This study was conducted to identify the primary financial determinants influencing the credit rating process for readymade garment (RMG) factories in Bangladesh based on seven commonly reported financial factors found in various credit rating reports. The data used in this study were collected from secondary sources, specifically from credit rating reports. These reports were gathered from 50 readymade garment (RMG) factories. This study measures the correlation between credit ratings and the seven common financial determinants through quantitative analysis using the bivariate (Pearson) correlation method. Additionally, a Boolean search technique was employed to collect related studies. In terms of data design, numerical values and positive/negative modifiers from long-term credit ratings (e.g., AAA1, AAA2, BBB1, BBB+, and BBB-) were removed for a better clarity. Data and findings are presented through graphical figures and statistics. The study reveals that rating agencies heavily rely on sales volume when assigning credit ratings to RMG factories in Bangladesh [Sales: r (48) = -.66 (long-term rating rank), p<.05; -.59 (short-term rating rank), p<.05]. Furthermore, the study shows that the majority of RMG factories have received a “ST-3” rating for the short term and a “BBB” rating for the long term. This exploratory study adds value as factory management can directly benefit from its insights, enabling them to understand the strategies needed to enhance their credit ratings. In addition, credit rating agencies will benefit from this study by adopting a more comprehensive framework for assigning credit ratings to RMG factories in Bangladesh.

| Published in | International Journal of Economics, Finance and Management Sciences (Volume 13, Issue 5) |

| DOI | 10.11648/j.ijefm.20251305.16 |

| Page(s) | 297-310 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Credit Rating, Credit Rating Inflation, Speculative Rating Grades, Non-Speculative Rating Grades, Readymade Garment, Trade off Reputation, Sustainable Supply Chain

Financial Determinants | Rating Rank (Long-Term) | Rating Rank (Short-Term) | |

|---|---|---|---|

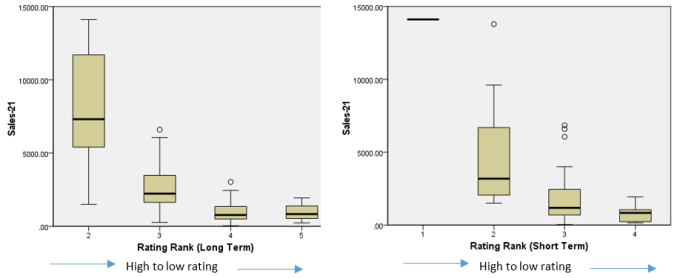

Sales-21 | Pearson Correlation | -.664** | -.587** |

Sig. (2-tailed) | <.001 | <.001 | |

N | 50 | 50 | |

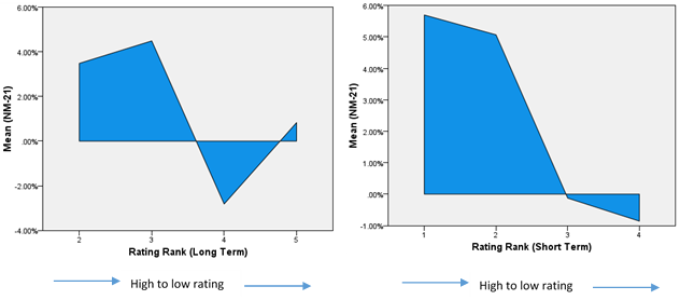

Net Profit Margin (NM-21) [21: FY 2020-2021] | Pearson Correlation | -.140 | -.116 |

Sig. (2-tailed) | .331 | .423 | |

N | 50 | 50 | |

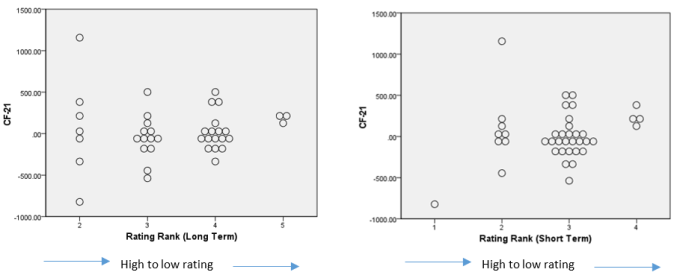

(Cash flow from Operations) CF-21 | Pearson Correlation | .036 | .202 |

Sig. (2-tailed) | .827 | .212 | |

N | 40 | 40 | |

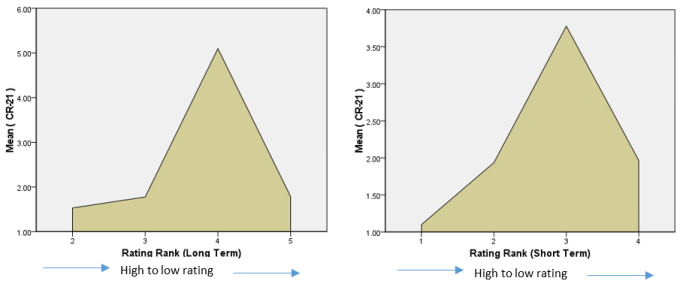

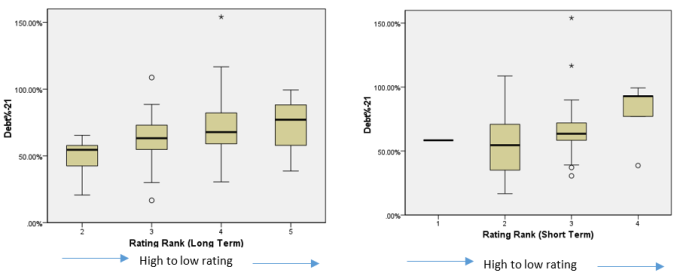

Current Ratio (CR-21) | Pearson Correlation | .125 | .042 |

Sig. (2-tailed) | .387 | .771 | |

N | 50 | 50 | |

Debt%-21 | Pearson Correlation | .311* | .269 |

Sig. (2-tailed) | .028 | .059 | |

N | 50 | 50 | |

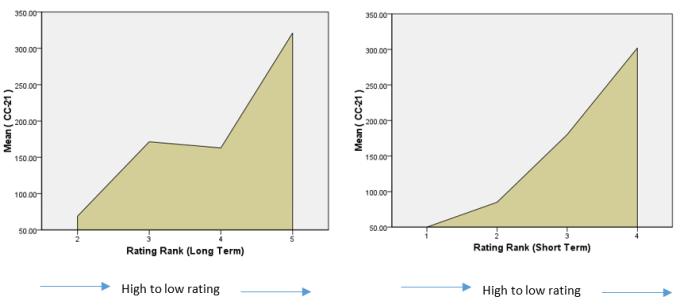

Cash conversion cycle (CC-21) | Pearson Correlation | .261 | .369* |

Sig. (2-tailed) | .095 | .016 | |

N | 42 | 42 | |

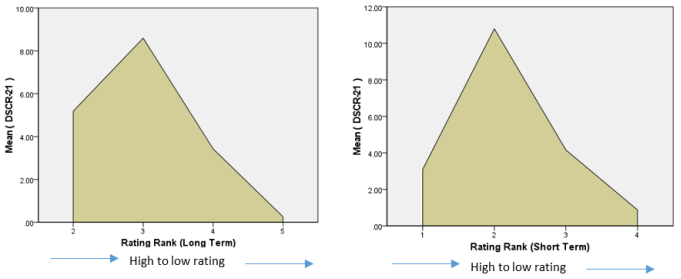

Debt service coverage ratio (DSCR-21) | Pearson Correlation | -.109 | -.191 |

Sig. (2-tailed) | .566 | .312 | |

N | 30 | 30 | |

Rating (Long Term)* | Rank | Remarks |

|---|---|---|

AAA | 1 | Non-Speculative Grades |

AA | 2 | Non-Speculative Grades |

A | 3 | Non-Speculative Grades |

BBB | 4 | Non-Speculative Grades |

BB | 5 | Speculative Grades |

B | 6 | Speculative Grades |

CCC | 7 | Speculative Grades |

CC | 8 | Speculative Grades |

C | 9 | Speculative Grades |

D | 10 | Speculative Grades |

Rating (Short Term) | Rank | Remarks |

|---|---|---|

ST-1 | 1 | Non-Speculative Grades |

ST-2 | 2 | Non-Speculative Grades |

ST-3 | 3 | Non-Speculative Grades |

ST-4 | 4 | Speculative Grades |

ST-5 | 5 | Speculative Grades |

ST-6 | 6 | Speculative Grades |

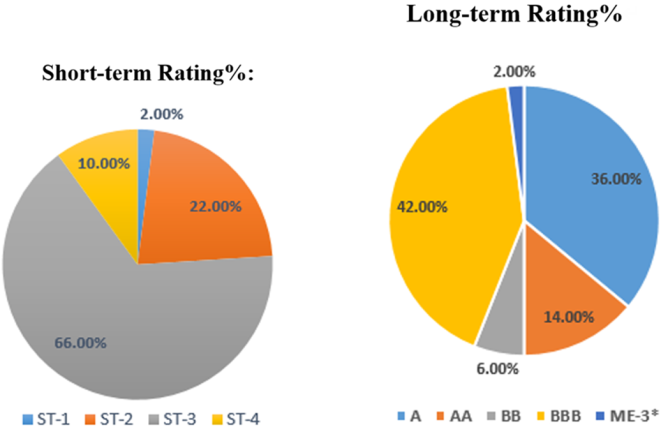

Rating | Rank | Count | Percent |

|---|---|---|---|

ST-1 | 1 | 1 | 2.0% |

ST-2 | 2 | 11 | 22.0% |

ST-3 | 3 | 33 | 66.0% |

ST-4 | 4 | 5 | 10.0% |

Rating | Rank | Count | Percentage |

|---|---|---|---|

AA | 2 | 7 | 14.00% |

A | 3 | 18 | 36.00% |

BBB | 4 | 21 | 42.00% |

BB | 5 | 3 | 6.00% |

ME-3* | 3 | 1 | 2.00% |

Correlations | Sales-21 | Rating Rank (Long Term) | Rating Rank (Short Term) | |

|---|---|---|---|---|

Sales-21 | Pearson Correlation | 1 | -.664** | -.587** |

Sig. (2-tailed) | <.001 | <.001 | ||

N | 50 | 50 | 50 | |

Correlations | NM-21 | Rating Rank (Long Term) | Rating Rank (Short Term) | |

|---|---|---|---|---|

NM-21 | Pearson Correlation | 1 | -.140 | -.116 |

Sig. (2-tailed) | .331 | .423 | ||

N | 50 | 50 | 50 | |

Correlations | CF-21 | Rating Rank (Long Term) | Rating Rank (Short Term) | |

|---|---|---|---|---|

CF-21 | Pearson Correlation | 1 | .036 | .202 |

Sig. (2-tailed) | .827 | .212 | ||

N | 40 | 40 | 40 | |

Correlations | CR-21 | Rating Rank (Long Term) | Rating Rank (Short Term) | |

|---|---|---|---|---|

CR-21 | Pearson Correlation | 1 | .125 | .042 |

Sig. (2-tailed) | .387 | .771 | ||

N | 50 | 50 | 50 | |

Correlations | Debt%-21 | Rating Rank (Long Term) | Rating Rank (Short Term) | |

|---|---|---|---|---|

Debt%-21 | Pearson Correlation | 1 | .311* | .269 |

Sig. (2-tailed) | .028 | .059 | ||

N | 50 | 50 | 50 | |

Correlations | CC-21 | Rating Rank (Long Term) | Rating Rank (Short Term) | |

|---|---|---|---|---|

CC-21 | Pearson Correlation | 1 | .261 | .369* |

Sig. (2-tailed) | .095 | .016 | ||

N | 42 | 42 | 42 | |

Correlations | DSCR-21 | Rating Rank (Long Term) | Rating Rank (Short Term) | |

|---|---|---|---|---|

DSCR-21 | Pearson Correlation | 1 | -.109 | -.191 |

Sig. (2-tailed) | .566 | .312 | ||

N | 30 | 30 | 30 | |

RMG | Readymade Garment |

SMEs | Small and Medium Enterprises |

CRA | Credit Rating Agency |

SDG | Sustainable Development Goals |

ESG | Environmental, Social and Governance |

SECB | Security Exchange Commission of Bangladesh |

CF | Cash Flow (Operation) |

CR | Current Ratio |

CC | Cash Conversion |

DSCR | Debt Service Coverage Ratio |

| [1] | Ubarhande, P. and Chandani, A. (2021) ‘Elements of Credit Rating: A Hybrid Review and Future Research Agenda’, Cogent Business & Management, 8(1), |

| [2] | Adegbite, G. (2018), “2008 Global financial crisis-ten years after; is another crisis ‘resonating’?”, SSRN Electronic Journal, pp. 1-11. |

| [3] | Tsunoda, J., Ahmed, M., & Islam, T. (2013), “Regulatory Framework and Role of Domestic Credit Rating Agencies in Bangladesh”, Asian Development Bank, pp. 1. |

| [4] |

Uddin, M. (2022), “Future bright for RMG sector after record year”, The Daily Star, 13 February, available at:

https://www.thedailystar.net/recovering-covid-reinventing-our-future/blueprint-brighter-tomorrow/news/future-bright-rmg-sector-after-record-year-2960541 (Accessed 01 January 2025) |

| [5] |

“About Garment Industry of Bangladesh”, BGMEA, available at:

https://www.bgmea.com.bd/page/AboutGarmentsIndustry (Accessed 01 January 2025) |

| [6] |

Rahman, S. (2021), “Reazuddin: The tailor who became the first RMG exporter from Bangladesh”, Tbsnews, 3 February, available at:

https://www.tbsnews.net/feature/panorama/reazuddin-tailor-who-became-first-rmg-exporter-bangladesh-196057 (Accessed 13 February 2025) |

| [7] | Sepulveda, J. and Akin, H. (2004), "Modeling a garment manufacturer's cash flow using object-oriented simulation," Proceedings of the 2004 Winter Simulation Conference, 2004, pp. 1176-1183 vol. 2, |

| [8] | Gupta, R. (2023), “Financial determinants of corporate credit ratings: An Indian evidence”, International Journal of Finance & Economics, 28(2), pp. 1622-1637, |

| [9] | Kaur, J., Vij, M. & Chauhan, A. K. (2023), “Signals influencing corporate credit ratings-a systematic literature review”. Decision 50, pp. 91-114, |

| [10] | Ma, Z., Ruan, L., Wang, D., & Zhang, H. (2021), “Generalist CEOs and Credit Ratings”, Contemporary Accounting Research, 38(2), pp. 1009-1036, |

| [11] | Bhandari, A., & Golden, J. (2021), “CEO political preference and credit ratings”, Journal of Corporate Finance, 68, |

| [12] | Raihan, S., Bourguignon, F., & Salam, U. (Eds.). (2024), “Is the Bangladesh Paradox Sustainable?: The Institutional Diagnostic Project”, Cambridge University Press, pp. 102, |

| [13] | Wu, J., Zhang, Z., & Zhou, S. X. (2022), “Credit Rating Prediction Through Supply Chains: A Machine Learning Approach”, Production and Operations Management, 31(4), pp. 1613-1629, |

| [14] | Amin, M. A., & Baldacci, R. (2025), “A mixed-method approach to develop an eco-robust supply chain management framework for Bangladeshi RMG industries”, Sustainable Futures, 9, pp. 1-2, |

| [15] | Roy, P. K. (2023), “Enriching the green economy through sustainable investments: An ESG-based credit rating model for green financing”, Journal of Cleaner Production, 420, pp. 1-3, |

| [16] | Biswas, M. K., Azad, A. K., Datta, A., Dutta, S., Roy, S., & Chopra, S. S. (2024), “Navigating Sustainability through Greenhouse Gas Emission Inventory: ESG Practices and Energy Shift in Bangladesh’s Textile and Readymade Garment Industries”, Environmental Pollution, 345, pp. 1-4, |

| [17] | Pineau, E., Le, P., & Estran, R. (2022), “Importance of ESG factors in sovereign credit ratings”, Finance Research Letters, 49, pp. 1-5, |

| [18] | Barua S., Kar D., & Mahbub F. B. (2018), “Risks and their management in ready-made garment industry: Evidence from the world’s second largest exporting nation”, Journal of Business and Management, 24(2), pp. 75-99, |

| [19] |

Prothom Alo (2022), “Which bank should you select to put your money?” 26 December, available at:

https://www.prothomalo.com/business/bank/vai6tdt7u8 (Accessed 09 March 2025) |

| [20] | Camanho, N., Deb, P., & Liu, Z. (2022), “Credit rating and competition”, International Journal of Finance & Economics, 27(3), pp. 2873-2897, |

| [21] | Akber, s & Saha, Rita & Tabassum, Karisma & Shamim, Dr. (2023), “Causes and Impact of Labor Unrest in RMG Sector; An Analysis on the Ready Made Garments Industries of Bangladesh”, 3, pp. 1-16. |

| [22] | Siew-Huan Ng, A., & Mohamed, M. A. S. (2020), “A Multi-Country Study Of Factors Affecting Credit Ratings Revisions”, International Journal of Business and Society, 21(3), pp. 1424-1443, |

| [23] | Abuhommous, A. A. A., Alsaraireh, A. S., & Alqaralleh, H. (2022), “The impact of working capital management on credit rating”, Financial Innovation, 8(1), 72, pp. 1-20, |

APA Style

Sadat, A. (2025). A Study on Credit Rating Factors of Readymade Garments in Bangladesh. International Journal of Economics, Finance and Management Sciences, 13(5), 297-310. https://doi.org/10.11648/j.ijefm.20251305.16

ACS Style

Sadat, A. A Study on Credit Rating Factors of Readymade Garments in Bangladesh. Int. J. Econ. Finance Manag. Sci. 2025, 13(5), 297-310. doi: 10.11648/j.ijefm.20251305.16

AMA Style

Sadat A. A Study on Credit Rating Factors of Readymade Garments in Bangladesh. Int J Econ Finance Manag Sci. 2025;13(5):297-310. doi: 10.11648/j.ijefm.20251305.16

@article{10.11648/j.ijefm.20251305.16,

author = {Anarus Sadat},

title = {A Study on Credit Rating Factors of Readymade Garments in Bangladesh

},

journal = {International Journal of Economics, Finance and Management Sciences},

volume = {13},

number = {5},

pages = {297-310},

doi = {10.11648/j.ijefm.20251305.16},

url = {https://doi.org/10.11648/j.ijefm.20251305.16},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijefm.20251305.16},

abstract = {This study was conducted to identify the primary financial determinants influencing the credit rating process for readymade garment (RMG) factories in Bangladesh based on seven commonly reported financial factors found in various credit rating reports. The data used in this study were collected from secondary sources, specifically from credit rating reports. These reports were gathered from 50 readymade garment (RMG) factories. This study measures the correlation between credit ratings and the seven common financial determinants through quantitative analysis using the bivariate (Pearson) correlation method. Additionally, a Boolean search technique was employed to collect related studies. In terms of data design, numerical values and positive/negative modifiers from long-term credit ratings (e.g., AAA1, AAA2, BBB1, BBB+, and BBB-) were removed for a better clarity. Data and findings are presented through graphical figures and statistics. The study reveals that rating agencies heavily rely on sales volume when assigning credit ratings to RMG factories in Bangladesh [Sales: r (48) = -.66 (long-term rating rank), p<.05; -.59 (short-term rating rank), p<.05]. Furthermore, the study shows that the majority of RMG factories have received a “ST-3” rating for the short term and a “BBB” rating for the long term. This exploratory study adds value as factory management can directly benefit from its insights, enabling them to understand the strategies needed to enhance their credit ratings. In addition, credit rating agencies will benefit from this study by adopting a more comprehensive framework for assigning credit ratings to RMG factories in Bangladesh.

},

year = {2025}

}

TY - JOUR T1 - A Study on Credit Rating Factors of Readymade Garments in Bangladesh AU - Anarus Sadat Y1 - 2025/09/26 PY - 2025 N1 - https://doi.org/10.11648/j.ijefm.20251305.16 DO - 10.11648/j.ijefm.20251305.16 T2 - International Journal of Economics, Finance and Management Sciences JF - International Journal of Economics, Finance and Management Sciences JO - International Journal of Economics, Finance and Management Sciences SP - 297 EP - 310 PB - Science Publishing Group SN - 2326-9561 UR - https://doi.org/10.11648/j.ijefm.20251305.16 AB - This study was conducted to identify the primary financial determinants influencing the credit rating process for readymade garment (RMG) factories in Bangladesh based on seven commonly reported financial factors found in various credit rating reports. The data used in this study were collected from secondary sources, specifically from credit rating reports. These reports were gathered from 50 readymade garment (RMG) factories. This study measures the correlation between credit ratings and the seven common financial determinants through quantitative analysis using the bivariate (Pearson) correlation method. Additionally, a Boolean search technique was employed to collect related studies. In terms of data design, numerical values and positive/negative modifiers from long-term credit ratings (e.g., AAA1, AAA2, BBB1, BBB+, and BBB-) were removed for a better clarity. Data and findings are presented through graphical figures and statistics. The study reveals that rating agencies heavily rely on sales volume when assigning credit ratings to RMG factories in Bangladesh [Sales: r (48) = -.66 (long-term rating rank), p<.05; -.59 (short-term rating rank), p<.05]. Furthermore, the study shows that the majority of RMG factories have received a “ST-3” rating for the short term and a “BBB” rating for the long term. This exploratory study adds value as factory management can directly benefit from its insights, enabling them to understand the strategies needed to enhance their credit ratings. In addition, credit rating agencies will benefit from this study by adopting a more comprehensive framework for assigning credit ratings to RMG factories in Bangladesh. VL - 13 IS - 5 ER -

Department of Accounting & Finance, American International University-Bangladesh, Dhaka, Bangladesh

Figure 1. Short-term & long-term rating summary from sample dataset.

Figure 2. Represents relationship between sales and credit rating rank.

Figure 3. Represents relationship between Net Profit Margin and credit rating rank.

Figure 4. Represents relationship between CFO and credit rating rank.

Figure 5. The relationship between current ratio and credit rating rank.

Figure 6. Represents relationship between debt% and credit rating rank.

Figure 7. Represents relationship between CC cycle (in days) and credit rating rank.

Figure 8. Represents relationship between DSCR and credit rating rank.

Information