1. Introduction

The banking sector has been significantly transformed by the introduction of various service delivery channels, most notably Automated Teller Machines (ATMs). ATMs have become a strategic technological cornerstone, fundamentally changing customer habits by providing 24/7 access to financial transactions without a human teller. This self-service capability has dramatically increased the accessibility and convenience of banking, reducing reliance on conventional branches and offering greater autonomy to customers

| [47] | Tambasi, J. R. (2019). Influence of electronic delivery services on customer satisfaction in savings and credit cooperatives, a case of Mwalimu National Sacco, Kenya [Unpublished master's thesis]. University of Nairobi. |

[47]

. This shift has made the quality of ATM services a critical factor for banks aiming to maintain a competitive advantage and enhance customer satisfaction

. The use of technology for such purposes aligns with the broader goals of Islamic finance and its contribution to Sustainable Development Goals (SDGs)

| [22] | Herindar, E., & Shikur, A. A. (2023). Islamic Finance and Sustainable Development Goals (SDGs): Text Analytics using R. Finance and Sustainability, 1(1). https://doi.org/10.58968/fs.v1i1.420 |

[22]

and the use of research to map developments in areas like renewable energy in Islamic countries

.

The introduction of ATMs, while offering undeniable convenience, has also brought forth challenges that require careful investigation. Specifically, concerns regarding service delivery and its subsequent impact on customer satisfaction have become increasingly prominent. One of the biggest issues is the prevalence of service disruptions and failures that hinder ATM reliability. A study by

| [7] | Asfaw, S. (2024). Examining the effects of ATM service quality on customers satisfaction: In the case of Dashen Bank Western District, Addis Ababa, Ethiopia, 2024 [Unpublished master's thesis]. St. Mary's University. |

[7]

highlighted customer complaints at Dashen Bank about long waiting lines, problems with the network system, and frequent ATM breakdowns. These operational inefficiencies cause inconvenience and lead to dissatisfaction, significantly deteriorating the entire banking experience. Such issues can also impact overall firm performance in the context of bank regulations in Ethiopian commercial banks

| [52] | Yusuf, J. M., & Shikur, A. A. (2023). Bank Regulations and Firm Performance: In the Case of Ethiopian Commercial Banks. International Journal of Finance and Banking Research, 9(4), 58-67. https://doi.org/10.11648/j.ijfbr.20230904.11 |

[52]

and are crucial to address to build trust, similar to the critical role of trust and institutions in influencing zakat payments

| [45] | Shikur, A. A., Aslan, H., & Fodol, M. Z. (2025). Factors influencing zakat payment among Ethiopian Muslims: a PLS-SEM analysis. International Journal of Islamic and Middle Eastern Finance and Management, 18(5), 1150-1175. https://doi.org/10.1108/imefm-07-2024-0362 |

[45]

. Understanding the comprehensive relationship between ATM service quality dimensions and customer satisfaction presents another level of difficulty. Consequently, identifying which aspects of service quality are most critical can help banks focus on their improvements and allocate resources wisely.

Several studies have emphasized that a better ATM service delivery plays a significant role in customer satisfaction. For instance,

examined the significant impact of ATM service delivery on customer satisfaction, identifying key dimensions such as reliability, empathy, network, and price. A study by

| [4] | Aktar, M. S. (2024). The impacts of ATM service quality on client satisfaction and loyalty: a study on selected banks in Bangladesh. Journal of Business Studies, 4(1), 1-20. https://doi.org/10.58753/jbspust.4.1.2023.17 |

[4]

also explored the dimensions of reliability, empathy, affordability, fulfillment, privacy, and ease of use and their impact on customer satisfaction. The significant role of ATM service delivery in enhancing customer satisfaction is further supported by a study from

| [47] | Tambasi, J. R. (2019). Influence of electronic delivery services on customer satisfaction in savings and credit cooperatives, a case of Mwalimu National Sacco, Kenya [Unpublished master's thesis]. University of Nairobi. |

[47]

, which emphasized factors like price, network, reliability, and empathy.

In the Ethiopia context, there's an increasing investment in transaction technology, especially ATMs. Yet, some studies suggest that ATM development and implementation are not fully meeting customer demands. The availability of ATMs is not sufficient compared to the country's quickly growing urban population. This gap highlights the importance of thoroughly examining the ATM service delivery and its impact on customer satisfaction with the Ethiopian banks

. Similarly,

| [34] | Nigatua, A. G., Belete, A. A., & Habtie, G. M. (2023). Effects of automated teller machine service quality on customer satisfaction: Evidence from commercial bank of Ethiopia. Heliyon, 9(11), e19132. https://doi.org/10.1016/j.heliyon.2023.e19132 |

[34]

examined the influence of ATM service delivery on customer satisfaction in Ethiopian commercial banks. Research by

| [46] | Solomon, N. (2023). Effect of ATM service quality on customer satisfaction: Case study of selected bank [Unpublished master's thesis]. St. Mary's University. |

[46]

conducted the effect of ATM service quality on customer satisfaction. These studies consistently highlight the importance of reliable and efficient ATM services in maintaining customer satisfaction. Moreover, variations in service delivery across different banks and regions can lead to disparities in customer experience.

Many studies have investigated the broader implications of service quality impacts on the whole banking sector. It was established by

| [10] | Embiale, Y. (2016). The effect of automatic teller machine service quality on customer satisfaction: The case of the Commercial Bank of Ethiopia in Hawassa City. Journal of Engineering and Economic Development, 3(2). https://doi.org/10.7176/jmcr/58-01 |

[10]

that argues that in a very competitive banking environment, service quality is key to being different and building strong customer relationships and loyalty. Specific geographical locations do not limit the problems with ATM services. For instance,

| [28] | Kumbhar, V. M. (2011). Customers' satisfaction in ATM service: An empirical evidences from public and private sector banks in India. Management Research and Practice, 3(2), 24-35. |

[28]

revealed that customers in India are concerned about efficiency, security, responsiveness, cost-effectiveness, problem handling, and contact service in both public and private sector banks. A study by

| [32] | Mwatsika, C. (2016). Factors influencing customer satisfaction with ATM banking. International Journal of Academic Research in Business and Social Sciences, 6(2), 172-185. https://doi.org/10.6007/ijarbss/v6-i2/2002 |

[32]

emphasized the importance of banks in Malawi addressing factors affecting customer satisfaction to maintain a competitive advantage in ATM banking. It was emphasized by

| [35] | Nshimiyimana, A., & Chen, W. (2019). An empirical study analyzing the ATM service quality and customer satisfaction relationship in Rwanda. International Journal of Business and Economics Research, 8(6), 439-451. https://doi.org/10.11648/j.ijber.20190806.24 |

[35]

emphasized that ATMs are a key part of modern banking and stressed that banks need to ensure their efficiency and customer-oriented operation. A study by

| [23] | Hoque, M. A., Jahan, F., & Begum, F. (2024). Exploring the nexus of ATM service quality, customer satisfaction, and loyalty in the private banking sector in Bangladesh. Pakistan Journal of Life and Social Sciences, 22(1), 1091-1104. https://doi.org/10.57239/pjlss-2024-22.1.0074 |

[23]

examined the relationship between ATM service delivery, customer satisfaction, and loyalty in Bangladesh. Furthermore

| [47] | Tambasi, J. R. (2019). Influence of electronic delivery services on customer satisfaction in savings and credit cooperatives, a case of Mwalimu National Sacco, Kenya [Unpublished master's thesis]. University of Nairobi. |

[47],

studied how electronic services, including ATMs, influence customer satisfaction in Kenya. Customer satisfaction is also influenced by other factors such as attitude and perceived behavioral control, as seen in studies on halal food purchasing behavior

| [42] | Salmah, S., & Shikur, A. A. (2023). The Relationship of Attitude, Perceived Behavioral Control, Subjective Norm on Halal Food Purchasing Behavior on Indonesian Muslim Millennials. Ekonomi Islam Indonesia, 5(1). https://doi.org/10.58968/eii.v5i1.258 |

[42]

. Similarly, studies in Ethiopia

| [1] | Adane, M. D., Wale, T., & Meried, E. W. (2021). Determinants of automated teller machine deployment in commercial banks of Ethiopia. Heliyon, 7(8). https://doi.org/10.1016/j.heliyon.2021.e07712 |

| [47] | Tambasi, J. R. (2019). Influence of electronic delivery services on customer satisfaction in savings and credit cooperatives, a case of Mwalimu National Sacco, Kenya [Unpublished master's thesis]. University of Nairobi. |

[1, 47]

have also proved the significant impact of ATM service quality on customer satisfaction. This gap highlights the necessity for optimizing ATM service quality to meet the changing needs of the customer base, and this applies to all financial institutions, including those that provide Islamic microfinance services as a tool for poverty reduction

| [44] | Shikur, A. A., & Akkas, E. (2024). Islamic microfinance services: a catalyst for poverty reduction in eastern Ethiopia. International Journal of Islamic and Middle Eastern Finance and Management, 17(4), 770-788. https://doi.org/10.1108/imefm-09-2023-0327 |

[44]

.

For these reasons, a comprehensive investigation of ATM service delivery and its impact on customer satisfaction is of paramount importance in the ethical and service-oriented framework of Islamic banking. Therefore, this study is conducted to identify the determinants of ATM service delivery and its influence on customer satisfaction in the case of the Bank of Abyssinia's Dire Dawa Interest-Free Branch.

2. Literature Review

2.1. Theoretical Review

2.1.1. The Concept of ATM

An ATM typically consists of a Central Processing Unit (CPU) that controls the user interface and transaction devices; a magnetic or chip card reader for identifying the customer; a display used by the customer to perform transactions; function buttons, and a record printer that provides the customer with a transaction receipt

| [13] | Garba, M. (2019). Adoption of information and communications technology for cashless economy in nigerian banking sector. Kaduna Journal of Postgraduate Research, 2(2). |

[13]

. Most ATMs are connected to interbank networks, allowing people to withdraw and deposit money from machines not belonging to their bank or even located in a different country. An Automated Teller Machine (ATM) is a modern computerized telecommunication electronic device that enables customers to conduct financial transactions generally outside normal banking hours without the need for a human clerk. To ensure security, safety, privacy, and accuracy, banking authorities provide their customers with a plastic ATM card containing a magnetic strip and a Personal Identification Number (PIN)

| [3] | Akomolafe, D. T., & Afeni, B. O. (2014). Using database management system to generate, manage and secure personal identification numbers (PIN). Journal of Software Engineering and Applications, 7(05), 461. https://doi.org/10.4236/jsea.2014.75043 |

[3]

. This innovation in banking aligns with the principles of providing accessible and trustworthy financial services, which is a core tenet of Islamic banking and its broader objective of contributing to Sustainable Development Goals (SDGs)

| [22] | Herindar, E., & Shikur, A. A. (2023). Islamic Finance and Sustainable Development Goals (SDGs): Text Analytics using R. Finance and Sustainability, 1(1). https://doi.org/10.58968/fs.v1i1.420 |

[22]

. ATMs offer 24-hour banking services to bank customers, such as cash withdrawal, funds transfer, balance inquiry, and bill payment. In the context of e-banking, ATM services play an important role in enhancing customer satisfaction by making banking transactions easier for customers. ATMs are placed not only near or inside bank premises but also in locations such as shopping centers/malls, airports, and restaurants. These represent two types of ATM installations: on-premises and off-premises. Financial institutions and independent sales organizations (ISOs) deploy off-premises machines when there is a straightforward cash need

| [5] | Ali, P. I. (2016). Impact of automated teller machine on banking services delivery in Nigeria: a stakeholder analysis. Cadernos de Educação Tecnologia e Sociedade, 9(1), 64-72. https://doi.org/10.14571/cets.v9.n1.64-72 |

[5]

.

2.1.2. Purpose of ATM

In today's world, Automated Teller Machines (ATMs) have become an invaluable asset, widely regarded as one of the most beneficial services provided by the banking sector to all account holders. Their hallmark is round-the-clock availability, granting customers the liberty to access cash, within specified limits, at any hour of the day or night

. From a service perspective, ATM banking embodies a product rich in features and attributes designed to fulfill both stated and unstated customer needs. In Islamic finance, achieving customer satisfaction through these services is a matter of fulfilling the ethical duty of providing excellent and accessible service (amanah) and building trust with the community

| [45] | Shikur, A. A., Aslan, H., & Fodol, M. Z. (2025). Factors influencing zakat payment among Ethiopian Muslims: a PLS-SEM analysis. International Journal of Islamic and Middle Eastern Finance and Management, 18(5), 1150-1175. https://doi.org/10.1108/imefm-07-2024-0362 |

[45]

. Achieving customer satisfaction hinges on these attributes, delivering a level of service quality that meets or exceeds customer expectations. Consequently, for banks to truly satisfy their clientele through ATM services, managers must possess a profound understanding of the specific features and attributes of ATM banking that contribute to superior service quality

| [36] | O'Brien, G., Xiao, G., & Mason, M. (2019). Digital transformation game plan: 34 tenets for masterfully merging technology and business. O'Reilly Media. |

[36]

. Beyond everyday banking, ATMs offer significant advantages, particularly for travelers. They negate the necessity of carrying large sums of cash, providing a secure and accessible means to obtain local currency

| [2] | Adu, C. A. (2016). Cashless policy and its effects on the Nigerian economy. European Journal of Business, Economics and Accountancy, 4(2), 81-88. |

[2]

. Additionally, ATMs extend their utility by enabling users to manage and pay their bills

| [50] | Thomas, A., Pfeifer, J., Moore, S., Meyer, D., Yap, L., & Armstrong, A. (2013). Evaluation of the removal of ATMs from gaming venues in Victoria, Australia. Evaluation. https://doi.org/10.1093/benz/9780199773787.article.b00140438 |

[50]

.

2.1.3. Customer Satisfaction

Customer satisfaction, the dependent variable in this study, refers to the degree to which customers feel satisfied with their experience with ATM services. It is a multi-dimensional construction that can be influenced by various factors.

| [7] | Asfaw, S. (2024). Examining the effects of ATM service quality on customers satisfaction: In the case of Dashen Bank Western District, Addis Ababa, Ethiopia, 2024 [Unpublished master's thesis]. St. Mary's University. |

| [14] | Gessese, N. B. (2018). Factors affecting customer satisfaction towards ATM service: A case study of Commercial Bank of Ethiopia in Addis Ababa. Journal of Marketing and Consumer Research, 48, 1-8. |

[7, 14]

examined customer satisfaction in the context of ATM services in Ethiopia. A comparative study of customer satisfaction in ATM services between public and private sector banks in India was conducted by

| [28] | Kumbhar, V. M. (2011). Customers' satisfaction in ATM service: An empirical evidences from public and private sector banks in India. Management Research and Practice, 3(2), 24-35. |

[28]

. The impact of service quality on customer satisfaction was also studied by

| [29] | Lulit, A. M. (2019). Factors affecting customer satisfaction in ATM service: The case of United Bank S. C. in Addis Ababa, Ethiopia. Journal of Accounting and Financial Management, 5(2), 34-47. |

[29]

. Customer satisfaction in the context of ATM usage can be defined as a customer's overall feeling of contentment or pleasure with the ATM transaction experience. The customer shapes this feeling by comparing their expectations of the service with their actual experience. If the experience meets or exceeds expectations, the customer is satisfied. Conversely, if the experience falls short, the customer is dissatisfied. This concept of satisfaction is a key measure of the bank's adherence to its ethical responsibilities within an Islamic framework.

2.1.4. Service Delivery

Service delivery is a multifaceted concept that essentially reflects how well a delivered service meets or exceeds customer expectations

. It is not merely about the outcome of a service but also encompasses the entire service experience, including the interactions, the environment, and the reliability of the provider

. In today's intensely competitive business landscape, service quality emerges as a crucial differentiator, significantly influencing customer relationships and nurturing loyalty

| [10] | Embiale, Y. (2016). The effect of automatic teller machine service quality on customer satisfaction: The case of the Commercial Bank of Ethiopia in Hawassa City. Journal of Engineering and Economic Development, 3(2). https://doi.org/10.7176/jmcr/58-01 |

[10]

. Researchers have proposed several models and dimensions to understand and measure service quality. One of the most widely recognized frameworks is the SERVQUAL model, which identified five key dimensions, often remembered by the acronym RATER

| [40] | Parasuraman, A., Zeithaml, V. A., & Berry, L. L. (1988). SERVQUAL: A multiple-item scale for measuring consumer perceptions of service quality. Journal of Retailing, 64(1), 12-40. https://doi.org/10.1037/t09264-000 |

[40]

.

Reliability: This dimension concerns the ability to perform the promised service dependably and accurately. In banking, this translates to accurate transaction processing, keeping promises regarding service delivery timelines, and error-free account statements. Reliability is fundamental to building trust and long-term customer relationships

| [53] | Zeithaml, V. A., Parasuraman, A., & Berry, L. L. (1990). Delivering quality service: Balancing customer perceptions and expectations. Free Press. https://doi.org/10.1177/0092070393211001 |

| [10] | Embiale, Y. (2016). The effect of automatic teller machine service quality on customer satisfaction: The case of the Commercial Bank of Ethiopia in Hawassa City. Journal of Engineering and Economic Development, 3(2). https://doi.org/10.7176/jmcr/58-01 |

[53, 10]

.

Responsive: This term involves the willingness of service providers to help customers and provide prompt service. In banking, the term could mean the speed at which customer queries are addressed, the promptness of loan approvals, and the readiness of staff to assist with issues. In today's fast-paced environment, responsiveness is crucial for customer satisfaction

| [30] | Mols, N. P. (2000). The Internet and relationship marketing in financial services. The International Journal of Bank Marketing, 18(7), 313-321. https://doi.org/10.1108/10662240010312093 |

| [40] | Parasuraman, A., Zeithaml, V. A., & Berry, L. L. (1988). SERVQUAL: A multiple-item scale for measuring consumer perceptions of service quality. Journal of Retailing, 64(1), 12-40. https://doi.org/10.1037/t09264-000 |

[30, 40]

.

Tangibles: The term refers to the physical appearance of facilities, equipment, personnel, and communication materials. For instance, in a banking context, such factors could include the cleanliness and aesthetics of the branch, the modernness of ATMs, and the professional appearance of staff. These tangible elements create a first impression and influence customer perceptions of service quality

.

Empathy: The term focuses on the caring, individualized attention provided to customers. In banking, the term means understanding customer needs, providing personalized service, and showing care and concern. Demonstrating empathy can significantly enhance customer loyalty and create a positive service experience

.

Assurance: This adjective relates to the knowledge and courtesy of employees and their ability to inspire trust and confidence.

2.1.5. Service Delivery and Customer Satisfaction

The foundation of this review lies in the well-established link between service quality and customer satisfaction.

| [40] | Parasuraman, A., Zeithaml, V. A., & Berry, L. L. (1988). SERVQUAL: A multiple-item scale for measuring consumer perceptions of service quality. Journal of Retailing, 64(1), 12-40. https://doi.org/10.1037/t09264-000 |

[40]

developed the SERVQUAL model, which identifies key dimensions of service quality, including reliability, responsiveness, assurance, tangibles, and empathy. While not specific to ATMs, this model provides a valuable framework for understanding how customers evaluate service quality in various contexts, including banking. Furthermore

applies this framework in the context of ATM services. Additionally,

| [38] | Puspita, A. T., & Shikur, A. A. (2023). Islamic financial stability: Previous research based on Scopus database. Review on Islamic Accounting, 3(1). https://doi.org/10.58968/ria.v3i1.317 |

[38]

explored the cognitive, effective, and attribute satisfaction bases, providing further theoretical grounding for understanding how service delivery dimensions influence customer satisfaction in the context of ATM usage.

2.1.6. Technology Acceptance Model (TAM)

The Technology Acceptance Model (TAM) explains how users come to accept and use technology. Developed by

| [9] | Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319-340. https://doi.org/10.2307/249008 |

[9]

, TAM suggests that perceived usefulness and perceived ease of use are the two main factors that influence an individual's intention to use a technology. In the context of ATM services, TAM can help explain why some customers are more satisfied than others. For example, if customers perceive ATMs as simple to use and useful for their banking needs, they are more likely to be satisfied with ATM services. This is consistent with studies that have examined how factors such as attitude and perceived behavioral control influence consumer behavior, such as in the case of halal food purchasing among Indonesian Muslim millennials

| [42] | Salmah, S., & Shikur, A. A. (2023). The Relationship of Attitude, Perceived Behavioral Control, Subjective Norm on Halal Food Purchasing Behavior on Indonesian Muslim Millennials. Ekonomi Islam Indonesia, 5(1). https://doi.org/10.58968/eii.v5i1.258 |

[42]

. In similar way

| [4] | Aktar, M. S. (2024). The impacts of ATM service quality on client satisfaction and loyalty: a study on selected banks in Bangladesh. Journal of Business Studies, 4(1), 1-20. https://doi.org/10.58753/jbspust.4.1.2023.17 |

[4]

highlights the importance of ease of use as one dimension of ATM service delivery.

2.1.7. Self-Service Technology (SST) and ATM Service

ATMs are a prime example of self-service technology (SST), which has become increasingly prevalent in the banking industry. A study by

| [24] | Iberahim, H., Taufik, N. R. M., & Shamsudin, M. F. (2016). Service quality and customer satisfaction: The mediating effect of customer relationship management (CRM). Journal of Business and Retail Management Research, 10(2), 84-97. |

[24]

highlights the importance of SST in retail banking, noting that the interface between humans and machines is crucial in today's technology-driven world. The adoption of SST, such as ATMs, aims to enhance efficiency, reduce costs, and improve customer convenience. This convenience, in turn, is a key driver of customer satisfaction. As technology advances, understanding how customers perceive and interact with SST becomes essential for optimizing service delivery. This is especially relevant in the context of Islamic finance, where technological solutions like ATMs can be leveraged as a tool for economic development and poverty reduction through initiatives such as Islamic microfinance services

| [44] | Shikur, A. A., & Akkas, E. (2024). Islamic microfinance services: a catalyst for poverty reduction in eastern Ethiopia. International Journal of Islamic and Middle Eastern Finance and Management, 17(4), 770-788. https://doi.org/10.1108/imefm-09-2023-0327 |

[44]

.

2.2. Empirical Review

2.2.1. Studies Outside Ethiopia

A substantial body of empirical research conducted across the globe confirms the significant and positive impact of ATM service delivery on customer satisfaction. Initial studies set the stage by showing the important connection between ATM service quality and customer satisfaction, as seen in the research by

| [23] | Hoque, M. A., Jahan, F., & Begum, F. (2024). Exploring the nexus of ATM service quality, customer satisfaction, and loyalty in the private banking sector in Bangladesh. Pakistan Journal of Life and Social Sciences, 22(1), 1091-1104. https://doi.org/10.57239/pjlss-2024-22.1.0074 |

[23]

in Bangladesh. This connection is paramount, as a bank's ability to provide reliable services is a fundamental component of building trust (amanah) with its clientele, a core principle in both conventional and Islamic finance

. Building upon this, subsequent studies have delved into the nuances of service quality, seeking to pinpoint the specific dimensions that most powerfully influence how customers evaluate their ATM experiences. For instance,

| [4] | Aktar, M. S. (2024). The impacts of ATM service quality on client satisfaction and loyalty: a study on selected banks in Bangladesh. Journal of Business Studies, 4(1), 1-20. https://doi.org/10.58753/jbspust.4.1.2023.17 |

[4]

, also in Bangladesh, identified a comprehensive set of eight key dimensions of ATM service quality and empirically demonstrated their strong correlation with overall client satisfaction. In a different geographical focus,

| [28] | Kumbhar, V. M. (2011). Customers' satisfaction in ATM service: An empirical evidences from public and private sector banks in India. Management Research and Practice, 3(2), 24-35. |

[28]

research in India illuminated the specific factors that customers prioritize when assessing the quality of ATM services.

The consistent relationship between ATM service quality and customer satisfaction has been observed and analyzed across a diverse range of geographical contexts, underscoring its universal relevance in the banking industry. Studies conducted in Rwanda, Nigeria, Kenya, and Brunei Darussalam all contribute to this global consensus

| [35] | Nshimiyimana, A., & Chen, W. (2019). An empirical study analyzing the ATM service quality and customer satisfaction relationship in Rwanda. International Journal of Business and Economics Research, 8(6), 439-451. https://doi.org/10.11648/j.ijber.20190806.24 |

| [11] | Farayibi, A. O. (2016). Service delivery and customer satisfaction in Nigerian banks. MPRA Paper No. 73612. Munich Personal RePEc Archive. https://doi.org/10.2139/ssrn.2836963 |

| [48] | Tasaw, M. M. (2019). Impact of automated teller machine (ATM) service quality dimensions on customer satisfaction: A case study of Awash Bank selected branches in Addis Ababa, Ethiopia. Journal of Marketing and Consumer Research, 57, 1-10. https://doi.org/10.7176/jmcr/72-02 |

| [6] | Amin, M. (2016). Internet banking service quality and its implications on customer satisfaction and loyalty. International Journal of Bank Marketing, 34(3), 280-306. https://doi.org/10.1108/ijbm-10-2014-0139 |

[35, 11, 48, 6]

. More recent empirical investigations reinforce these earlier findings. For instance,

| [26] | Islam, M. S., Hossain, M. A., & Islam, M. T. (2020). Impact of ATM service quality on customer satisfaction and brand image: Evidence from the banking sector of Bangladesh. Journal of Asian Finance, Economics and Business, 7(10), 815-824. https://doi.org/10.58753/jbspust.4.1.2023.17 |

[26]

not only reaffirmed the positive impact of ATM service quality on customer satisfaction in Bangladesh but also extended the analysis to demonstrate its positive influence on a bank's overall brand image. This positive brand image is crucial for all financial institutions, especially those operating under an ethical framework such as Islamic banking, where public perception is closely tied to the institution's commitment to social responsibility and its contribution to global goals, such as the Sustainable Development Goals (SDGs)

| [22] | Herindar, E., & Shikur, A. A. (2023). Islamic Finance and Sustainable Development Goals (SDGs): Text Analytics using R. Finance and Sustainability, 1(1). https://doi.org/10.58968/fs.v1i1.420 |

[22]

. A related study in Indonesia found that general risk significantly influences consumer trust, which in turn affects satisfaction and the intention to recommend a product or service, demonstrating that the principles of risk management, trust, and satisfaction are fundamental to customer relationships across various sectors, including the halal food industry

| [41] | Puspita, A. T., & Shikur, A. A. (2022). General risk on trust, satisfaction, and recommendation intention for halal food: Evidence in Indonesia. Islamic Marketing Review, 1(1). https://doi.org/10.5896/mwv11267 |

[41]

. This collective body of international research firmly establishes the critical role of ATM service quality in shaping customer perceptions and fostering positive outcomes for financial institutions worldwide.

2.2.2. Studies Inside Ethiopia

A concentrated body of research conducted within Ethiopia offers valuable, context-specific insights into the intricate relationship between ATM service delivery and customer satisfaction. It has been established that several key dimensions of ATM service quality significantly contribute to customer satisfaction within the Ethiopian banking context

| [10] | Embiale, Y. (2016). The effect of automatic teller machine service quality on customer satisfaction: The case of the Commercial Bank of Ethiopia in Hawassa City. Journal of Engineering and Economic Development, 3(2). https://doi.org/10.7176/jmcr/58-01 |

[10]

. This is also significant in the context of the rise of Islamic finance in Ethiopia, where technological advancements and accessible services are seen as a tool for economic development and poverty reduction

| [44] | Shikur, A. A., & Akkas, E. (2024). Islamic microfinance services: a catalyst for poverty reduction in eastern Ethiopia. International Journal of Islamic and Middle Eastern Finance and Management, 17(4), 770-788. https://doi.org/10.1108/imefm-09-2023-0327 |

[44]

. Building upon this foundational research,

| [34] | Nigatua, A. G., Belete, A. A., & Habtie, G. M. (2023). Effects of automated teller machine service quality on customer satisfaction: Evidence from commercial bank of Ethiopia. Heliyon, 9(11), e19132. https://doi.org/10.1016/j.heliyon.2023.e19132 |

[34]

used careful number-based methods to study Ethiopian commercial banks in the Afar region and clearly showed that better ATM service quality leads to higher customer satisfaction. Providing a localized perspective,

| [14] | Gessese, N. B. (2018). Factors affecting customer satisfaction towards ATM service: A case study of Commercial Bank of Ethiopia in Addis Ababa. Journal of Marketing and Consumer Research, 48, 1-8. |

[14]

specifically examined the factors influencing customer satisfaction with ATM services within the Commercial Bank of Ethiopia in Addis Ababa. Similarly,

| [48] | Tasaw, M. M. (2019). Impact of automated teller machine (ATM) service quality dimensions on customer satisfaction: A case study of Awash Bank selected branches in Addis Ababa, Ethiopia. Journal of Marketing and Consumer Research, 57, 1-10. https://doi.org/10.7176/jmcr/72-02 |

[48]

delved into the impact of specific ATM service quality dimensions on customer satisfaction within Awash Bank branches, also located in Addis Ababa. This understanding was further contributed to by a study that explored the determinants of customer satisfaction with ATM services at United Bank S. C.

| [29] | Lulit, A. M. (2019). Factors affecting customer satisfaction in ATM service: The case of United Bank S. C. in Addis Ababa, Ethiopia. Journal of Accounting and Financial Management, 5(2), 34-47. |

[29]

. The efficiency of ATM services can also have a direct impact on broader business operations, as highlighted by a study on bank regulations and firm performance in Ethiopian commercial banks

| [52] | Yusuf, J. M., & Shikur, A. A. (2023). Bank Regulations and Firm Performance: In the Case of Ethiopian Commercial Banks. International Journal of Finance and Banking Research, 9(4), 58-67. https://doi.org/10.11648/j.ijfbr.20230904.11 |

[52]

. Finally,

expanded the topic by looking into what influences how ATM services are set up in Ethiopian commercial banks, providing a better understanding of the strategic issues related to ATM networks in the country. Collectively, these studies conducted within Ethiopia consistently underscore the critical role of ATM service quality in shaping customer satisfaction within the country's banking sector, providing valuable, localized evidence and insights.

2.3. Research Gap

While the existing body of research, both globally and within Ethiopia, has extensively explored the relationship between ATM service delivery and customer satisfaction, several significant gaps remain, which this study is specifically designed to address. The introduction highlights that despite the strategic importance of ATMs and increasing investment in this technology, persistent operational challenges such as service disruptions, network problems, and frequent breakdowns continue to negatively impact customer experience

| [7] | Asfaw, S. (2024). Examining the effects of ATM service quality on customers satisfaction: In the case of Dashen Bank Western District, Addis Ababa, Ethiopia, 2024 [Unpublished master's thesis]. St. Mary's University. |

[7]

. This indicates a broader issue that existing studies have not fully resolved.

Firstly, although studies in Ethiopia, such as those by

| [1] | Adane, M. D., Wale, T., & Meried, E. W. (2021). Determinants of automated teller machine deployment in commercial banks of Ethiopia. Heliyon, 7(8). https://doi.org/10.1016/j.heliyon.2021.e07712 |

| [34] | Nigatua, A. G., Belete, A. A., & Habtie, G. M. (2023). Effects of automated teller machine service quality on customer satisfaction: Evidence from commercial bank of Ethiopia. Heliyon, 9(11), e19132. https://doi.org/10.1016/j.heliyon.2023.e19132 |

| [47] | Tambasi, J. R. (2019). Influence of electronic delivery services on customer satisfaction in savings and credit cooperatives, a case of Mwalimu National Sacco, Kenya [Unpublished master's thesis]. University of Nairobi. |

[1, 34, 47]

, acknowledge the importance of ATM service delivery, there is a distinct lack of research focused on the specific determinants of ATM service quality and their impact on customer satisfaction within the unique operational context of a single location, such as the Bank of Abyssinia's Dire Dawa Interest-Free Branches. The local situation, shaped by its specific geographical context and customer base, may present unique challenges and service needs that are not captured by broader national or regional studies.

Secondly, while previous Ethiopian studies have examined the influence of ATM service delivery on customer satisfaction, a comprehensive investigation that applies all five dimensions of the SERVQUAL model assurance, tangibility, empathy, reliability, and responsiveness is needed for this specific branch. Many existing studies may focus on only a subset of these dimensions or generalize findings from the broader banking sector, potentially overlooking the nuanced and relative impact of each SERVQUAL dimension on customer satisfaction at this particular location.

Finally, bridging the issues highlighted in the problem statement such as system failures and network issues with a detailed analysis of how they directly translate into customer dissatisfaction remains a critical research gap. This study aims to provide a more granular understanding of the relationship between these practical, on-the-ground issues and customer perceptions of service delivery at the Bank of Abyssinia's Dire Dawa Interest-Free Branch, thereby offering actionable insights for the bank's management to improve service quality and align with the broader ethical framework of Islamic banking. In essence, this research aims to provide a focused and comprehensive analysis that addresses the limitations of broader studies, contributing valuable, localized knowledge to the existing body of literature.

2.4. Hypothesis Development

2.4.1. ATM Service Reliability and Customer Satisfaction

ATM service reliability is a cornerstone of service delivery, referring to the ability of automated teller machines to perform the promised service dependably and accurately on a consistent basis

| [40] | Parasuraman, A., Zeithaml, V. A., & Berry, L. L. (1988). SERVQUAL: A multiple-item scale for measuring consumer perceptions of service quality. Journal of Retailing, 64(1), 12-40. https://doi.org/10.1037/t09264-000 |

[40]

. The term encompasses the dependable availability of cash, error-free transaction processing, consistent hardware and software functionality, and the reliable generation of transaction records

| [26] | Islam, M. S., Hossain, M. A., & Islam, M. T. (2020). Impact of ATM service quality on customer satisfaction and brand image: Evidence from the banking sector of Bangladesh. Journal of Asian Finance, Economics and Business, 7(10), 815-824. https://doi.org/10.58753/jbspust.4.1.2023.17 |

[26]

. When ATMs operate reliably, customers gain trust in their ability to handle financial transactions smoothly, which is a fundamental requirement in Islamic banking where transactions must be free from uncertainty (

gharar) and deceit. This reliability minimizes inconvenience and fosters confidence in the bank

. Across various service industries, reliability is a cornerstone of customer satisfaction. In the context of ATMs, customers expect them to function without frequent interruptions, execute transactions accurately, and have sufficient cash available. Conversely, issues like downtime, inaccurate transactions, and lack of cash significantly diminish customer satisfaction.

Empirical studies consistently highlight reliability as a key determinant of ATM service delivery. Research in Ethiopia shows that reliability is very important for how customers view ATM services

| [10] | Embiale, Y. (2016). The effect of automatic teller machine service quality on customer satisfaction: The case of the Commercial Bank of Ethiopia in Hawassa City. Journal of Engineering and Economic Development, 3(2). https://doi.org/10.7176/jmcr/58-01 |

| [49] | Tavakol, M., & Dennick, R. (2011). Making sense of Cronbach's alpha. International Journal of Medical Education, 2, 53-55. https://doi.org/10.5116/ijme.4dfb.8dfd |

| [34] | Nigatua, A. G., Belete, A. A., & Habtie, G. M. (2023). Effects of automated teller machine service quality on customer satisfaction: Evidence from commercial bank of Ethiopia. Heliyon, 9(11), e19132. https://doi.org/10.1016/j.heliyon.2023.e19132 |

[10, 49, 34]

. Similarly, studies on self-service banking technology show similar results

| [24] | Iberahim, H., Taufik, N. R. M., & Shamsudin, M. F. (2016). Service quality and customer satisfaction: The mediating effect of customer relationship management (CRM). Journal of Business and Retail Management Research, 10(2), 84-97. |

[24]

. The importance of ATM reliability is also confirmed by findings in Bangladesh, Rwanda, and Pakistan

| [4] | Aktar, M. S. (2024). The impacts of ATM service quality on client satisfaction and loyalty: a study on selected banks in Bangladesh. Journal of Business Studies, 4(1), 1-20. https://doi.org/10.58753/jbspust.4.1.2023.17 |

| [35] | Nshimiyimana, A., & Chen, W. (2019). An empirical study analyzing the ATM service quality and customer satisfaction relationship in Rwanda. International Journal of Business and Economics Research, 8(6), 439-451. https://doi.org/10.11648/j.ijber.20190806.24 |

| [8] | Aslam, W., Tariq, A., & Arif, I. (2019). The effect of ATM service quality on customer satisfaction and customer loyalty: An empirical analysis. Global Business Review, 1-24. https://doi.org/10.1177/0972150919846965 |

[4, 35, 8]

. Even research focusing on other aspects like efficiency, security, and responsiveness implicitly highlights the necessity of underlying reliability for these factors to be effective in satisfying customers

| [28] | Kumbhar, V. M. (2011). Customers' satisfaction in ATM service: An empirical evidences from public and private sector banks in India. Management Research and Practice, 3(2), 24-35. |

[28]

.

H1: ATM service reliability positively affects customer satisfaction for Interest-Free Banking customers at the Dire Dawa Branch.

2.4.2. ATM Service Responsiveness and Customer Satisfaction

ATM service responsiveness is a critical factor in shaping customer satisfaction, encompassing the bank's ability and willingness to promptly address customer inquiries, resolve problems, and provide efficient service

. This includes the speed and effectiveness of handling ATM malfunctions, delivering new cards, and addressing complaints. This commitment to meeting customer needs in a timely and effective manner is a key tenet of Islamic finance, as it builds trust and demonstrates a service-oriented approach. This ethical framework also ensures that the bank's responsiveness is transparent and fair, aligning with the principles of avoiding excessive uncertainty (

gharar) and upholding justice (

'adl)

| [39] | Osman, R., Abdul-Rahim, H., & Hussin, H. (2021). Service quality dimensions of Islamic banks and their impact on customer satisfaction and loyalty. Journal of Islamic Marketing, 12(3), 570-589. 10.1108/JIM-07-2020-0255 |

[39]

.

Studies consistently indicate that when banks demonstrate high levels of responsiveness, customers are more satisfied

| [40] | Parasuraman, A., Zeithaml, V. A., & Berry, L. L. (1988). SERVQUAL: A multiple-item scale for measuring consumer perceptions of service quality. Journal of Retailing, 64(1), 12-40. https://doi.org/10.1037/t09264-000 |

[40]

. For instance, research on self-service technology in retail banking highlights responsiveness as a significant factor influencing customer satisfaction

| [24] | Iberahim, H., Taufik, N. R. M., & Shamsudin, M. F. (2016). Service quality and customer satisfaction: The mediating effect of customer relationship management (CRM). Journal of Business and Retail Management Research, 10(2), 84-97. |

[24]

. Similarly, a study by

| [10] | Embiale, Y. (2016). The effect of automatic teller machine service quality on customer satisfaction: The case of the Commercial Bank of Ethiopia in Hawassa City. Journal of Engineering and Economic Development, 3(2). https://doi.org/10.7176/jmcr/58-01 |

[10]

on ATMs in Hawassa, Ethiopia, found that a bank's willingness to provide prompt service positively impacts customer satisfaction. The importance of responsiveness as a key element of overall service delivery is also underscored in research on Nigerian banks

. In their study on private banking in Bangladesh,

| [23] | Hoque, M. A., Jahan, F., & Begum, F. (2024). Exploring the nexus of ATM service quality, customer satisfaction, and loyalty in the private banking sector in Bangladesh. Pakistan Journal of Life and Social Sciences, 22(1), 1091-1104. https://doi.org/10.57239/pjlss-2024-22.1.0074 |

[23]

found responsiveness to be a crucial aspect of ATM service delivery affecting customer satisfaction and loyalty. Research in India implicitly suggests that a lack of responsiveness contributes to lower satisfaction levels

| [28] | Kumbhar, V. M. (2011). Customers' satisfaction in ATM service: An empirical evidences from public and private sector banks in India. Management Research and Practice, 3(2), 24-35. |

[28]

. Another study conducted by

| [46] | Solomon, N. (2023). Effect of ATM service quality on customer satisfaction: Case study of selected bank [Unpublished master's thesis]. St. Mary's University. |

[46]

further supports the link between how quickly and effectively banks address ATM-related issues and customer contentment.

H2: ATM service responsiveness positively affects customer satisfaction for Interest-Free Banking customers at the Dire Dawa Branch.

2.4.3. ATM Service Tangibility and Customer Satisfaction

In the context of Islamic banking, ATM service tangibility goes beyond a simple physical presence; it reflects a commitment to Islamic principles of purity, cleanliness, and professionalism. Tangibility refers to the physical elements of a service that customers can perceive through their senses, such as the ATM itself, the surrounding environment, and any related materials

| [40] | Parasuraman, A., Zeithaml, V. A., & Berry, L. L. (1988). SERVQUAL: A multiple-item scale for measuring consumer perceptions of service quality. Journal of Retailing, 64(1), 12-40. https://doi.org/10.1037/t09264-000 |

[40]

. The professionalism and appearance of staff, as well as the cleanliness, lighting, and aesthetic appeal of the ATM area, contribute to this perception. Positive perceptions of tangibility create a sense of trust, security, and comfort that align with the ethical values of Islamic finance. Conversely, negative perceptions can lead to dissatisfaction and cause customers to seek alternative, Sharia-compliant service providers.

Studies have consistently shown that when customers perceive the tangible elements of a service positively, their overall satisfaction is significantly influenced. Research focusing on the visual appeal of ATMs and their surroundings demonstrates that these tangible cues play a crucial role in shaping customer attitudes and feelings about the service experience. The importance of tangibility on customer satisfaction, particularly in the context of ATM services, has been examined in studies across various contexts. This research underscores the importance of maintaining and enhancing the physical aspects of service delivery to create a favorable customer experience

| [7] | Asfaw, S. (2024). Examining the effects of ATM service quality on customers satisfaction: In the case of Dashen Bank Western District, Addis Ababa, Ethiopia, 2024 [Unpublished master's thesis]. St. Mary's University. |

| [29] | Lulit, A. M. (2019). Factors affecting customer satisfaction in ATM service: The case of United Bank S. C. in Addis Ababa, Ethiopia. Journal of Accounting and Financial Management, 5(2), 34-47. |

| [47] | Tambasi, J. R. (2019). Influence of electronic delivery services on customer satisfaction in savings and credit cooperatives, a case of Mwalimu National Sacco, Kenya [Unpublished master's thesis]. University of Nairobi. |

[7, 29, 47]

.

H3: ATM service tangibility positively affects customer satisfaction for Interest-Free Banking customers at the Dire Dawa Branch.

2.4.4. ATM Service Empathy and Customer Satisfaction

In the context of Islamic banking, ATM service empathy, a crucial aspect of customer interaction, embodies the bank's capacity to understand and address the unique needs and perspectives of ATM users. It moves beyond mere functionality to demonstrate care, individualized attention, and anticipation of potential challenges

. This empathetic approach manifests in an intuitive interface design, proactive issue resolution through on-screen guidance and accessible support, and a commitment to ensuring safe and consistently operational environments, transparent communication, and fair complaint resolution. These elements are particularly important as they align with the Islamic principles of trust, transparency, and fairness.

Empirically, while "empathy" in ATM service isn't always explicitly measured, its influence on customer satisfaction is evident in studies focusing on related service quality dimensions. For example,

| [24] | Iberahim, H., Taufik, N. R. M., & Shamsudin, M. F. (2016). Service quality and customer satisfaction: The mediating effect of customer relationship management (CRM). Journal of Business and Retail Management Research, 10(2), 84-97. |

[24]

identified responsiveness conceptually linked to empathy through its focus on understanding and promptly addressing customer needs as a key driver of customer satisfaction. Significant dimensions such as fulfillment, ease of use, and security and privacy were also highlighted by

| [8] | Aslam, W., Tariq, A., & Arif, I. (2019). The effect of ATM service quality on customer satisfaction and customer loyalty: An empirical analysis. Global Business Review, 1-24. https://doi.org/10.1177/0972150919846965 |

[8]

; efficient, user-friendly, and secure ATMs demonstrate an implicit understanding of customer needs, which in turn leads to higher satisfaction. The significant impact of overall service quality, including elements akin to empathy, is further supported by studies

| [17] | Giao, H. N. K. (2019). Customer satisfaction towards ATM services: A case of Vietcombank Vinh Long, Vietnam. Journal of Asian Finance, Economics and Business, 6(1), 141-148. https://doi.org/10.13106/jafeb.2019.vol6.no1.141 |

| [25] | Idris, B. (2014). Customer satisfaction of automated teller machines (ATM) based on service quality. The 2014 WEI International Academic Conference Proceedings, New Orleans, USA. |

[17, 25]

. Consequently, it can be inferred that ATM service quality dimensions that reflect an understanding of customer needs and a commitment to a positive experience (i.e., empathy) positively influence customer satisfaction.

H4: ATM service empathy positively affects customer satisfaction for Interest-Free Banking customers at the Dire Dawa Branch.

2.4.5. ATM Service Assurance and Customer Satisfaction

ATM service assurance, within the Islamic banking context, refers to the financial institution's ability to convey trust and confidence in the reliability, security, and competence of its automated teller machine services

| [40] | Parasuraman, A., Zeithaml, V. A., & Berry, L. L. (1988). SERVQUAL: A multiple-item scale for measuring consumer perceptions of service quality. Journal of Retailing, 64(1), 12-40. https://doi.org/10.1037/t09264-000 |

[40]

. Fundamentally, this assurance is rooted in the bank's strict adherence to Sharia compliance, which ensures all transactions are free from prohibited elements such as interest (

riba), excessive uncertainty (

gharar), and gambling (

maisir). This dual commitment to both operational reliability and religious principles is crucial for building customer satisfaction.

The continuous availability of cash, the quality of notes, and the completeness of transactions are essential factors in providing this assurance. A lack of these elements can lead to customer dissatisfaction. Tangible aspects of ATM assurance include well-maintained and functioning machines, clear and professional signage, and a secure environment

| [26] | Islam, M. S., Hossain, M. A., & Islam, M. T. (2020). Impact of ATM service quality on customer satisfaction and brand image: Evidence from the banking sector of Bangladesh. Journal of Asian Finance, Economics and Business, 7(10), 815-824. https://doi.org/10.58753/jbspust.4.1.2023.17 |

[26]

. Intangibly, assurance is conveyed through the perceived reliability of the ATM in processing transactions accurately and consistently, the protection of customer data and privacy during transactions, and the availability of knowledgeable and courteous staff who can instill confidence and trust

| [3] | Akomolafe, D. T., & Afeni, B. O. (2014). Using database management system to generate, manage and secure personal identification numbers (PIN). Journal of Software Engineering and Applications, 7(05), 461. https://doi.org/10.4236/jsea.2014.75043 |

[3]

.

Studies have explored the impact of ATM service quality dimensions like credibility, completeness, and security on customer satisfaction

| [46] | Solomon, N. (2023). Effect of ATM service quality on customer satisfaction: Case study of selected bank [Unpublished master's thesis]. St. Mary's University. |

[46]

. The idea that ATM service quality significantly contributes to customer satisfaction is also supported by research that encompasses factors like reliability, convenience, and security

| [10] | Embiale, Y. (2016). The effect of automatic teller machine service quality on customer satisfaction: The case of the Commercial Bank of Ethiopia in Hawassa City. Journal of Engineering and Economic Development, 3(2). https://doi.org/10.7176/jmcr/58-01 |

[10]

. Additionally,

| [32] | Mwatsika, C. (2016). Factors influencing customer satisfaction with ATM banking. International Journal of Academic Research in Business and Social Sciences, 6(2), 172-185. https://doi.org/10.6007/ijarbss/v6-i2/2002 |

[32]

emphasizes the importance of ATM banking as a key channel for delivering banking products and services, further highlighting the link between ATM service and customer satisfaction.

H5: ATM Service assurance positively affects customer satisfaction for Interest-Free Banking customers at the Dire Dawa Branch.

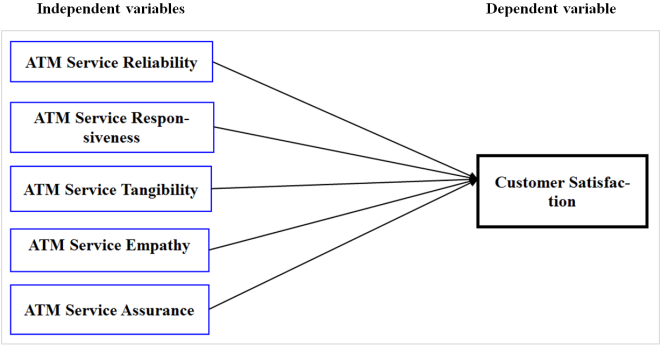

2.5. Conceptual Framework

The conceptual framework for this study is built upon the SERVQUAL model, with the aim of exploring how ATM service delivery factors affect customer satisfaction. This study specifically focuses on the Bank of Abyssinia's Dire Dawa Interest-Free banking windows and uses the five key dimensions of the SERVQUAL model: reliability, responsiveness, tangibility, empathy, and assurance. This framework is adapted to the context of Interest-Free Banking. The following diagram illustrates the conceptual framework of the study, showing how these independent variables are expected to influence the dependent variable, customer satisfaction. Hence the next diagram illustrates the conceptual framework of the study.

Figure 1. Conceptual framework.

4. Result and Analysis

4.1. Reliability Statistics

Reliability is a measure of the consistency of a research instrument. This study established the reliability of its questionnaire by employing Cronbach's alpha, with results calculated using SPSS 26. The questions for each variable were designed to consistently assess their intended concepts. According to

, an acceptable Cronbach’s alpha level typically ranges from 0.70 to 0.95. The alpha values for all five variables, ATM service reliability, responsiveness, tangibility, empathy, and assurance, were found to be between 0.732 and 0.877. These results, presented in

table 1 below, demonstrate that the questionnaire used to measure customer satisfaction among Interest Free Banking customers at the Bank of Abyssinia's Dire Dawa Branch is reliable.

Table 1. Reliability Test (Cronbach’s Alpha).

Variables | Number of items | Cronbach’s Alpha |

Reliability | 5 | 0.783 |

Responsiveness | 5 | 0.771 |

Tangibility | 5 | 0.877 |

Empathy | 5 | 0.732 |

Assurance | 5 | 0.831 |

Customer Satisfaction | 5 | 0.750 |

Source: Authors' Own.

4.2. Demographic Results and Descriptive Statistics

This section presents the quantitative analysis of the survey responses. To mitigate potential non-response bias, a total of 356 structured questionnaires were distributed to the selected sample. The researcher's maximum effort in the data collection process resulted in a high response rate of 89.3%, which yielded 318 usable questionnaires after removing 38 non-returned or incomplete submissions. According to

| [31] | Muganda, M. (1999). Business research methods. African Nazarene University. |

[31]

, the response rate of 50% is adequate, 60% is good, and 90% and above is considered excellent for analysis and reporting. Therefore, the high response rate achieved in this study falls within the good to excellent range and provides a highly representative sample suitable for robust statistical analysis. This section is divided into two parts: respondent demographics and a presentation of the survey results.

4.2.1. Respondent’s Demographic Socio-economic Characteristics

This foundational section aims to establish a clear understanding of the sample's composition and its context within the study on Interest-Free Banking (IFB) customers. The questionnaire commenced with a section on demographic characteristics to profile the respondents' socio-economic backgrounds.

The sample's gender distribution revealed a notable male majority, with 196 (61.6%) males compared to 122 (38.4%) females. Analyzing the age of the respondents, the findings indicate a strong concentration of participants in the young to middle-aged categories, as a significant 75.2% of the sample fell within the 18 to 40-year age bracket. The most substantial group of participants was aged 31 to 40 years, comprising 124 individuals (39%). This demographic profile is crucial as it underscores the prominent role of these age cohorts in shaping the study's findings on digital service quality.

Concerning educational status, the data showed that a significant majority of the respondents, 74.9%, had attained a diploma or higher, implying that the insights gathered are largely from individuals with post-secondary education. Most respondents indicated having a savings account with the Bank of Abyssinia, a category that encompassed 240 individuals (75.5%). This finding highlights the prevalence of savings accounts among the customer base surveyed. Lastly, the frequency with which customers utilize the bank's services revealed that the most active segment interacts with the bank on a daily basis, comprising 134 respondents (42.1%). This pattern indicates that a considerable portion of the study participants are regular and frequent users, suggesting their experiences and perceptions are well-formed and based on consistent interaction with the bank's services.

Table 2. Demographic and Socio-economic Characteristics of Respondents.

Features | Category | Frequency | Percent |

Gender | Male | 196 | 61.6 |

Female | 122 | 38.4 |

Total | 318 | 100 |

Age | 18- 30 | 115 | 36.2 |

31-40 | 124 | 39 |

41-50 | 56 | 17.6 |

Above 50 | 23 | 7.2 |

Total | 318 | 100 |

Educational Status | Below grade 12 | 80 | 25.1 |

Diploma | 123 | 38.7 |

Degree | 101 | 31.8 |

MSc and above | 14 | 4.4 |

Total | 318 | 100 |

Account Type | Current | 61 | 19.2 |

Saving | 240 | 75.5 |

Others | 17 | 5.3 |

Total | 318 | 100 |

Frequency of using the Bank | Daily | 134 | 42.1 |

Twice a week | 65 | 20.5 |

Weekly | 70 | 22 |

Monthly | 49 | 15.4 |

Total | 318 | 100 |

Source: Authors' Own.

4.2.2. Descriptive Statistics

Table 3 presents a descriptive overview of several key service delivery dimensions and customer satisfaction, utilizing mean scores and standard deviations derived from a five-point scale administered to 318 respondents. The interpretation of these scores is facilitated by categorizing them into low (below 2), moderate (2 to below 3), and high (3 and above) perception levels

| [43] | Sassenberg, K., Kessler, T., & Mummendey, A. (2011). Less is more? Social inclusion and exclusion as complementary predictors of discrimination. British Journal of Social Psychology, 50(4), 618-637. https://doi.org/10.1016/s0022-1031(02)00519-x |

[43]

.

Examining the variable of Reliability, its mean signifies a high level of perceived service dependability and accuracy, with a standard deviation indicating a moderate consistency in responses. Similarly, respondents perceive Responsiveness as high, with a high mean and a standard deviation reflecting a consistent positive view. Tangibility stands out with a moderate mean, placing it in the moderate perception category, and its higher standard deviation reveals the most diverse range of opinions among the assessed service delivery dimensions. Empathy registers the highest perception level with a high mean, and its standard deviation suggests a relatively consistent positive view. Assurance is also perceived as high, with a high mean and a standard deviation reflecting consistency. Finally, Customer Satisfaction registers a high overall level of satisfaction, with a standard deviation reflecting a moderate spread in responses. Overall, the data shows that most respondents have a positive view of the service delivery aspects, with tangibility being the only area seen as average and having the most varied responses. Furthermore, the overall level of customer satisfaction is also high among the respondents.

Table 3. Descriptive statistics.

Variables | N | Mean | Std. Deviation |

Reliability | 318 | 3.50 | .852 |

Responsiveness | 318 | 3.49 | .827 |

Tangibility | 318 | 2.91 | .987 |

Empathy | 318 | 3.81 | .772 |

Assurance | 318 | 3.70 | .833 |

Customer Satisfaction | 318 | 3.5824 | .764 |

Source: Authors' Own.

4.3. Test for the Linear Regression Model Assumption

4.3.1. Linearity

According to

| [20] | Hair, J. F., Black, W. C., Babin, B. J., Anderson, R. E., & Tatham, R. L. (2006). Multivariate data analysis (6th ed.). Pearson Prentice Hall. https://doi.org/10.2307/2983017 |

[20]

, the linearity test for the connection between variables is conducted using the correlation method. This relationship can be visually represented using a scatter plot, where pairs of values for two metric variables are mapped as individual points, with the aim of identifying a straight-line trend in the plotted data.

| [15] | Ghozali, I. (2006). Aplikasi analisis multivariate dengan program SPSS. Badan Penerbit Universitas Diponegoro. |

[15]

explains that homoscedasticity means the amount of error is the same no matter the level of the predictor variables. In simple terms, when looking at a dependent variable, homoscedasticity means that the spread of variance is the same across all levels of the predictor variables, which can be considered a cloud of dots on a scatter plot. On the other hand, non-homoscedasticity is usually considered a funnel shape, which shows that the error variance goes up (or down) in a regular way as the dependent variable changes.

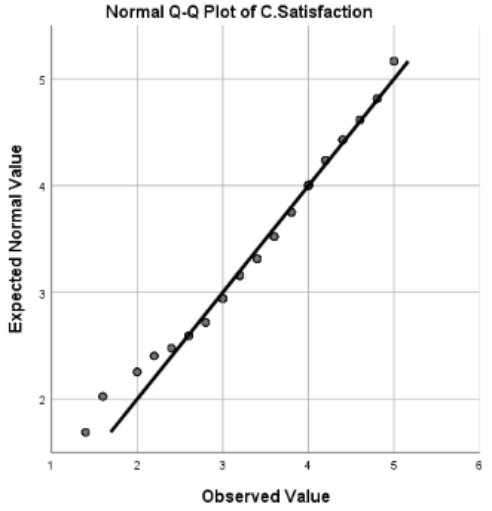

Figure 2 below illustrates the study's linearity results. This pattern suggests that the distribution of customer satisfaction is approximately normal.

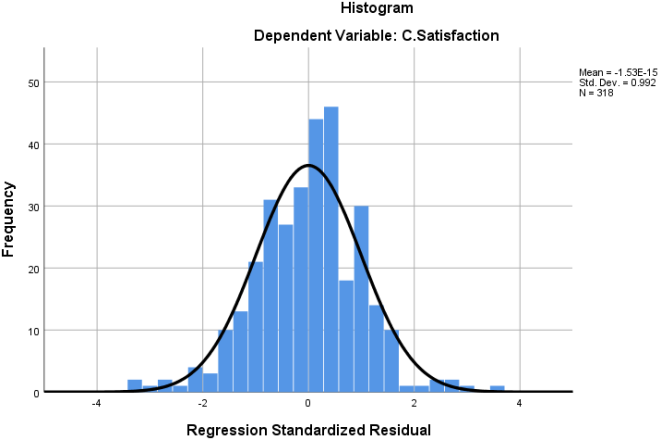

4.3.2. Normality

The histogram shows how the regression standardized residuals for customer satisfaction are spread out, along with a normal distribution curve. This visual assessment helps in evaluating whether the residuals are approximately normally distributed, a key assumption for many linear regression analyses

| [19] | Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2010). Multivariate data analysis (7th ed.). Prentice Hall. https://doi.org/10.2307/2348783 |

[19]

. Therefore,

Figure 3 presents a histogram suggesting approximately normally distributed residuals.

4.3.3. Multicollinearity

(i). Variance Inflation Factor (VIF)

According to

| [20] | Hair, J. F., Black, W. C., Babin, B. J., Anderson, R. E., & Tatham, R. L. (2006). Multivariate data analysis (6th ed.). Pearson Prentice Hall. https://doi.org/10.2307/2983017 |

[20]

, multicollinearity occurs when one variable exhibits a strong relationship with another. The more pronounced this inter-correlation, the more challenging it becomes to understand the individual impact of each variable in an analysis. Their close association makes it difficult to isolate the specific effect of any single predictor. In multiple regression analysis, a general rule is that multicollinearity isn't a big issue if the tolerance value for each variable is over 0.10 and the Variance Inflation Factor (VIF) is under 10. Additionally, if two variables have a high correlation coefficient (r) above 0.8, it can be a warning sign of multicollinearity. The following

Table 4 presents the results of the multicollinearity test. The researcher examined the Variance Inflation Factor (VIF), and

Table 4 shows that all VIF values ranged from 1.046 to 1.824. Because these values are all lower than the generally accepted cutoff of 5

| [21] | Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2017). A primer on partial least squares structural equation modeling (PLS-SEM) (2nd ed.). SAGE Publications. https://doi.org/10.1007/978-3-030-80519-7 |

[21]

, it can be concluded that multicollinearity did not significantly affect this analysis.

Table 4. Multicollinearity test.

Model | Collinearity Statistic |

Tolerance | VIF |

Constant | | |

Reliability | .552 | 1.810 |

Responsiveness | .548 | 1.824 |

Tangibility | .654 | 1.530 |

Empathy | .956 | 1.046 |

Assurance | .550 | 1.818 |

Source: Authors' Own.

(ii). Correlation Matrix

Correlation may be expressed as the degree of relationship present between two or more variables

| [26] | Islam, M. S., Hossain, M. A., & Islam, M. T. (2020). Impact of ATM service quality on customer satisfaction and brand image: Evidence from the banking sector of Bangladesh. Journal of Asian Finance, Economics and Business, 7(10), 815-824. https://doi.org/10.58753/jbspust.4.1.2023.17 |

[26]

. The linear correlation coefficient (r) is a measure of the degree of co-variability of the variables. The strength and the direction of a linear relationship between the two variables (dependent and independent) are measured by the linear correlation coefficient (r). The values that the correlation coefficient may assume vary from -1 to +1. There is a positive correlation between the variables when r is positive. r=+1 implies that there is a perfect positive correlation between variables. When r is negative, there exists a negative correlation between the variables. r=−1 implies that there is a perfect negative correlation between variables. When r is zero, there is no correlation between the variables. The following

table 5, presents the Pearson correlation matrix.

The Pearson correlation analysis reveals significant positive relationships between several factors and Customer Satisfaction within the study's sample of 318 participants. All correlations are statistically significant at the 0.01 level (p<0.01), indicating a low probability of these relationships occurring by chance. Notably, Reliability demonstrates the strongest positive correlation with Customer Satisfaction (r=.658), suggesting a strong association between higher service reliability and better customer outcomes. Responsiveness (r=.648) and Tangibility (r=.617) also exhibit strong positive correlations with Customer Satisfaction, implying that increased responsiveness and tangible features are significantly linked to improved customer satisfaction. Assurance (r=.594) shows a moderate-to-strong positive correlation, indicating that a feeling of security is also significantly associated with better Customer Satisfaction. Empathy (r=.227) shows a weak but significant positive correlation.

Furthermore, the analysis reveals intercorrelations among the independent variables themselves, suggesting that these factors are interrelated to varying degrees. For instance, Responsiveness and Tangibility show a strong positive correlation (r=.554). In conclusion, the findings strongly suggest that improvements in Reliability, Responsiveness, Tangibility, Assurance, and Empathy are all associated with enhanced Customer Satisfaction within this specific context. However, it is crucial to remember that correlation does not establish causation.

Table 5. Pearson Correlation.

Correlations |

| Reliability | Responsiveness | Tangibility | Empathy | Assurance | C. Satisfaction |

Reliability | Pearson Correlation | 1 | .539** | .427** | .169** | .616** | .658** |

Sig. (2-tailed) | | .000 | .000 | .003 | .000 | .000 |

N | 318 | 318 | 318 | 318 | 318 | 318 |

Responsiveness | Pearson Correlation | .539** | 1 | .554** | .170** | .539** | .648** |

Sig. (2-tailed) | .000 | | .000 | .002 | .000 | .000 |

N | 318 | 318 | 318 | 318 | 318 | 318 |

Tangibility | Pearson Correlation | .427** | .554** | 1 | .175** | .440** | .617** |

Sig. (2-tailed) | .000 | .000 | | .002 | .000 | .000 |

N | 318 | 318 | 318 | 318 | 318 | 318 |

Empathy | Pearson Correlation | .169** | .170** | .175** | 1 | .152** | .227** |

Sig. (2-tailed) | .003 | .002 | .002 | | .007 | .000 |

N | 318 | 318 | 318 | 318 | 318 | 318 |

Assurance | Pearson Correlation | .616** | .539** | .440** | .152** | 1 | .594** |

Sig. (2-tailed) | .000 | .000 | .000 | .007 | | .000 |

N | 318 | 318 | 318 | 318 | 318 | 318 |

C. Satisfaction | Pearson Correlation | .658** | .648** | .617** | .227** | .594** | 1 |

Sig. (2-tailed) | .000 | .000 | .000 | .000 | .000 | |

N | 318 | 318 | 318 | 318 | 318 | 318 |

Source: Authors' Own.

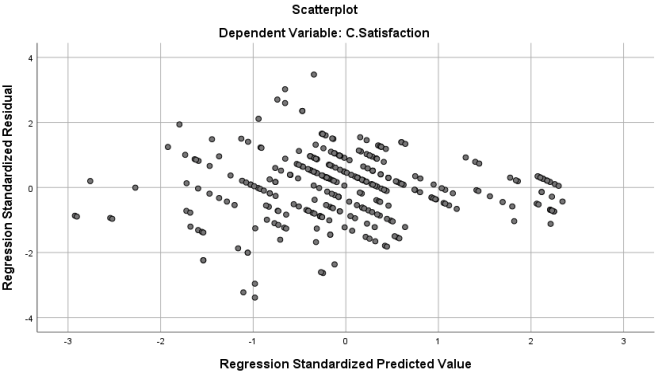

4.3.4. Homoscedasticity

Homoscedasticity means that the amount of "noise" or random error in our regression model is consistent across all predicted values of our dependent variable, Customer satisfaction.

Figure 4 (the scatterplot) allows us to visually check this assumption. If the spread of the points (representing the errors) is roughly the same across the entire range of predicted values, then homoscedasticity is likely present. In

Figure 4, the points appear randomly scattered without forming a distinct pattern like a funnel or a widening/narrowing band. This evidence suggests that the error variance is relatively constant across the predicted values of organizational performance. So, looking at

Figure 4, it appears that the assumption of homoscedasticity is satisfied, which means our regression analysis is likely reliable

| [12] | Field, A. (2018). Discovering statistics using IBM SPSS statistics (5th ed.). SAGE Publications. https://doi.org/10.1024/1012-5302/a000397 |

| [16] | Ghozali, I. (2018). Application of multivariate analysis with IBM SPSS. Badan Penerbit Universitas Diponegoro. |

[12, 16]

. If homoscedasticity is violated (heteroscedasticity), meaning the error variance changes with different predicted values, it can impact how accurate our predictions are and how valid our statistical tests are.

Figure 4. Homoscedasticity.

The researcher developed the following linear regression using the variables considered in the model.

CS=β0+β1X1+β2X2+β3X3+β4X4+β5X5+µ

The R-squared value shows how well the regression model accounts for changes in the dependent variable, while the beta coefficient indicates each variable’s level of influence on the dependent variable, which can be either positive or negative. The P-value indicates the probability that the observed results are due to chance.

As shown in

Table 6, the adjusted R-squared value of 62.4% means that the independent variables, which are the ATM service quality dimensions of reliability, responsiveness, tangibility, empathy, and assurance, together explain 62.4% of the customer satisfaction among Interest-Free Banking (IFB) customers. The remaining 37.6% of customer satisfaction is influenced by other variables not included in the mode.

Table 7 shows that the regression model is statistically significant, with a p-value less than 0.05. This finding indicates that the model significantly predicts the dependent variable, providing a satisfactory fit for the data.

Table 6. Model summary.

Model Summary |

Model | R | R Square | Adjusted R Square | Std. Error of the Estimate |

1 | .794a | .630 | .624 | .46849 |

a. Predictors: (Constant), Reliability, Responsiveness, Tangibility, Empathy, Assurance

b. Dependent Variable: Customer Satisfaction

Source: Authors' Own.

Table 7. ANOVA test.

ANOVAa |

Model | Sum of Squares | df | Mean Square | F | Sig. |

1 | Regression | 116.702 | 5 | 23.340 | 106.341 | .000b |

Residual | 68.479 | 312 | .219 | | |

Total | 185.181 | 317 | | | |

a. Dependent Variable: Customer Performance

a. Predictors: (Constant), Reliability, Responsiveness, Tangibility, Empathy, Assurance

Source: Authors' Own.

Table 8 presents the results of the model predicting performance using the variables of reliability, responsiveness, tangibility, empathy, and assurance. All of these variables were found to have a positive and significant effect on the outcome at a 95% confidence level. The unstandardized coefficient (beta value) for each variable indicates its degree of importance in influencing the dependent variable.

Table 8. Regression result.

Coefficients |

Model | Unstandardized Coefficients | Standardized Coefficients | T | Sig. |

B | Std. Error | Beta |

1 | (Constant) | .484 | .173 | | 2.804 | .005 |

Reliability | .282 | .042 | .314 | 6.784 | .000 |

Responsiveness | .220 | .043 | .238 | 5.109 | .000 |

Tangibility | .216 | .033 | .278 | 6.537 | .000 |

Empathy | .063 | .035 | .064 | 1.807 | .072 |

| Assurance | .129 | .043 | .140 | 3.024 | .003 |

a. Dependent Variable: Customer Satisfaction

Source: Authors' Own.

Regression Model Equation results are presented as follows.

CustomerSatisfaction=0.484+0.282Reliability+0.220Responsiveness+0.216Tangibility+0.063Empathy+0.129Assurance+µ

4.4. Discussion

4.4.1. ATM Service Reliability and IFB Customer Satisfaction

ATM service reliability, a fundamental aspect of service delivery, refers to the extent to which automated teller machines consistently deliver their promised services dependably and accurately

| [40] | Parasuraman, A., Zeithaml, V. A., & Berry, L. L. (1988). SERVQUAL: A multiple-item scale for measuring consumer perceptions of service quality. Journal of Retailing, 64(1), 12-40. https://doi.org/10.1037/t09264-000 |

[40]

. The term encompasses the dependable availability of cash, error-free transaction processing, and the consistent functionality of hardware and software

| [26] | Islam, M. S., Hossain, M. A., & Islam, M. T. (2020). Impact of ATM service quality on customer satisfaction and brand image: Evidence from the banking sector of Bangladesh. Journal of Asian Finance, Economics and Business, 7(10), 815-824. https://doi.org/10.58753/jbspust.4.1.2023.17 |

[26]

. For IFB customers, this reliability is crucial as it builds customer trust (amanah) and ensures transactions are free from excessive uncertainty (gharar), a key principle of Islamic finance. This dependability minimizes inconvenience and fosters confidence in the bank

.

The findings of this study, presented in

Table 8, demonstrate a substantial positive and significant impact of ATM service reliability on customer satisfaction (β = 0.282, p < 0.001). A 1% increase in perceived ATM service reliability is expected to increase customer satisfaction by a notable 28.2%. For instance, studies conducted within Ethiopia consistently underscore the importance of reliability.

| [10] | Embiale, Y. (2016). The effect of automatic teller machine service quality on customer satisfaction: The case of the Commercial Bank of Ethiopia in Hawassa City. Journal of Engineering and Economic Development, 3(2). https://doi.org/10.7176/jmcr/58-01 |

[10]

established that several key dimensions of ATM service quality, including reliability, significantly contribute to customer satisfaction within the Ethiopian banking context. Likewise,

| [49] | Tavakol, M., & Dennick, R. (2011). Making sense of Cronbach's alpha. International Journal of Medical Education, 2, 53-55. https://doi.org/10.5116/ijme.4dfb.8dfd |

| [34] | Nigatua, A. G., Belete, A. A., & Habtie, G. M. (2023). Effects of automated teller machine service quality on customer satisfaction: Evidence from commercial bank of Ethiopia. Heliyon, 9(11), e19132. https://doi.org/10.1016/j.heliyon.2023.e19132 |

[49, 34]

confirmed that reliability is very important for how customers view ATM services in the country.

This finding also resonates with international research. The crucial role of reliability in shaping customer satisfaction in their study in Rwanda

| [35] | Nshimiyimana, A., & Chen, W. (2019). An empirical study analyzing the ATM service quality and customer satisfaction relationship in Rwanda. International Journal of Business and Economics Research, 8(6), 439-451. https://doi.org/10.11648/j.ijber.20190806.24 |

[35]

. Similarly,