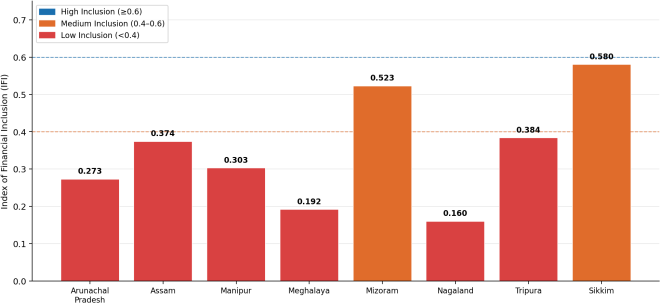

Financial inclusion particularly in regions with socio-economic challenges such as Northeast India, is a critical primary driver of social development and economic growth. This study seeks to analyses the financial inclusion across eight North-Eastern states of India- Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland, Tripura, Sikkim- by using a multidimensional approach which comprises three key dimensions of financial inclusion: Banking penetration, availability, and usage. Data were collected from secondary sources, including Database on Indian Economy (RBI), NABARD State Focus Papers and Census data. As the sample size is small and low correlation among variables, Principal Component Analysis (PCA) was not suited. Therefore, the study uses Sarma’s distance method (2008) to construct Financial Inclusion Index (FII) for eight states. The result of the study reveals significant disparities across states: Sikkim (FII= 0.58) and Mizoram (FII= 0.523) show high financial inclusion among the eight states and fall in medium inclusion category, because of robust banking access and penetration, while Nagaland (FII= 0.16), and Arunachal Pradesh (FII= 0.273), and Meghalaya (FII=0.192) display low financial inclusion, which reflects limited banking infrastructure and usage. Assam, Manipur, and Tripura fall in medium financial inclusion. The findings of the study underline the need of effective policy in lagging states to improve access and usage of financial services. The study contributes to the existing knowledge by providing a comparative state-level analysis of financial inclusion in North-East India, which helps policymakers, financial institutions and researchers in designing financial inclusion strategies.

| Published in | Innovation Management (Volume 1, Issue 2) |

| DOI | 10.11648/j.im.20260102.12 |

| Page(s) | 85-94 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

Financial Inclusion, Northeast India, Banking Penetration, Usage, Sarma Distance Method

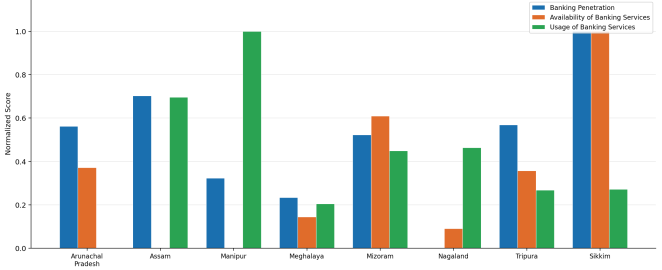

State | Total Number of Accounts | Population | Bank Accounts as Proportion of Population | Bank Penetration Dimension (d1) |

|---|---|---|---|---|

Arunachal Pradesh | 22,91,000 | 13,83,727 | 1.6557 | 0.5626 |

Assam | 5,67,23,000 | 3,12,05,576 | 1.8177 | 0.7035 |

Manipur | 35,47,000 | 25,70,390 | 1.3799 | 0.3228 |

Meghalaya | 37,89,000 | 29,66,889 | 1.2771 | 0.2333 |

Mizoram | 17,67,000 | 10,97,206 | 1.6105 | 0.5232 |

Nagaland | 19,96,000 | 19,78,502 | 1.0088 | 0.0000 |

Tripura | 61,08,000 | 36,73,917 | 1.6625 | 0.5685 |

Sikkim | 13,18,000 | 6,10,577 | 2.1586 | 1.0000 |

State | Total Offices | Population | Branch per 1000 Population | Availability Dimension (d2) |

|---|---|---|---|---|

Arunachal Pradesh | 257 | 13,83,727 | 0.185730 | 0.371893 |

Assam | 3,393 | 3,12,05,576 | 0.108731 | 0.000900 |

Manipur | 279 | 25,70,390 | 0.108544 | 0.000000 |

Meghalaya | 411 | 29,66,889 | 0.138529 | 0.144472 |

Mizoram | 258 | 10,97,206 | 0.235143 | 0.609968 |

Nagaland | 252 | 19,78,502 | 0.127369 | 0.090702 |

Tripura | 671 | 36,73,917 | 0.182639 | 0.356998 |

Sikkim | 193 | 6,10,577 | 0.316094 | 1.000003 |

State | Deposits (₹ Crore) | Credit (₹ Crore) | Credit-Deposit Ratio | Usage Dimension (d3) |

|---|---|---|---|---|

Arunachal Pradesh | 33,114 | 10,273 | 0.310231 | 0.000000 |

Assam | 2,34,070 | 1,46,867 | 0.627449 | 0.696679 |

Manipur | 16,806 | 12,866 | 0.765560 | 1.000000 |

Meghalaya | 37,779 | 15,241 | 0.403425 | 0.204674 |

Mizoram | 17,462 | 8,987 | 0.514660 | 0.448970 |

Nagaland | 18,789 | 9,792 | 0.521156 | 0.463236 |

Tripura | 42,140 | 18,224 | 0.432463 | 0.268448 |

Sikkim | 16,290 | 7,067 | 0.433824 | 0.271437 |

Rank | State | IFI Score | Inclusion Level | Category |

|---|---|---|---|---|

1 | Sikkim | 0.58 | Medium | 0.4–0.6 |

2 | Mizoram | 0.523 | Medium | 0.4–0.6 |

3 | Tripura | 0.384 | Low | 0.0–0.4 |

4 | Assam | 0.374 | Low | 0.0–0.4 |

5 | Manipur | 0.303 | Low | 0.0–0.4 |

6 | Arunachal Pradesh | 0.273 | Low | 0.0–0.4 |

7 | Meghalaya | 0.192 | Low | 0.0–0.4 |

8 | Nagaland | 0.16 | Low | 0.0–0.4 |

Dimension | Minimum | Maximum | Mean | Std. Dev. |

|---|---|---|---|---|

Banking Penetration (d1) | 0.000 | 1.000 | 0.489 | 0.305 |

Availability (d2) | 0.000 | 1.000 | 0.322 | 0.346 |

Usage (d3) | 0.000 | 1.000 | 0.419 | 0.312 |

FII | 0.160 | 0.580 | 0.349 | 0.148 |

RBI | Reserve Bank of India |

NABARD | National Bank for Agriculture and Rural Development |

FII | Financial Inclusion Index |

SDG | Sustainable Development Goal |

PMJDY | Pradhan Mantri Jan Dhan Yojana |

UPI | Unified Payments Interface |

KYC | Know Your Customer |

GDP | Gross Domestic Product |

ATM | Automated Teller Machine |

PCA | Principal Component Analysis |

BC | Business Correspondent |

SHG | Self Help Group |

| [1] | Annemalla, R., & Kasturi, A. (2025). Financial inclusion among Indian States: An analysis through financial inclusion index. Global Business Review, 09721509251356954. |

| [2] |

Aggarwal, R. (2014). Financial inclusion in India: Challenges and opportunities. International Journal of Research, 1(4), 557-567.

https://www.academia.edu/8227520/Financial_Inclusion_in_India_Challenges_and_Opportunities |

| [3] | Beck, T., Demirgüç-Kunt, A., & Levine, R. (2007). Finance, inequality and the poor. Journal of Economic Growth, 12(1), 27-49. |

| [4] | Behera, D., & Mishra, S. (2019). The extent of financial inclusion in the north-eastern states of India. Indian Journal of Social Research, 60(3). |

| [5] | Chhatoi, B. P., Sahoo, S. P., & Nayak, D. P. (2021). Assessing the Academic Journey of ‘Financial Inclusion’ from 2000 to 2020 through Bibliometric Analysis. Journal of Scientometric Research, 10(2), 148–159. |

| [6] | Dhar, P., & Barua, N. A. (2020). Financial Inclusion in India-A State-wise analysis. International Journal of Management (IJM), 11(10), 5. |

| [7] |

Garg, S., & Agarwal, P. (2014). Financial inclusion in India–a Review of initiatives and achievements. IOSR journal of business and Management, 16(6), 52-61.

https://d1wqtxts1xzle7.cloudfront.net/124479034/ed4d9132f72043b6220bf315d3a3a4d725b1-libre.pdf |

| [8] | Goel, S., & Sharma, R. (2017). Developing a financial inclusion index for India. Procedia computer science, 122, 949-956. |

| [9] | Gupta, S., Kumar, K., Mahajan, S., Narang, S., & Marwaha, P. (2025). A Comparative Analysis of Financial Inclusion Disparities Across Indian States and Union Territories. Exploresearch, 02(04), 114–126. |

| [10] | Honohan, P. (2008). Cross-country variation in household access to financial services. Journal of Banking & Finance, 32(11), 2493–2500. |

| [11] | Harithaa, ms. S., & alamelu, dr. K. (2026). Progress of financial inclusion in india’s aspirational districts: a zone-wise evaluation (2018-2025). International Journal of Research in Commerce and Management Studies, 08(02), 166–185. |

| [12] | Kapoor, S., & Mohandas, V. (2023). Measuring Financial Inclusion in India: An Approach. Indian Journal of Finance, 17(1), 27. |

| [13] |

Kapoor, R. (2022). Enabling financial inclusion in North-East India. Retrieved from

https://ranakapoor.in/enabling-financial-inclusion-in-north-east/ |

| [14] | Kaur, R., Singh, A. P., & Mishra, S. (2025). Predicting Economic Development Through the PMJDY Index for Financial Inclusion: Evidence from India. Indian Journal of Research in Capital Markets, 8–26. |

| [15] |

Kodan, A. S., Garg, N. K., & Kaidan, S. (2011). Financial inclusion: Status, issues, challenges and policy in northeastern region. The IUP Journal of Financial Economics, IX (2), 27-40.

https://www.proquest.com/openview/03c9d248900d03fbd28e92a0ed0a2612/1?pq-origsite=gscholar&cbl=54458 |

| [16] | Maity, S., & Majumder, A. (2024). A Nationwide Comparative Study on Financial Inclusion through PMJDY. SSRN Electronic Journal. |

| [17] |

Panja, G. (2024) Financial Inclusion and its Determinants: A Comparative Analysis in India and West Bengal.

http://timesjourney.co.in/wp-content/uploads/2025/05/TJ_2024_July_03.pdf |

| [18] | Prasuna, A., Kasturi, A., & Annemalla, R. (2024). Unveiling the factors influencing financial inclusion in India: a comprehensive analysis. Cogent Economics & Finance, 12(1). |

| [19] | Paramasivan, C., & Ganeshkumar, V. (2013). Overview of financial inclusion in India. International Journal of Management and Development Studies, Volume, (2). |

| [20] | Rangarajan, C. (2008). Report of the Committee on Financial Inclusion. Government of India, ministry of Finance. |

| [21] | Sethy, S. K., & Goyari, P. (2018). Measuring Financial Inclusion of Indian States: An Empirical Study. Indian Journal of Economics and Development, 14(1), 111. |

| [22] | Sarma, M., & Pais, J. (2010). Financial Inclusion and Development. Journal of International Development, 23(5), 613–628. |

| [23] |

Sarma, M. (2008). Index of financial inclusion (No. 215). Working paper.

https://www.econstor.eu/bitstream/10419/176233/1/icrier-wp-215.pdf |

| [24] | Yadav, V., Singh, B. P., & Velan, N. (2020). Multidimensional financial inclusion index for Indian states. Journal of Public Affairs, 21(3). Portico. |

APA Style

Sahani, R., Sharmacharjee, R. (2026). Financial Inclusion in Northeast India: A Multidimensional State-Level Analysis Using Sarma’s Distance Method. Innovation Management, 1(2), 85-94. https://doi.org/10.11648/j.im.20260102.12

ACS Style

Sahani, R.; Sharmacharjee, R. Financial Inclusion in Northeast India: A Multidimensional State-Level Analysis Using Sarma’s Distance Method. Innov. Manag. 2026, 1(2), 85-94. doi: 10.11648/j.im.20260102.12

@article{10.11648/j.im.20260102.12,

author = {Ritesh Sahani and Rajat Sharmacharjee},

title = {Financial Inclusion in Northeast India: A Multidimensional State-Level Analysis Using Sarma’s Distance Method},

journal = {Innovation Management},

volume = {1},

number = {2},

pages = {85-94},

doi = {10.11648/j.im.20260102.12},

url = {https://doi.org/10.11648/j.im.20260102.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.im.20260102.12},

abstract = {Financial inclusion particularly in regions with socio-economic challenges such as Northeast India, is a critical primary driver of social development and economic growth. This study seeks to analyses the financial inclusion across eight North-Eastern states of India- Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland, Tripura, Sikkim- by using a multidimensional approach which comprises three key dimensions of financial inclusion: Banking penetration, availability, and usage. Data were collected from secondary sources, including Database on Indian Economy (RBI), NABARD State Focus Papers and Census data. As the sample size is small and low correlation among variables, Principal Component Analysis (PCA) was not suited. Therefore, the study uses Sarma’s distance method (2008) to construct Financial Inclusion Index (FII) for eight states. The result of the study reveals significant disparities across states: Sikkim (FII= 0.58) and Mizoram (FII= 0.523) show high financial inclusion among the eight states and fall in medium inclusion category, because of robust banking access and penetration, while Nagaland (FII= 0.16), and Arunachal Pradesh (FII= 0.273), and Meghalaya (FII=0.192) display low financial inclusion, which reflects limited banking infrastructure and usage. Assam, Manipur, and Tripura fall in medium financial inclusion. The findings of the study underline the need of effective policy in lagging states to improve access and usage of financial services. The study contributes to the existing knowledge by providing a comparative state-level analysis of financial inclusion in North-East India, which helps policymakers, financial institutions and researchers in designing financial inclusion strategies.},

year = {2026}

}

TY - JOUR T1 - Financial Inclusion in Northeast India: A Multidimensional State-Level Analysis Using Sarma’s Distance Method AU - Ritesh Sahani AU - Rajat Sharmacharjee Y1 - 2026/04/24 PY - 2026 N1 - https://doi.org/10.11648/j.im.20260102.12 DO - 10.11648/j.im.20260102.12 T2 - Innovation Management JF - Innovation Management JO - Innovation Management SP - 85 EP - 94 PB - Science Publishing Group SN - 3071-5377 UR - https://doi.org/10.11648/j.im.20260102.12 AB - Financial inclusion particularly in regions with socio-economic challenges such as Northeast India, is a critical primary driver of social development and economic growth. This study seeks to analyses the financial inclusion across eight North-Eastern states of India- Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland, Tripura, Sikkim- by using a multidimensional approach which comprises three key dimensions of financial inclusion: Banking penetration, availability, and usage. Data were collected from secondary sources, including Database on Indian Economy (RBI), NABARD State Focus Papers and Census data. As the sample size is small and low correlation among variables, Principal Component Analysis (PCA) was not suited. Therefore, the study uses Sarma’s distance method (2008) to construct Financial Inclusion Index (FII) for eight states. The result of the study reveals significant disparities across states: Sikkim (FII= 0.58) and Mizoram (FII= 0.523) show high financial inclusion among the eight states and fall in medium inclusion category, because of robust banking access and penetration, while Nagaland (FII= 0.16), and Arunachal Pradesh (FII= 0.273), and Meghalaya (FII=0.192) display low financial inclusion, which reflects limited banking infrastructure and usage. Assam, Manipur, and Tripura fall in medium financial inclusion. The findings of the study underline the need of effective policy in lagging states to improve access and usage of financial services. The study contributes to the existing knowledge by providing a comparative state-level analysis of financial inclusion in North-East India, which helps policymakers, financial institutions and researchers in designing financial inclusion strategies. VL - 1 IS - 2 ER -

Department of Commerce, Assam University, Silchar, India

Information