Period of Emperor

Xian Feng (year of 1855), there were 243 Western businessmen in Shanghai. in the 8

th year of the Period of Emperor

Tong Zhi (year of 1870), the total population of Westerners in China stood at 1666”

| [10] | Dai Jianbin. History of Chinese Monetary Culture [M]. Shandong: Shandong Pictorial Publishing House, 2011. |

[10]

. Such a small number of Westerners in China fail to answer the call of insurance industry for personnel, and the Western businessmen, therefore, was forced to resort to other means, that is, employing Chinese people of good credibility as insurance compradors.

2.3. Fragmented Monetary System and Cumbersome Bookkeeping Methods Led Western Insurers to Turn to Compradors

In late Qing China, in addition to the currency in circulation like silver ingot, specie, copper coin, Western silver coin, paper vouchers issued by

Hubu (Ministry of Revenue), Guan Yinhao (financial institutions set up by the Qing government), money houses and exchange shops also function as medium of exchange; and notes issued by Western and Chinese banks went into circulation. There, it has never formed a fixed rate of exchange between the banknote and copper coin in circulation, and silver coin and ingot. Moreover, “

liang”, the main measurement unit of weight, was not identical, varying with venue and business; there were, for example, Shizu silver and Songjiang silver in Beijing, Huabao silver, Baibao silver and Lao Yanke silver in Tianjin, Wei Zhoubao in Zhang Jiakou, and Gongyi Zuwen silver in Zhenjiang, Jiangsu, etc. At the same time, silver was to be measured by scale, and yet there were approximately a thousand of measures for weighing silver; and therefore, the values of the same silver may differ greatly on different measures, which asks for conversion of the values

| [11] | Xu Dixin et. A History of the Development of Capitalism in China: Volume 2 [M]. Beijing: People's Publishing House, 2005. |

[11]

. After the Sino-Japanese War of 1894-1895, dozens of Western silver dollars were in circulation in China. Statistics indicates that Western silver coins in circulation as well as in storage in China amounted to 1.1 billion of pieces in 1911. In face of a monetary system of such complexity, Western businessmen admitted that “I had no choice but to resort to compradors to handle business in China”

| [4] | Sha Weikai. China's Comprador System [M]. Beijing: The Commercial Press,1934. |

[4]

. By the same token, Western insurance businessmen had to rely on compradors to deal with bookkeeping. Graham, Shanghai Branch Head of Sun Fire Insurance Office’London, once commented that “Europeans will never understand the bookkeeping system of the Chinese”.

2.4. Such Factors as Language Barriers and Customs Necessitated Western Insurance Industry Relying on Compradors

In Chinese economic life of the 19th century, business networks were still embedded in other social networks, a fact that attached a high economic value to social networks. When Western merchants brought insurance industry to China, they resorted, in the absence of market mechanism and a sound legal system, to insurance compradors with powerful social networks to boost expansion in China’s insurance market.

First of all, China has a lowly commercialized society in the 19th century; and guilds, based on kinship and regional origins, monopolized most industries. Once a stabilizer for China’s feudal economy, the system of guilds and townsmen associations now would become a stumbling block to Western insurance industry’s expansion in Chinese market. In particular, townsmen associations, relying on kinship and regional ties, serve the feudal economy along with guilds, as supplement to the underdeveloped market. They safeguarded the normal operation of the feudal economy, and yet the self-protection led to the seclusion of the industry and of the market. On the other, when the Western insurance industry came to China for business opportunities, handling the relationship with guilds, which were at the helm of industries, was a major work of Western insurers. Not uncoincidentally, Chinese businessmen with favorable resources and networks serve as compradors, introducing the insurance industry to China’s enclosed industries. An extensive social network defined the striking feature of insurance compradors. Building mutual trust with Western businessmen was the prime condition of insurance comprador’s social networks; and the capacity to develop and manage social networks was insurance comprador’s core competitiveness.

Secondly, the sense of security in old China, rooted in social networks, precluded the promotion of insurance. In the 19th century, except for a few open ports, China was a closed society in most areas, where kinship and blood ties were heavily clung to for sense of security, and a word-of-mouth integrity system prevailed valuing kinship and countrymanship, as demonstrated in several old sayings, “raising sons to provide for one’s old age”, “depending on friends when one is away from home”. Lack of insurance awareness and rigid traditional ideas made insurance products unpopular with Chinese people.

In short, “since 1842, when free trade replaced the monopolizing

Gonghang system, Western businessmen have found it tricky to establish direct contact with China. They have been compelled by numerous factors to employ Chinese people to work for them as compradors”. At the time, one Western newspaper commented on the function of compradors that “they can be likened to wheel shaft, which enables the wheel of trade to move forward between Westerners and Chinese people, and under many circumstances, they also can be likened to wheel hub, spoke, wheel rims-indeed a whole wheel, except for the paint of a wheel. And while, Western firms may act as painter, giving compradors a nominal color”

| [9] | Xu Run. Shanghai Miscellaneous[M]. Zhuhai: Zhuhai Publishing House, 2006. |

[9]

. Compradors in Western firms got, directly or indirectly, involved with the business of insurance. Statistics suggest that 88 persons worked as compradors for the 4 big Western firms (Jardine Matheson, Augustine Heard & Co., Dent & Co., Russell & Co.) during the period of 1850s to 1870s, and specifically: 24 for Augustine Heard & Co., 18 for Dent & Co., 15 for Russell & Co., 31 for Jardine Matheson. By the end of the 19

th century, 49 compradors were surely involved in the insurance business; 8 Western insurers, including Yangtze, were known to have employed 13 insurance compradors. From the end of 19

th century to the beginning of 20

th century, 36 Western firms writing marine and fire policies were known to have employed 39 insurance compradors.

Western insurance businesses, at their early development, relied heavily on insurance compradors. At the end of 19th century, Sun Fire Insurance Office’London established its Shanghai branch, operating insurance business directly in China. Graham, Head of the branch, once asserted that “all European companies in Shanghai wholly count on their compradors to deal with the Chinese people”.

3. Insurance Comprador System

Comprador insurance system is an economic system gradually built for the service of Western insurance industry. It incorporates a set of marketing, incentive and credit guarantee systems, based on social networks.

3.1. Duties of Insurance Compradors

The most important duties of insurance compradors include: (1) selling insurance products; and (2) developing insurance agencies in China. A comprador, once picked by a Western insurer, tends to have to go through a probation, “which generally lasts three months, before his competency warrants the insurer continuing to employ him”. Being competent or not depends on his performance of the duties, which are stipulated by Western insurers. Take the stipulations of the Sun Fire Insurance Office’London for example.

Insurance compradors in Shanghai Branch of Sun Fire Insurance Office’London was also the general manager of the branch’s Chinese agencies, and his duties were set as follows: (1) as comprador, to bring in business for the company directly through his sway, or indirectly through brokers. And specifically, to meet clients and brokers; to provide guarantee for premiums; to collect premiums; to pay local bills; and to keep a complete ledger in Chinese. (2) as general manager of Chinese agencies, to visit cities and towns where the company sees potential. And specifically, to visit local officials; to pick and train local agents; to confirm whether appropriate guarantee is in place; to maintain communication with local agents; to arrange for monthly remittance of premiums to the company by local agents.

Western insurers have developed a set of marketing system, based on social networks, by means of selecting compradors and defining their duties. They selected compradors, who are trustworthy and have certain social networks, and through the latter wrote insurance policies, developed Chinese agents, so as to open up insurance markets in the rest of China and to make more profits.

3.2. Credit Guarantee System as a Way to Constrain Insurance Compradors

In consideration of China’s special conditions, Western businessmen would use the power of social networks to guarantee the credit of compradors. In order to maintain his social networks built on “word-of-mouth”, insurance comprador would attach great importance to personal credit lest resources contained in the networks get lost. This offers Western businessmen a primary guarantee for the comprador’s credit; in some cases, Western insurers hired compradors just in light of the latter’s profound social networks. Tao tingxuan, insurance comprador with Java Sea & Fire Insurance Co. of Batavia was appointed to the post exempt of paying otherwise required deposits, as his father Tao Lanquan held a senior position in the Bank of China and some sway in the financial community.

In addition to social networks, western Western businessmen also seek guarantee from launching the deposit system, wherein compradors are required to pay deposits as a collateral to constrain their behavior. The system was widely used in Western firms in China. The amount of deposits varied with the industry, size of business, and the comprador’s duties, with a high up to tens of thousands and over 10 thousand even at its low. The Comprador Agreement, for example, entered into between the Sun Fire Insurance Office’London and its comprador Zun Tiefu, stipulates “to pay a deposit of 3000 liang to its [Sun Fire Insurance Office’London] branch”. Deposits paid by compradors helps spread asset risks for the Western insurance industry, and also provides a source of capital for the Western insurance companies.

3.3. Income Distribution System of Insurance Compradors

Insurance comprador’s income is mainly composed of monthly salary, commission, Chinese agent commission, proceeds from investment on premiums, commission difference, and honorarium from the insured. The income takes on two features: first, the fixed income (including monthly salary and honorarium from the insured) accounts for a small portion, while the flexible income (including commission, Chinese agent commission, proceeds from investment on premiums, and commission difference) is the major source of income, a fact that makes income gap formidable among compradors; second, agent commission, distribution of which lies in the hands of insurance compradors, used to constitute the most important source of income for compradors; and yet it varies with time and individuals. In all, western insurers have designed a set of income-based incentive mechanism to mobilize compradors’ initiative, so as to improve their performance and expand the market.

Compradors as a whole has speedily become rich following the freeing of trade between China and the West; and the American scholar Yen-ping Hao called them “upstart” of modern China. By working as compradors and running business, they have earned as much as 530,000,000

liang within 54 years from 1842 to 1896

| [9] | Xu Run. Shanghai Miscellaneous[M]. Zhuhai: Zhuhai Publishing House, 2006. |

[9]

, an equivalent to 10 years’ revenue of the Qing government. The swift rise of compradors’ wealth caused a social sensation at the time, as Wang Tao commented “[they] can make a lot of money in an instant with just bare hands”. The sources and sum of compradors’ income differ through different periods and industries. Some scholars have statistically analyzed the compradors’ income from 1840 to 1894 in all industries and concluded that they have made 500 million

liang from,

exclusive of proceeds from investment, working as compradors, which was subdivided into 88 million from salary, 184 million from general trade and other type of earnings, 84 million from price difference of export commodities, 97 million from opium trade, 19 million working as compradors for Western plants, 5 million from Western borrowing, 6 million from working as compradors for banks, 10 million from working as compradors in shipping and insurance industries

| [12] | Ma Xueqiang et. Between China and the West: The Social Life of The Compradors in Modern Shanghai [M]. Shanghai: Shanghai Dictionary Publishing House, 2009. |

[12]

.

How did compradors manage to make such a formidable wealth as suggested in the above-mentioned statistics? Although compradors’ income varies, depending on their “competency”, employer insurers and the timing of working as compradors, it mainly comes from the following sources: (1) monthly salary. Monthly salary of each comprador may differ a bit with different companies, yet the difference is small. For example, the monthly salary of insurance compradors in Shanghai generally ranges “between 100 and 300

liang”

| [4] | Sha Weikai. China's Comprador System [M]. Beijing: The Commercial Press,1934. |

[4]

, and the salary of a comprador working for the Sun Fire Insurance Office’London stood at 200

liang per month. (2) Honorarium from the policyholder. “The insurer will compensate the policyholder as per insurance policies in the event of disaster, and the comprador will receive as honorarium 5% of the compensation from the policyholder, and meanwhile the latter will express his acknowledgements to the comprador on newspapers”

. (3) Commission. Western insurance companies believes that “an employee‘s income shall not be limited to payment on his position, but also linked to his performance on the company’s business”, and so the commission rate for insurance compradors varied, which generally ranged between 5% and 10% of the net premiums. (4) agent commission. Lowering agent commission rate was also one of important means of competition among Western insurers. For the business in Europe, the agent commission rate was agreed at 15% and rigidly followed by insurers. But for the business in China, there lacks of a fixed rate, which was very high at times of fierce competition. The agent commission rate was defined by the Western insurers, so volatile as ranging between 20% and 60%; and the commission was administered by compradors. The Sun Fire Insurance Office’London, for example, stipulated that 25% of the premiums be deducted as commission, kickback or brokerage for compradors and left at the disposal of compradors. At times of fierce competition, insurers may promise a 60% commission rate. In an agreement, for example, between the Sun Fire Insurance Office’London and its comprador Ms. Zun, the insurer agreed to “deduct 60% of its premiums on Chinese business as brokerage and reward for the comprador”.

In addition to the above 4 sources of income, insurance comprador can also make money from commission difference, proceeds from investment on premiums, as well as office expense. It can be told from the above analysis that the difference among insurance compradors’ income was mainly determined by commission rate and agent commission rate, and in particular the latter fluctuated a lot. In the early stage of development, Western insurers have developed a large number of agencies; and insurance compradors controlled the distribution of Chinese agent commission, which was an important reason why they got rich rapidly.

4. Dialectical Relationship between Insurance Compradors and Western Insurers

Historical needs spawned the insurance comprador system, which has been in constant fluctuation with the change of relationship between Western insurers and insurance compradors, that is, in general from inter-dependence to independence.

4.1. Watershed: Insurance Compradors Bought Shares of Western Insurance Companies

With the deepening of association between Western insurers and insurance compradors, their relationship has turned from engagement, with compradors working for the insurers, characterizing the initial stage of the Western insurance business’ development, to partnership, with compradors investing in insurers while working for them. Insurance compradors, with the accumulated wealth from working as compradors and under the encouragement by Western insurers, actively invest in insurance companies. The act of investing has set a new course for the relationship between insurance compradors and Western insurance businesses. On the one hand, the act has formed between them a closer community of shared interests. Compradors would accumulate more wealth from the dividends and security benefits; the investment by compradors would provide the Western insurer business another source of capital as well as more business. On the other, the act has paved the way for the future “separation” between the Western insurance business and insurance compradors. With the investment, the status of compradors was also changed from insurer’s employee into its shareholder, who would get involved in the management of the business’ operation. The change of status would facilitate compradors’ involvement in establishing Chinese national insurance industry, in terms of capital and managerial expertise; the establishment of insurance sales networks has also lessened the reliance on compradors by Western insurance companies.

Following the entry or set-up of Western firms into China, Chinese merchants and Chinese nationals invest in Western firms by means of purchasing their stocks. From 1860s onwards, some Chinese merchants have bought significant shares of enterprises in treaty ports, like Western ships, banks, insurance, reeling silk, and power.

It has been long since Chinese businessmen bought stocks of Western insurers. “As early as in 1835, Union Insurance Society Co., which was set up by Dent & Co. in Macau, saw the Chinese merchants’ investing in its shares. Some recordings even noted that the company was co-founded by Chinese businessmen in the capital of Guangdong Province with their Western counterparts”

| [14] | Zhang Kaiyuan et. al. History of the Revolution of 1911 [M]. Beijing: Oriental Press, 2010. |

[14]

. After the Opium War, Chinese nationals holding shares of Western insurers became a commonplace with the increase of Western insurers in China. In 1863 North China Insurance Company was founded by five British companies, and in its 1865 prospectus it expressly stated that “for Chinese nationals who would like to purchase stocks, in big or small numbers, it can be negotiated through letters or in person”

| [8] | Yen-P'Ing Hao. The Comprador in Nineteenth Century China: Bridge between East and West[M].Shanghai: Shanghai Academy of Social Sciences Edition, 1989. |

[8]

. The Yangtze Insurance Association has seen the involvement of Chinese capital since its foundation in 1862 in Shanghai, and after its expansion in 1878, the population of its Chinese shareholder grew to such an extent that Chinese shareholders’ names were often seen on its shareholder representative list. Besides, China Fire Insurance Co., China Trader’s Insurance Co., Hong Kong Fire Insurance Co., China & Japan Marine Insurance Co., and among others, “have seen the involvement of Chinese capital upon their foundation or during their subsequent restructuring”

| [14] | Zhang Kaiyuan et. al. History of the Revolution of 1911 [M]. Beijing: Oriental Press, 2010. |

[14]

. Western insurers’ absorption of capital from Chinese nationals, one the one hand, provided a source of capital; on the other and more importantly, it facilitated their using the social networks of Chinese shareholders to expand insurance business.

Mr. Wang Jingyu once concluded that “among [Chinese] shareholders of Western enterprises … most are compradors”. Of the 47 major Chinese shareholders who have been identified, 28 were compradors of Western firms, accounting for 59. 6%

| [15] | Wang Jingyu. Tang Tingshu Research [M].Beijing: China Social Sciences Press, 1983. |

[15]

. A majority of Chinese nationals buying stocks of Western insurers were also insurance compradors. Tang tingshu in 1863 became a comprador for Jardine Matheson, taking care of all of its business in China, including that of its establishment Canton Insurance Society. In 1867, Tang Tingshu at the age of 35 began to buy stocks of Canton Insurance Society; and in 1868, he marketed shares of Canton Insurance Society and Hong Kong Fire Insurance Co. to Chinese merchants and solicited insurance business

| [16] | Wang Jingyu.The Economic Aggression of Western Capitalism against China in the Nineteenth Century[M].Beijing:People's Publishing House,1983. |

[16]

. When Mr. He Dong in 1882 became a comprador of Canton Insurance Society and Hong Kong Fire Insurance Co. as a result of winning recognition of Jardine Matheson’s manager, Canton Insurance Society happened to go through restructuring, expanding its capital to 2.5 million yuan and absorbing shareholders from the public. “Shares of our company are available for everyone to purchase”. He Dong then seized the opportunity to actively buy the shares, and in 1884 he was among the directors of Canton Insurance Society and representative of its China office. After 1890s, the strength of Chinese shareholders in Canton Insurance Society appeared in Canton Insurance Company. There were, for example, 8 major Chinese shareholders on the name list of representatives attending the 1891 shareholders’ congress, including another comprador of Jardine Matheson Mr. He Gantang who was also He Dong’s brother

| [17] | Yan Pengfei et. History of Insurance in China 1805-1949 [M]. Shanghai: Shanghai Academy of Social Sciences Press, 1989. |

[17]

.

Allowing compradors of competence to buy its stocks is one of Western insurer’s incentive means. Jardine Matheson’s internal communications mentioned several times of selling shares to Tangtingxu as a reward for his remarkable contribution to the company’s business in China. In 1870s, the development of two insurance companies under Jardine Matheson “were in an unsatisfactory state”, and in a bid to draw over Chinese businessmen and compradors, the company believed that “Tang Jingxing [pseudonym of Tang Tingshu] seems to have tried his best to bring in business,…consider allocating part of the profits he’s made to him and other Chinese businessmen with influence”

| [16] | Wang Jingyu.The Economic Aggression of Western Capitalism against China in the Nineteenth Century[M].Beijing:People's Publishing House,1983. |

[16]

. As Chinese merchants were so enthusiastic with buying its shares, the North China Insurance Company promulgated a rule, linking the quota of shares with business development, that is, “the amount of shares assigned to an applicant is determined by how much goods the applicant has underwrote for the company.

Yields compradors made from buying shares of insurers were mainly made up of dividends and security returns. First, insurance compradors as shareholders of Western insurance company was eligible to its high returns. “North China Insurance Company has made huge profits throughout the 1860s, and its shareholders receive a bonus as much as 60% to 80% of their investment, in addition to a 10% fixed dividend”

| [17] | Yan Pengfei et. History of Insurance in China 1805-1949 [M]. Shanghai: Shanghai Academy of Social Sciences Press, 1989. |

[17]

. In allocating margins, Western insurance company gave more weight to reward for shareholders, as well as contribution to company’s business. Canton Insurance Society announced to issue 100 new shares, and it stipulated that the two thirds in lieu of one third of profits be retained and allocated to contributing shareholders. In the Articles of Association of Hong Kong Fire Insurance Co., it was stated that “one third of its annual net profits be put in the reserve fund account, another one third be distributed in proportion to the shares held by each shareholder, and the remaining one third be allocated in proportion to the premiums contributed in the previous year. When its reserve fund reached a certain amount, Hong Kong Fire Insurance Co. distributed most of its profits as dividends. In years from 1884 to 1887, the company’s dividends accounted for 70% to 85% of its profits. Second, earnings from the security market. Appreciation of shares in the security market brought big bonuses to insurance compradors. “Since the establishment of the Hong Kong Fire Candle Insurance Company, its annual profit has been equivalent to 50 percent of its share capital, and the value of its shares once has risen to 400 percent. One British newspaper in Hongkong wrote that the prosperity was credited to the company’s managers, and He Dong was one of its Chinese shareholder managers

| [17] | Yan Pengfei et. History of Insurance in China 1805-1949 [M]. Shanghai: Shanghai Academy of Social Sciences Press, 1989. |

[17]

. After 1880s, shares of insurance companies were allowed to be freely trade, which made it easier for insurance companies to buy and sell shares. In 1881, Canton Insurance Company announced its prospectus on newspaper, saying that, the rule that shareholder should sign in Hongkong to sell shares was now replace with a new one, under which, if a Londoner, for example, would like to sell his shares in London, he could concluded the deal by signing in London first and informing the general-manager in Hongkong afterwards. The free trade of shares allowed insurance compradors to promptly cash in the wealth they’d reaped in the security market, accelerating capital flows.

The act of buying shares of Western insurance companies is, on the one hand, an important means for insurance compradors to accumulate capital; and on the other, it provides a channel for Western insurance industry to absorb Chinese capital. As Mr. Wang Jingyu argued, the bourgeoisie in modern China grew up by, to a large extent, buying shares of Western firms pillaging China. It was also the case with insurance capitalists in modern China.

4.2. Independence of Insurance Compradors and Western Insurance Industry

Insurance compradors has always taken a subordinate position to Western insurance businesses in the distribution of profits, and never had them had the final say in this regard. Their income has been constantly adjustment to meet Western insurers’ need for development. When Western insurers’ development stabilized, the proxy rate was fixed, leading to decrease in insurance compradors’ income. The decrease in income, psychological impact caused by uneven distribution of profits and huge difference therein, together with the maturity of strength (in capital and expertise), have made alienation from Western insurers an easy choice for insurance compradors.

On another front, by the end of the 19

th century, the Western insurance industry has grown to maturity in China, building a network stretching from coastal areas to inland; and at the same time, its capital and size had multiplied, and its monopoly of the market was initially established. Agencies for Western insurers have also made great progress. In 1866, Western insurance companies had 102 insurance agencies in 6 port cities in China, namely, Shanghai, Shantou, Xiamen, Fouzhou and Tianjin. By 1894, Western insurers and their agencies had extended their presence from coastal areas to inland, and the number of the agencies, according to statistics, stood roughly at 680

| [18] | Li Bizhang. Overview of the Development of Shanghai's Modern Trade Economy 1854-1989 [M]. Shanghai: Shanghai Academy of Social Sciences Press, 1993. |

[18]

.

With its insurance network in place, Western insurance industry’s capital and size have exploded. According to a report by British consul in Shanghai, the total capital of 6 insurance companies in Shanghai in 1875, Canton Insurance Office, Union Insurance Society of Canton, Yangtze Insurance Co., North China Insurance Association, Chinese Insurance Co., China and Japan Marine Insurance Co., amounted to 570000 pounds, which was around 2 million

liang at the then exchange rate

| [19] | Cox H, Biao H, Metcalfe S. Compradors, Firm Architecture and the 'Reinvention' of British Trading Companies: John Swire & Sons' Operations in Early Twentieth-Century China [J]. Business History, 2003, 45(2): 15-34. https://doi.org/10.1080/713999308 |

[19]

. By the end of 1895, the 6 companies had an authorized capital of close to 10 million

liang| [16] | Wang Jingyu.The Economic Aggression of Western Capitalism against China in the Nineteenth Century[M].Beijing:People's Publishing House,1983. |

[16]

, which, regardless of inflation and other factors, had on average increased approximately 5 times; and that of Canton Insurance Office, under Jardine Matheson Co. had increased nearly 18 times.

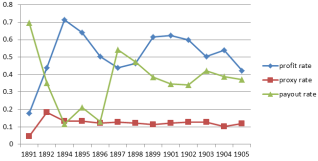

It is worthy of note that businessmen aim to maximize profits. Both Western merchants and insurance compradors seek to maximize their profits. Despite close cooperation between Western merchants and insurance compradors in pursuit of profits, conflicts and friction did took place, which was rooted in the distribution of profits. And the most notable concern regarding the distribution was the agency fee. As was analyzed above, agency fee, whose rate may vary from 10% to 60%, was largely controlled by insurance compradors. Proxy rate represented the value of insurance comprador’s social networks in the insurance market, exerting a positive effect on premium increase, and while a high proxy rate would hurt the interests of Western insurers. As aforementioned, therefore, insurance compradors asked of insurance companies for higher commission and proxy rate. So who has the final say in the distribution of profits, insurance company or compradors? Let’s look for the answer through analysis of the 1891-1905 data on profit margin, proxy rate and payout ratio of Yangtze Insurance Association.

Figure 1. Yangtsze Insurance Association 1891 --- 1905 profit rate, proxy rate, payout rate line chart.

The above chart reflects the characteristics in the development of Western insurance industry. (1) in the early stage of development, Western insurers needed the help of insurance compradors with their strong networks to expand agencies and build sales networks. Western insurers used high proxy rates to attract agencies for the purpose of expanding in the market, and the proxy rate was in a positive proportional relationship with profit rate. In this stage, agencies were very important to insurance companies; insurance compradors played a big role in the development of insurance companies and received a large amount of agent fee. However, the development driven by expansion was likely to cause volatile payout rates, making risks and profits uncontrollable. (2) As its capital strengthened, Western insurers adjusted their development strategies from expansion to risk management with a view to maximize profits; and the number and scale of agencies were gradually stabilized as were the proxy rate. At this point, the main task of Western insurers was to stabilize the proxy rate, payout rate and profit margin within a controllable range, maximizing profits with minimum costs. With the gradual stabilizing of agencies, proxy rate came to stabilize, and therefore the role and influence of insurance compradors waned.

In short, in the period of stable development, which was marked by stabilized agencies, duly managed risk, stable profits, Western insurers saw steady year-on-year increase in premiums and profits. No longer relying on compradors and agencies, Western insurers began to take a firm grip on proxy rates, payout rates and profit margins, bringing in steady and high returns.

The social networks of insurance compradors depreciated in light of Western insurance industry growing mature, and thus the insurance comprador system was phased out. Some Western insurers may still employ compradors, but the latter were completely subject to the former; some insurers employed Chinese managers in place of compradors. For example, when the Yangtsze Insurance Company entered stable development, its manager in 1900 announced in newspaper that “from today onwards, all premiums were on longer handed in to compradors”. In a bid to define limits to compradors’ power, Sun Fire Insurance Office’London branch empowered its Western manager to promote a running broker to comprador. Some American insurance companies no longer count their business on traditional compradors or agencies, but instead employed Chinese staff who had received Western education to do business as subsidiary manager or division head. This institution was popularized with the development of Western insurance industry. In 1927, Swire Group recruited a group of graduates from Hongkong University to serve as Chinese managers in its insurance department. After receiving sufficient training, these young managers became salaried employee of the companies

| [19] | Cox H, Biao H, Metcalfe S. Compradors, Firm Architecture and the 'Reinvention' of British Trading Companies: John Swire & Sons' Operations in Early Twentieth-Century China [J]. Business History, 2003, 45(2): 15-34. https://doi.org/10.1080/713999308 |

[19]

.

Insurance compradors were earliest exposed to the Western insurance idea and the business model of insurance enterprises, in the process of developing agencies for as well as buying share of Western insurers; they have accumulated a fair amount of capital with the returns from their contribution Western insurer’s development in China; and they have gradually quit Western insurance industry with the latter’s development. These factors have made insurance comprador the earliest group of Chinese insurance entrepreneurs. Tang Tingshu, Xu Run, Guo Ganzhang, Tang Maozhi, Ruan Licun, and among other insurance compradors, recognized pioneers in the Chinses insurance industry, have played an important role in the establishing of the first Chinese insurance businesses.

5. Conclusion

In conclusion, the history of China’s modern insurance industry features co-existence and co-development of Western insurance industry, Chinese national insurance industry, Chinese bureaucrat-capitalist insurance industry and insurance industry in revolutionary bases. Insurance compradors have played an important part in both the strengthening of Western insurance industry in China and in the birth of China’s insurance industry. They as a new type of businessman emerge out of the collision of Chinese and Western economy and culture. On the one hand, they assisted Western insurers monopolize the insurance market of China, causing an incalculable outflow of incalculable premiums from China; on the other, as intermediary for Western businesses entering Chinese insurance market and trailblazer Chinese businessmen setting foot in insurance business, insurance compradors have exerted a far-reaching impact on the modernization of Chinese insurance industry. Worthy of note here, they have also exerted significant impact on China’s early attempt at industrialization. Under the influence of Self-strengthening Movement, insurance compradors in late Qing China invested not only in insurance industry, but also actively in the modern industry.

Funding

The authors gratefully acknowledge financial support from China Postdoctoral Science Foundation and Youth Fund of Humanities and Social Science Research of the Ministry of Education of China.

Conflicts of Interest

The authors declare no conflicts of interest.

References

| [1] |

Wilkins M. Multinational enterprise in insurance: An historical overview [J]. Business History, 2009, 51(3): 334-363.

https://doi.org/10.1080/00076790902871636

|

| [2] |

Thai P. A Risky Business: The Tai Ping Insurance Company and Fire Insurance in China, 1928–1937[J]. Enterprise and Society, 2020:1-38.

https://doi.org/10.1017/eso.2020.47

|

| [3] |

G. C. Allen. Western Enterprise in Far Eastern economic development, China and Japan [M]. London: Jarrold and Sons Ltd Norwich, 1968.

|

| [4] |

Sha Weikai. China's Comprador System [M]. Beijing: The Commercial Press,1934.

|

| [5] |

Wang Chuifang. History of the West—Shanghai: 1843—1956 [M]. Shanghai: Shanghai Social Sciences Press, 2007.

|

| [6] |

Yan Pengfei, Shao Qiufen. Research on the History of Modern Insurance Relations between China and the United Kingdom [J]. Economic Review, 2000, (2): 97- 100.

https://doi.org/10.19361/j.er.2000.02.025

|

| [7] |

Nie Baozhang. Materials on the History of Shipping in Modern China [M]. Shanghai: Shanghai People Publishing House, 1983.

|

| [8] |

Yen-P'Ing Hao. The Comprador in Nineteenth Century China: Bridge between East and West[M].Shanghai: Shanghai Academy of Social Sciences Edition, 1989.

|

| [9] |

Xu Run. Shanghai Miscellaneous[M]. Zhuhai: Zhuhai Publishing House, 2006.

|

| [10] |

Dai Jianbin. History of Chinese Monetary Culture [M]. Shandong: Shandong Pictorial Publishing House, 2011.

|

| [11] |

Xu Dixin et. A History of the Development of Capitalism in China: Volume 2 [M]. Beijing: People's Publishing House, 2005.

|

| [12] |

Ma Xueqiang et. Between China and the West: The Social Life of The Compradors in Modern Shanghai [M]. Shanghai: Shanghai Dictionary Publishing House, 2009.

|

| [13] |

Wang Jingyu Chinese businessmens shareholding activities in foreign invaded enterprises in the nineteenth century [J]. Historical Research, 1965(4): 39-74.

https://doi.org/CNKI:SUN:LSYJ.0.1965-04-002

|

| [14] |

Zhang Kaiyuan et. al. History of the Revolution of 1911 [M]. Beijing: Oriental Press, 2010.

|

| [15] |

Wang Jingyu. Tang Tingshu Research [M].Beijing: China Social Sciences Press, 1983.

|

| [16] |

Wang Jingyu.The Economic Aggression of Western Capitalism against China in the Nineteenth Century[M].Beijing:People's Publishing House,1983.

|

| [17] |

Yan Pengfei et. History of Insurance in China 1805-1949 [M]. Shanghai: Shanghai Academy of Social Sciences Press, 1989.

|

| [18] |

Li Bizhang. Overview of the Development of Shanghai's Modern Trade Economy 1854-1989 [M]. Shanghai: Shanghai Academy of Social Sciences Press, 1993.

|

| [19] |

Cox H, Biao H, Metcalfe S. Compradors, Firm Architecture and the 'Reinvention' of British Trading Companies: John Swire & Sons' Operations in Early Twentieth-Century China [J]. Business History, 2003, 45(2): 15-34.

https://doi.org/10.1080/713999308

|

Cite This Article

-

APA Style

Xuecan, S., Rong, C. (2025). A Special Agent: Insurance Comprador for Western Insurers in 19th Century China. International Journal of Finance and Banking Research, 11(4), 81-90. https://doi.org/10.11648/j.ijfbr.20251104.12

Copy

|

Copy

|

Download

Download

ACS Style

Xuecan, S.; Rong, C. A Special Agent: Insurance Comprador for Western Insurers in 19th Century China. Int. J. Finance Bank. Res. 2025, 11(4), 81-90. doi: 10.11648/j.ijfbr.20251104.12

Copy

|

Download

AMA Style

Xuecan S, Rong C. A Special Agent: Insurance Comprador for Western Insurers in 19th Century China. Int J Finance Bank Res. 2025;11(4):81-90. doi: 10.11648/j.ijfbr.20251104.12

Copy

|

Download

-

@article{10.11648/j.ijfbr.20251104.12,

author = {Song Xuecan and Chen Rong},

title = {A Special Agent: Insurance Comprador for Western Insurers in 19th Century China

},

journal = {International Journal of Finance and Banking Research},

volume = {11},

number = {4},

pages = {81-90},

doi = {10.11648/j.ijfbr.20251104.12},

url = {https://doi.org/10.11648/j.ijfbr.20251104.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijfbr.20251104.12},

abstract = {The history of modern Chinese insurance is a history of foreign insurance industry to control and monopolize the old Chinese insurance market while the Chinese insurance industry tried to be independent and anti-monopoly. Insurance compradors have played an important role in the Western insurance “Indigenization” process in the 19th century China. Insurance buying is a form of western capital in modern insurance industry, which is born and comes for profit. This paper argues, to expand in Chinese market, Western insurers designed a set of system, based on social networks, incorporating marketing, incentive, and credit guarantee namely the insurance buying system; that is, the insurance comprador system, which has assisted Western insurers in monopolizing the Chinese insurance market and bred a group of parvenu insurance compradors. With the growth of both Western insurers and insurance compradors, their relationship has gradually turned from inter-dependence to independence. On the one hand, when Western insurers came to scale, risk control replaced market expansion as development priority, which necessitated the change from a business model weighing insurance compradors to that weighing professionalization and risk-control; on the other hand, insurance compradors founded Chinese insurance industry with the capital and know-how accumulated in working for Western insurers.

},

year = {2025}

}

Copy

|

Download

-

TY - JOUR

T1 - A Special Agent: Insurance Comprador for Western Insurers in 19th Century China

AU - Song Xuecan

AU - Chen Rong

Y1 - 2025/09/23

PY - 2025

N1 - https://doi.org/10.11648/j.ijfbr.20251104.12

DO - 10.11648/j.ijfbr.20251104.12

T2 - International Journal of Finance and Banking Research

JF - International Journal of Finance and Banking Research

JO - International Journal of Finance and Banking Research

SP - 81

EP - 90

PB - Science Publishing Group

SN - 2472-2278

UR - https://doi.org/10.11648/j.ijfbr.20251104.12

AB - The history of modern Chinese insurance is a history of foreign insurance industry to control and monopolize the old Chinese insurance market while the Chinese insurance industry tried to be independent and anti-monopoly. Insurance compradors have played an important role in the Western insurance “Indigenization” process in the 19th century China. Insurance buying is a form of western capital in modern insurance industry, which is born and comes for profit. This paper argues, to expand in Chinese market, Western insurers designed a set of system, based on social networks, incorporating marketing, incentive, and credit guarantee namely the insurance buying system; that is, the insurance comprador system, which has assisted Western insurers in monopolizing the Chinese insurance market and bred a group of parvenu insurance compradors. With the growth of both Western insurers and insurance compradors, their relationship has gradually turned from inter-dependence to independence. On the one hand, when Western insurers came to scale, risk control replaced market expansion as development priority, which necessitated the change from a business model weighing insurance compradors to that weighing professionalization and risk-control; on the other hand, insurance compradors founded Chinese insurance industry with the capital and know-how accumulated in working for Western insurers.

VL - 11

IS - 4

ER -

Copy

|

Download